Assessing Q2 Holdings (QTWO) Valuation As Growth Slows And Margins Trail Competitors

Recent commentary around Q2 Holdings (QTWO) has focused on slower annual recurring revenue growth, an expected deceleration in sales, and a gross margin level that trails peers, raising fresh questions for investors about the stock’s risk and reward.

See our latest analysis for Q2 Holdings.

Against that backdrop, Q2 Holdings’ share price of $71.50 sits after a 12.9% 90 day share price return and a 1 year total shareholder return decline of 28.4%. This suggests recent momentum is building from a weaker longer term experience as investors reassess growth and margin risks alongside participation in events like the Raymond James Institutional Investors Conference.

If Q2’s story has you watching digital finance closely, it could be a good moment to see what else is moving among high growth tech and AI stocks that are reshaping financial and enterprise software.

With Q2 trading at $71.50, an intrinsic value estimate implying an 18.9% discount and analyst targets sitting higher, the key question is whether recent concerns are already in the price or if markets are still pricing in optimistic growth.

Most Popular Narrative Narrative: 20.3% Undervalued

With Q2 Holdings last closing at $71.50 against a narrative fair value of $89.71, the valuation gap is built on specific growth and margin assumptions that go well beyond a simple re rating story.

The increasing focus by financial institutions on digital transformation, evidenced by strong engagement and expanded investments in mission-critical digital banking, fraud prevention, and AI solutions, is likely to drive robust subscription revenue growth and improve retention for Q2 over the longer term. Heightened demand for integrated, omni-channel, and mobile-first banking experiences is accelerating adoption of Q2's unified platform across both new and existing customers, expanding the addressable market and supporting higher average revenue per user (ARPU) and overall revenue growth.

Curious what growth rate, profit margin step up, and future earnings multiple are baked into that $89.71 figure, and how those forecasts line up through 2028? The full narrative breaks out the revenue curve, the margin lift and the earnings profile that all feed into this 8.78% discount rate and help explain why the implied valuation sits where it does.

Result: Fair Value of $89.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including higher churn tied to bank M&A and tougher competition in fraud and risk tools that could challenge those optimism heavy assumptions.

Find out about the key risks to this Q2 Holdings narrative.

Another View On Valuation

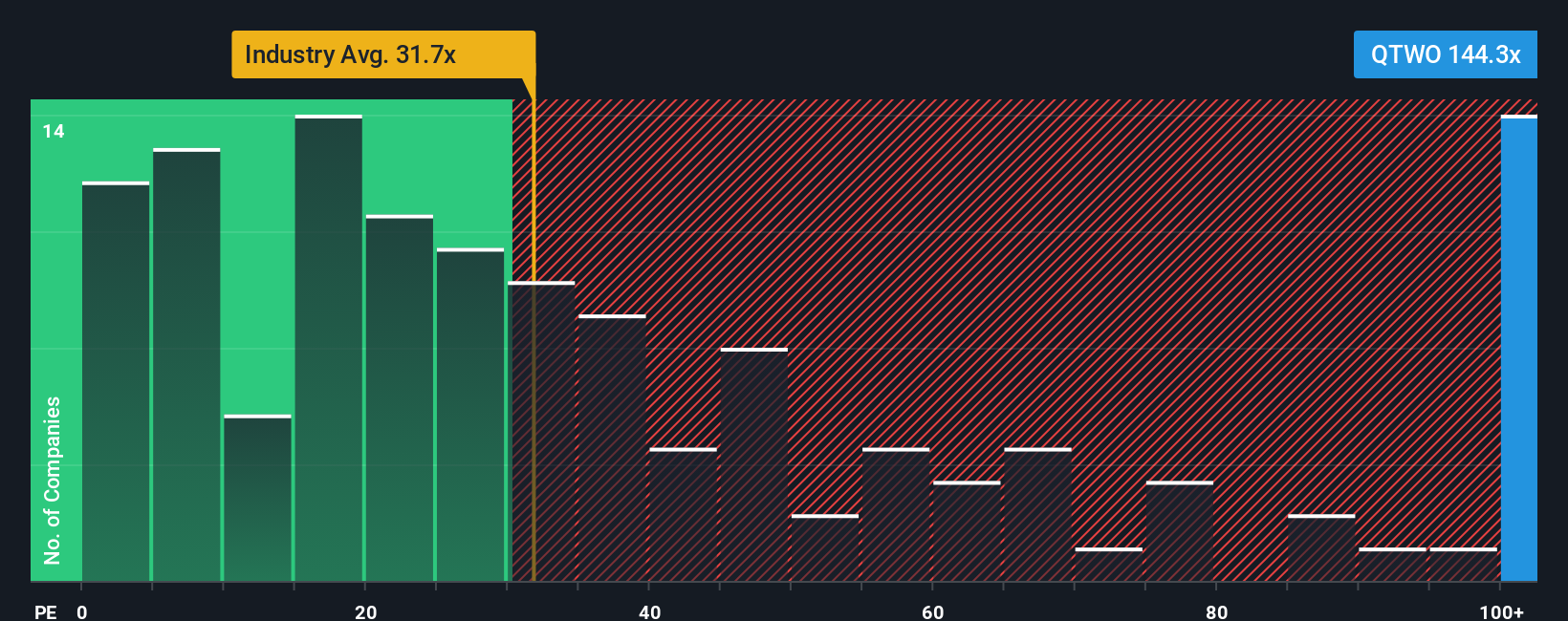

The narrative fair value of $89.71 suggests Q2 Holdings is 20.3% undervalued, but the P/E story pulls in the opposite direction. At about 140.9x earnings versus a US Software average of 32.7x and a peer average of 36.4x, the current multiple sits well above both reference points and a fair ratio of 52.2x. This raises the question of how much future growth is already baked into the price.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Q2 Holdings Narrative

If you are not convinced by these assumptions or prefer your own take on the numbers, you can quickly build a personalised story using Do it your way.

A great starting point for your Q2 Holdings research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Q2 has sparked your interest, do not stop there. Broaden your watchlist with a few focused stock ideas that could sharpen how you think about risk and return.

- Spot potential mispricings by scanning these 882 undervalued stocks based on cash flows that may offer more attractive entry points based on their cash flow profiles.

- Ride long term technology shifts by checking out these 27 AI penny stocks shaping everything from automation to next generation software tools.

- Add a different growth angle by reviewing these 79 cryptocurrency and blockchain stocks tied to digital assets and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com