- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalØrsted (CPSE:ORSTED) Valuation After US Offshore Wind Suspension And Legal Challenge

Ørsted (CPSE:ORSTED) is back in focus after it launched legal challenges against the US suspension of its Revolution Wind and Sunrise Wind projects, putting multi billion dollar investments and timelines under scrutiny for shareholders.

See our latest analysis for Ørsted.

Despite the legal overhang in the US, Ørsted’s recent price action has been mixed, with an 8.9% 7 day share price return and a 23.1% decline in 1 year total shareholder return. This suggests short term momentum alongside a weaker long term record.

If this sort of regulatory headline has you reassessing your watchlist, it could be a good moment to broaden your search with fast growing stocks with high insider ownership.

With Ørsted’s shares still down on a 1 year and multi year view despite recent gains, the key question now is whether legal and regulatory risks are already reflected in the price, or if the market is still assuming stronger future growth.

Price to Sales of 2.5x: Is it justified?

On a P/S of 2.5x at a DKK133.20 share price, Ørsted currently sits in line with the European renewable energy P/S average and below its peer group.

P/S compares the company’s market value to its revenue, which can be useful for loss making businesses where earnings do not yet provide a clear signal.

For Ørsted, a 2.5x P/S suggests investors are paying roughly the same multiple of sales as the wider European renewable energy space, while paying much less than the 5.3x peer average. That gap indicates the market is valuing each unit of Ørsted’s revenue at a discount to similar companies, even though analysts expect revenue to grow at 4.7% per year and earnings to improve from current loss making levels.

Compared with both the industry and peers, the current 2.5x P/S looks restrained rather than aggressive, especially given Ørsted is forecast to become profitable and has revenue growth expected to be slightly ahead of the Danish market.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Sales of 2.5x (ABOUT RIGHT)

However, there are still clear risks, including unresolved US legal disputes and current losses of DKK902m, which could challenge investors’ confidence in the current P/S narrative.

Find out about the key risks to this Ørsted narrative.

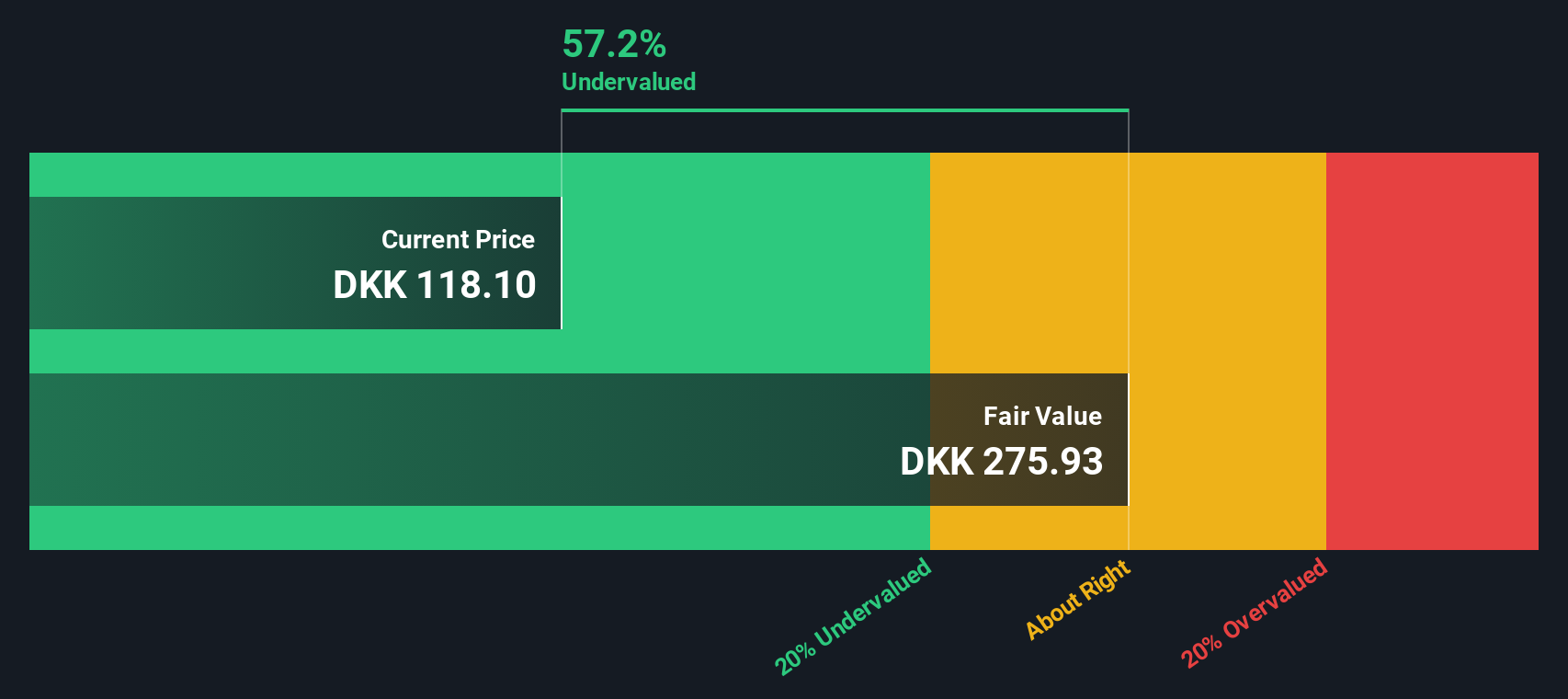

Another View: Our DCF Model Paints A Tougher Picture

While the 2.5x P/S ratio makes Ørsted look fairly priced against peers, our DCF model points in the opposite direction. At a DKK133.20 share price, Ørsted trades above an estimated fair value of DKK81.96, which implies the shares may be overvalued on a cash flow basis.

That gap suggests the market price builds in more optimism than the DCF model does, especially given current losses of DKK902m and ongoing legal and funding questions. It leaves you weighing one key issue: do you trust the revenue based yardstick or the cash flow based one more at this stage?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Ørsted for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Ørsted Narrative

If you look at the numbers and come to a different conclusion, or prefer to test your own assumptions, you can build a personalised Ørsted view in a few minutes with Do it your way.

A great starting point for your Ørsted research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are weighing what to do next after looking at Ørsted, it makes sense to line up a few fresh ideas before the next round of news hits.

- Target reliable income streams by scanning these 12 dividend stocks with yields > 3% that may offer more consistent cash returns than many growth focused names.

- Lean into structural technology shifts by reviewing these 26 AI penny stocks that are building their businesses around artificial intelligence.

- Hunt for potential mispriced opportunities by filtering these 886 undervalued stocks based on cash flows where prices and underlying cash flows look out of sync.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com