- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs PDD Holdings (PDD) Still Attractive After Recent Share Price Gains And DCF Reassessment

- If you are wondering whether PDD Holdings' share price still offers value after a strong run in recent years, this article will walk through what the current market price may be implying.

- PDD Holdings recently closed at US$120.97, with returns of 6.7% over 7 days, 3.3% over 30 days, 4.5% year to date, 20.6% over 1 year and 29.4% over 3 years, while the 5 year return stands at a 27.7% decline.

- Recent coverage has focused on PDD Holdings' position in Chinese e commerce and its international growth ambitions, as well as regulatory commentary that continues to shape sentiment toward major China based platforms. These themes help frame how investors are thinking about the stock's risk profile and potential opportunities today.

- On our valuation checks, PDD Holdings scores a 6 out of 6, and next we will look at how different valuation methods stack up, before ending with a way to think about value that goes beyond the usual ratios and models.

Approach 1: PDD Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model takes estimates of the cash a company could generate in the future, then discounts those cash flows back to today to arrive at an implied value for the equity.

For PDD Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flows reported in CN¥. The latest twelve month free cash flow is CN¥111.4b. Analyst estimates and Simply Wall St extrapolations project annual free cash flow out to 2035, with figures such as CN¥138.5b in 2026 and CN¥164.6b in 2027, and further extrapolated values for later years.

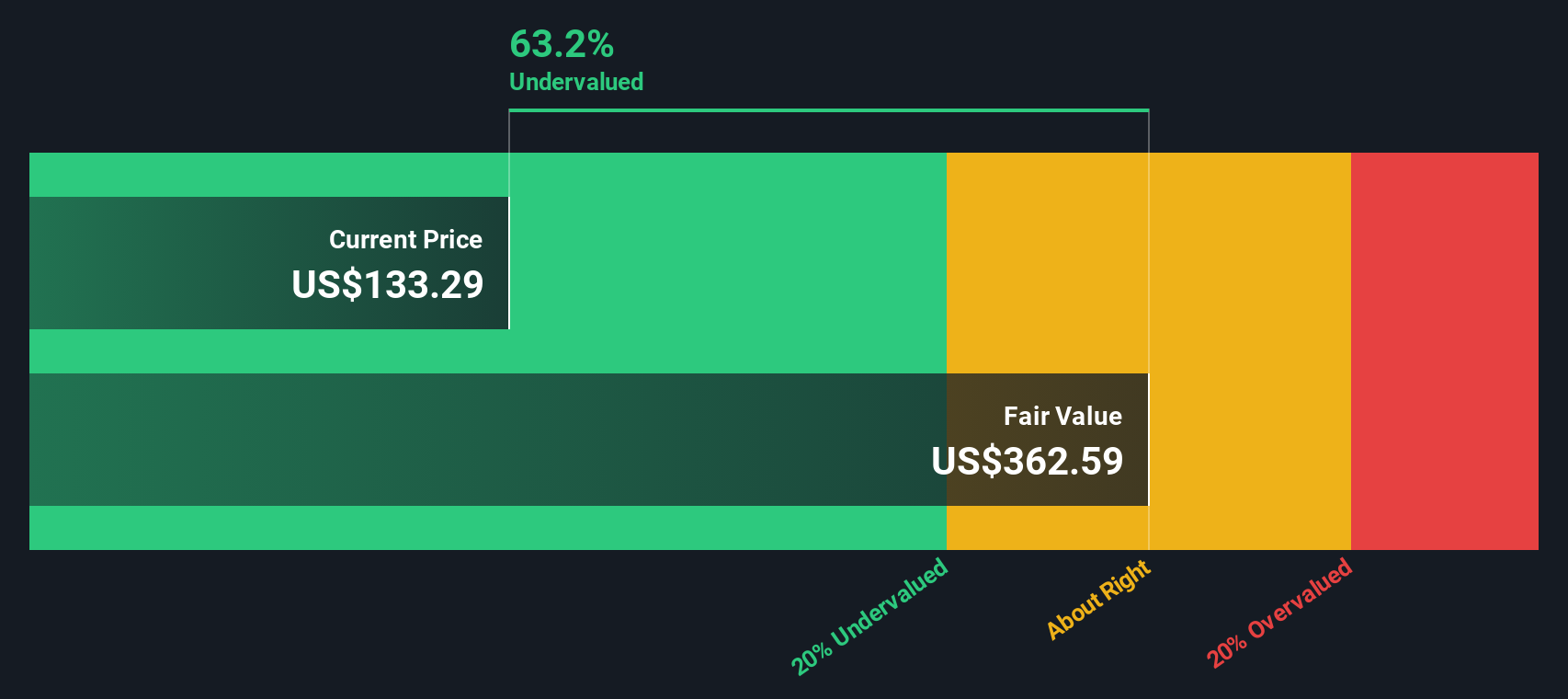

When all those projected cash flows are discounted back to today, the DCF model arrives at an estimated intrinsic value of US$343.88 per share, compared with the recent share price of US$120.97. That gap implies the stock is 64.8% undervalued on this set of assumptions.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests PDD Holdings is undervalued by 64.8%. Track this in your watchlist or portfolio, or discover 884 more undervalued stocks based on cash flows.

