- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Varonis (VRNS) Using Its SaaS Pivot and Buybacks to Redefine Its Core Business Model?

- In recent days, Varonis Systems has drawn renewed attention as it advances its shift from on-premises software to cloud-based SaaS data security, while analysts and investors reassess the business following weaker renewals and updated guidance.

- Despite this pressure, the company’s growing SaaS mix, new share repurchase authorization, and largely favorable analyst ratings are shaping a fresh view of its long-term business model.

- We’ll now examine how Varonis’ accelerated SaaS transition and the analyst reaction to recent renewal softness reshape the company’s investment narrative.

These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Varonis Systems Investment Narrative Recap

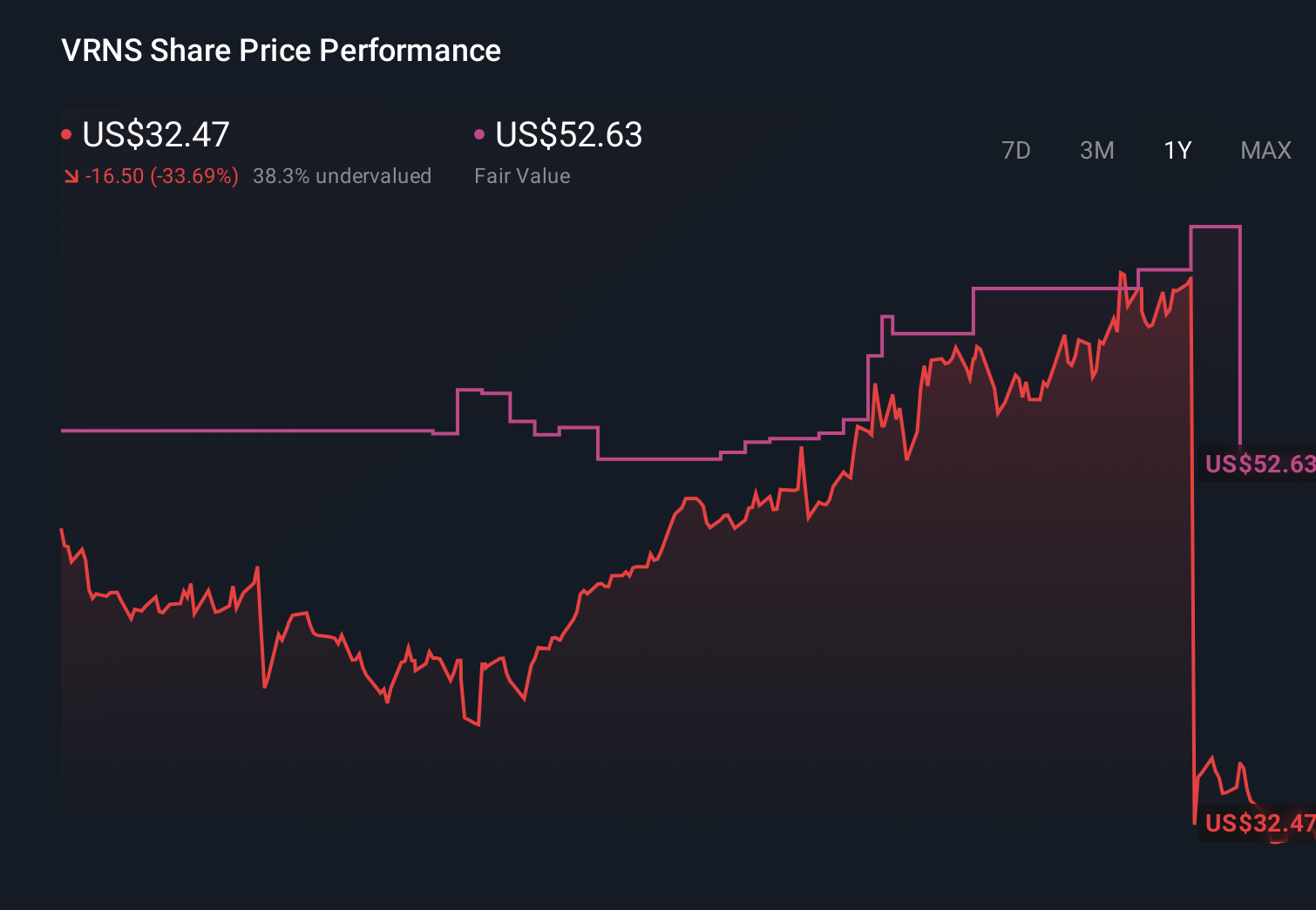

To own Varonis today, you need to believe its pivot to SaaS data security can outweigh short term pain from weaker renewals and volatile guidance. The key near term catalyst is clearer evidence that SaaS ARR growth and high cloud mix can restore confidence after the stock’s near 49% single day drop, while the biggest risk is that softer on prem and federal renewals signal deeper demand or competitive issues rather than a temporary transition bump.

The most relevant recent development is Varonis’ disclosure that SaaS now represents 76% of ARR, which directly ties into the current debate over its transition. This higher cloud mix supports the core catalyst of more visible, recurring revenue over time, but it also raises the stakes for execution, as investors will be watching closely to see if this SaaS heavy model can offset renewal softness and eventually translate into improving profitability.

Yet behind the optimism around SaaS growth, investors should be aware that persistent gross margin pressure and potential pricing strain could...

Read the full narrative on Varonis Systems (it's free!)

Varonis Systems' narrative projects $911.4 million revenue and $119.3 million earnings by 2028.

Uncover how Varonis Systems' forecasts yield a $51.84 fair value, a 46% upside to its current price.

Exploring Other Perspectives

Three members of the Simply Wall St Community value Varonis between US$51.84 and US$70, highlighting how far opinions can stretch. You should weigh that optimism against the risk that SaaS transition costs and margin pressure could keep reported earnings under strain for longer, with real implications for how the market values the stock.

Explore 3 other fair value estimates on Varonis Systems - why the stock might be worth just $51.84!

Build Your Own Varonis Systems Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Varonis Systems research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Varonis Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Varonis Systems' overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com