- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Manhattan Associates (MANH) Valuation After Mixed Share Performance And Contrasting P/E And DCF Signals

Setting the stage

Manhattan Associates (MANH) has been drawing attention after a mixed stretch in its share performance, with gains over the year to date set against weaker recent returns. This has prompted investors to reassess the current valuation.

See our latest analysis for Manhattan Associates.

At a share price of $173.07, Manhattan Associates reflects a modest year to date share price return of 3.46%, set against a 90 day share price decline of 14.96% and a 1 year total shareholder return of negative 36.49%. This suggests momentum has been fading even after stronger 3 and 5 year total shareholder returns of 42.46% and 53.04%.

If Manhattan Associates has you rethinking your tech exposure, it could be a good moment to widen your search with high growth tech and AI stocks.

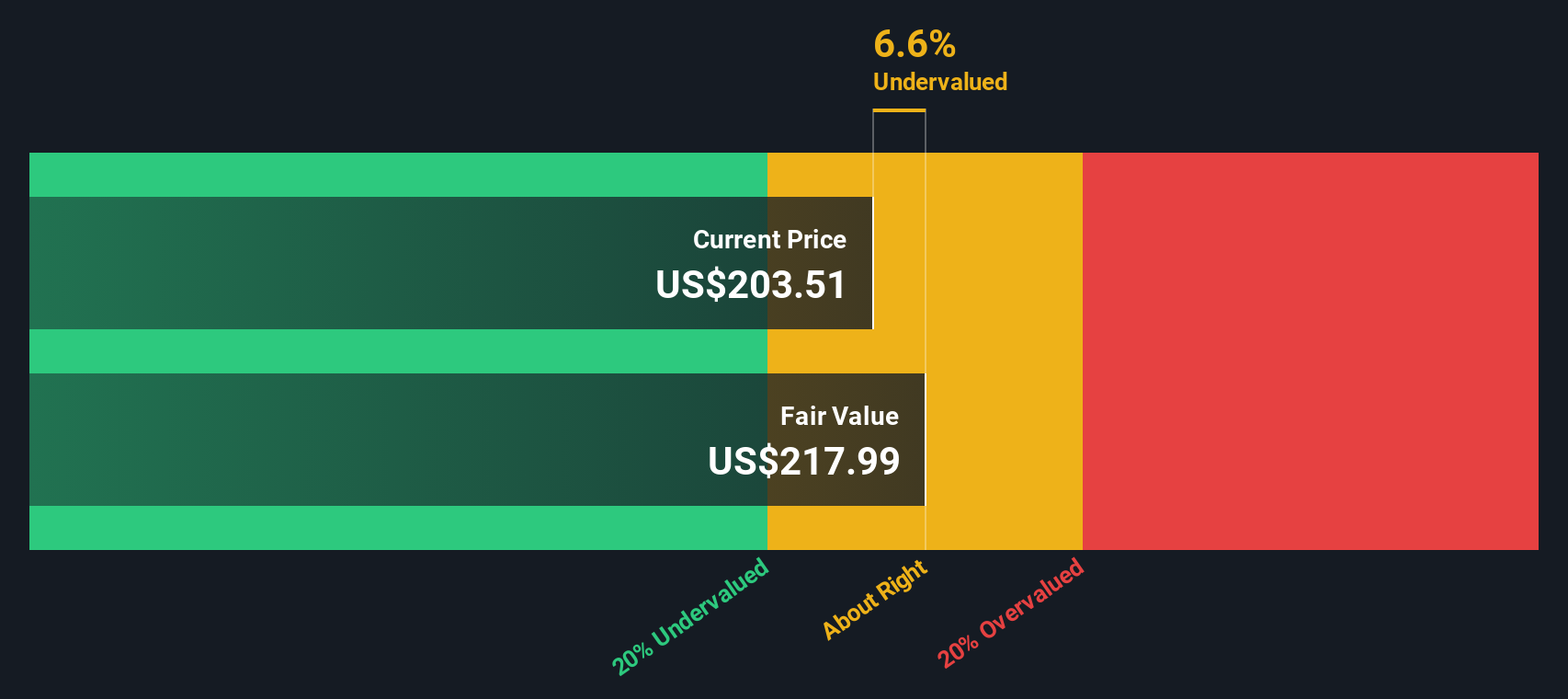

With revenue and net income both growing in the latest year, and the shares trading about 31% below one estimate of intrinsic value, you have to ask: is Manhattan Associates now underappreciated, or is the market already baking in future growth?

Price-to-Earnings of 48.3x: Is it justified?

At a last close of $173.07, Manhattan Associates is trading on a P/E of 48.3x, which screens as expensive against several benchmarks investors often watch.

The P/E ratio compares the current share price to earnings per share and is a common yardstick for software names because profits are already positive and earnings forecasts are available.

For Manhattan Associates, that 48.3x P/E sits above the US Software industry average of 32.7x and above the peer average of 41.2x. This indicates the market is attaching a richer earnings multiple than it does to many comparable companies. It is also higher than an estimated fair P/E of 31.3x, a level the market could move towards if sentiment cools or earnings do not keep pace with expectations.

In other words, the current P/E implies investors are paying a premium for each dollar of earnings compared with both the industry and what the fair ratio estimate suggests might be appropriate over time.

Explore the SWS fair ratio for Manhattan Associates

Result: Price-to-Earnings of 48.3x (OVERVALUED)

However, that premium P/E could quickly look stretched if revenue or net income growth stalls, or if high expectations for its cloud products fade.

Find out about the key risks to this Manhattan Associates narrative.

Another view: DCF suggests a different story

Our DCF model points in the opposite direction to the rich 48.3x P/E. With an estimate of fair value at $252.06 per share versus a current price of $173.07, the shares screen as about 31.3% undervalued. Is the market being too pessimistic, or is the model too generous?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Manhattan Associates for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 886 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Manhattan Associates Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom view of Manhattan Associates in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Manhattan Associates.

Looking for more investment ideas?

If Manhattan Associates has sharpened your thinking, do not stop here. Use these pre built screens to quickly spot other opportunities that might suit your style.

- Target potential deep value situations by checking out these 886 undervalued stocks based on cash flows that may be pricing in more pessimism than their cash flows suggest.

- Zero in on the future of automation and data by scanning these 26 AI penny stocks that sit at the intersection of software, cloud and machine learning.

- Add a different growth angle to your watchlist by reviewing these 79 cryptocurrency and blockchain stocks tied to blockchain infrastructure and digital asset adoption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com