Approach 2: PDD Holdings Price vs Earnings

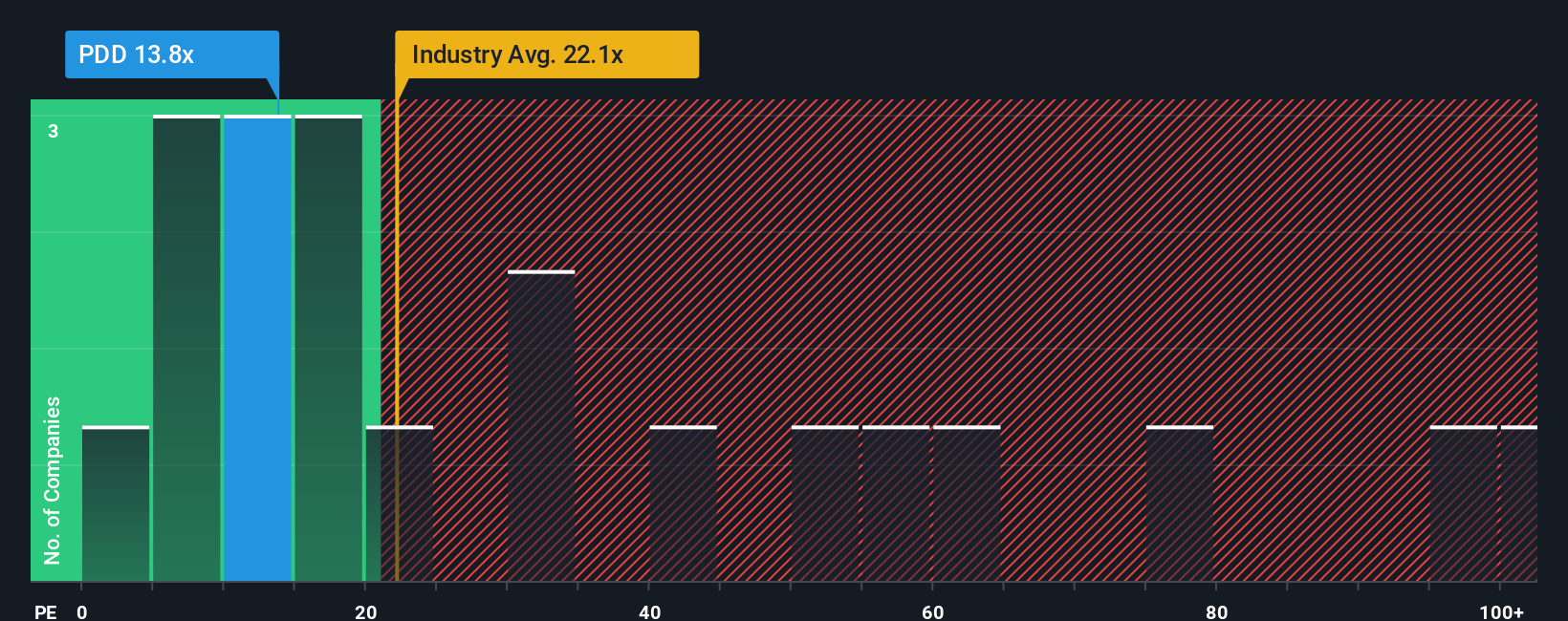

For profitable companies like PDD Holdings, the P/E ratio is a common way to gauge what the market is willing to pay for each dollar of earnings. Investors usually expect higher P/E ratios when they see stronger growth potential or lower risk, and lower P/E ratios when growth expectations are more modest or risks feel higher.

PDD Holdings currently trades on a P/E of 11.75x. That compares with an average P/E of 19.31x for the Multiline Retail industry and a peer group average of 59.55x, so the stock is on a lower multiple than both of these reference points.

Simply Wall St also provides a proprietary “Fair Ratio” of 25.93x for PDD Holdings. This is designed to be more tailored than a simple peer or industry comparison because it factors in company specific elements such as earnings growth expectations, profit margins, risk profile, size and industry. By anchoring on these fundamentals instead of just what others in the sector trade at, the Fair Ratio aims to indicate a more customised P/E level for the business.

Comparing the Fair Ratio of 25.93x with the actual P/E of 11.75x suggests the shares are trading below that fair multiple on these assumptions.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PDD Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company, backed up by their own assumptions for future revenue, earnings, margins and a fair value that can be compared with today’s share price.

On Simply Wall St’s Community page, Narratives are easy to use because they link your view of PDD Holdings to a financial forecast and then to a fair value estimate. They also update automatically when new information such as earnings, company news or analyst revisions is added.

For example, one PDD Holdings Narrative on the platform currently applies assumptions that lead to a fair value of US$165.00 per share, while another uses more cautious inputs and arrives at about US$146.21. This shows how two investors can look at the same business, plug in different expectations and end up with different fair values that they can each compare with the latest price of US$120.97 to guide their own decision on whether the stock looks attractive, fairly priced or expensive.

Do you think there's more to the story for PDD Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com