- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalOcugen (OCGN) Valuation Check As Social Media Buzz Highlights Its High Risk High Reward Pipeline

Social media driven spotlight on Ocugen

Ocugen (OCGN) is back in focus after a surge in social media chatter around its gene and cell therapy pipeline for eye diseases, highlighting the stock’s volatility and small cap biotech risk profile.

See our latest analysis for Ocugen.

The recent social media buzz has arrived on top of a strong short term run, with a 7 day share price return of 17.78% and 30 day share price return of 32.50% after a more mixed 90 day share price return of a 13.11% decline. Meanwhile, the 1 year total shareholder return of 91.36% and 3 year total shareholder return of 26.19% show how quickly sentiment on Ocugen can swing around clinical and funding milestones.

If Ocugen’s volatility has caught your eye, it can be helpful to compare it with a wider set of healthcare stocks that also hinge on clinical progress and regulatory outcomes.

With Ocugen still loss making on modest revenue and trading at US$1.59 against a US$9.00 target, you have to ask: is the recent excitement leaving value on the table, or is the market already pricing in future growth?

Most Popular Narrative Narrative: 82.3% Undervalued

Against Ocugen’s last close of US$1.59, the most followed narrative points to a fair value of about US$9.00, putting a bold spotlight on its long range potential.

Ocugen is progressing multiple gene therapy candidates (OCU400, OCU410, OCU410ST) towards late stage trials and regulatory filings, with three market authorization applications planned in the next three years. These therapies address large global patient populations with significant unmet needs, increasing the potential for substantial future revenue growth. The company’s modifier gene therapy platform leverages broad, gene agnostic mechanisms, potentially offering first/best in class, single treatment solutions for diseases like RP, Stargardt, and dry AMD. This positions Ocugen to benefit from ongoing advancements in biotechnology and genomics, and higher pricing/reimbursement for innovative, long acting therapies, which would positively impact long term net margins.

Curious how a loss making biotech gets marked up to that kind of fair value? The narrative leans heavily on rapid revenue expansion, margin turnaround, and a rich future earnings multiple. Want to see which assumptions really carry the weight in that US$9.00 figure and how a 7.17% discount rate shapes the outcome?

Result: Fair Value of $9 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upbeat story relies on unapproved late-stage programs and a high cash burn, so any trial setback or funding stumble could quickly challenge the current narrative.

Find out about the key risks to this Ocugen narrative.

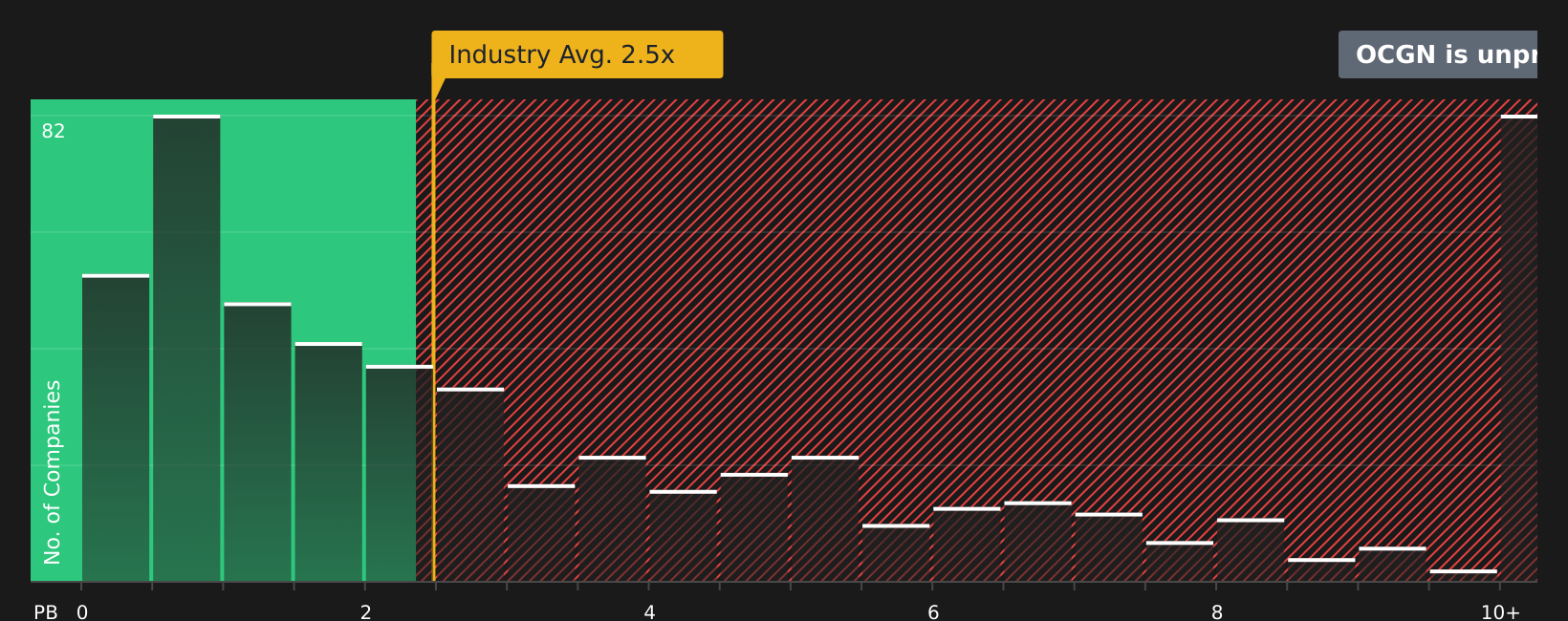

Another View: Multiples Paint A Very Different Picture

That eye catching fair value of about US$9.00 sits awkwardly beside Ocugen’s P/B ratio of 140.6x, compared with 2.7x for the wider US Biotechs industry and 3.5x for peers. At that kind of premium, are you looking at deep value, or simply paying far ahead of the fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ocugen Narrative

If you are not fully on board with this view or prefer to lean on your own judgment, you can test the numbers yourself in minutes, then Do it your way

A great starting point for your Ocugen research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Ocugen has sharpened your curiosity, do not stop here. There is a whole universe of other stocks you can filter quickly to match your style.

- Spot potential value setups by scanning these 884 undervalued stocks based on cash flows that align more closely with the cash flow profile you want to focus on.

- Explore major tech shifts by checking out these 26 AI penny stocks that are tied to specific use cases and listed market opportunities.

- Strengthen your income focus by reviewing these 12 dividend stocks with yields > 3% and see which companies currently combine yield with fundamental checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com