- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalKingsgate Consolidated (ASX:KCN) Valuation Check After New US$25 Million Loan Facility And Refinancing

Kingsgate Consolidated (ASX:KCN) has secured access to a US$25 million loan facility from Nebari Natural Resources Credit Fund II after meeting all conditions, alongside refinancing that reshapes its debt profile and financial flexibility.

See our latest analysis for Kingsgate Consolidated.

The refinancing news comes after a strong run in the shares, with a 30-day share price return of 31.32% and a 90-day share price return of 46.02%. This has contributed to a very large 1-year total shareholder return, while the current A$5.87 share price reflects momentum that has built rather than faded over recent months.

If this kind of move has your attention, it could be a moment to broaden your watchlist and check out fast growing stocks with high insider ownership.

With the shares already up sharply over 1 year and trading at A$5.87, the key question now is simple: is Kingsgate still trading below what the market thinks it is worth, or is future growth already priced in?

Price to Earnings of 52.8x: Is it justified?

On a P/E of 52.8x at a A$5.87 share price, Kingsgate looks expensive compared to its own estimated fair P/E level and sector peers.

The P/E ratio compares the current share price to earnings per share, so a higher multiple usually means the market is placing a richer price on each dollar of profit.

For Kingsgate, the current P/E of 52.8x sits well above the Metals and Mining industry average P/E of 24x and the peer average of 36.9x, which suggests the market is paying a substantial premium. It is also higher than the estimated Fair P/E of 32.2x, a level the market could potentially move towards if expectations and sentiment cool from current settings.

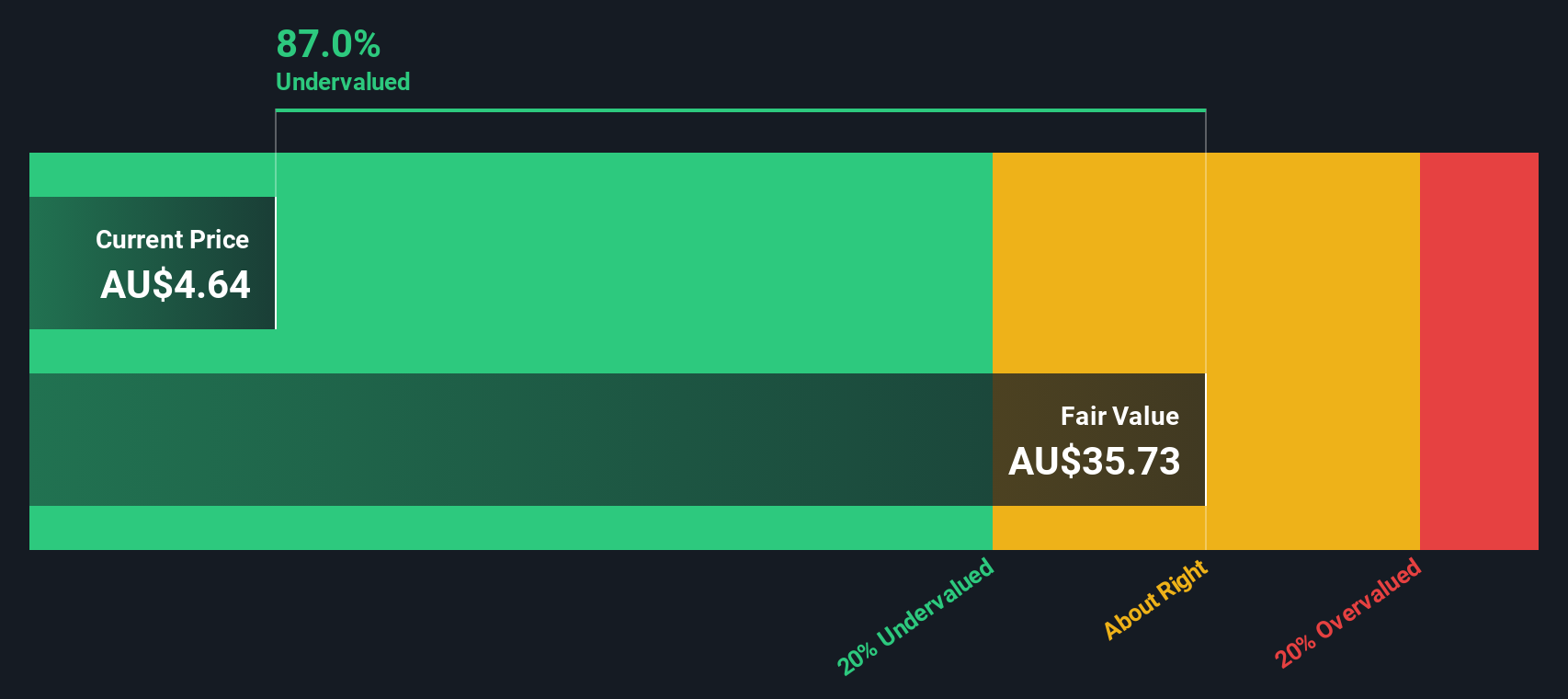

This premium is reinforced by the Simply Wall St DCF work, which indicates the shares are trading at A$5.87 compared to an estimated fair value of A$32.13, implying a very large discount on a cash flow basis even as the earnings multiple looks stretched.

Explore the SWS fair ratio for Kingsgate Consolidated

Result: Price-to-Earnings of 52.8x (OVERVALUED)

However, the premium P/E and reliance on the Chatree Gold Mine mean that any shift in earnings expectations or asset performance could quickly challenge the recent share price strength.

Find out about the key risks to this Kingsgate Consolidated narrative.

Another View: DCF Points the Other Way

If the 52.8x P/E makes Kingsgate look expensive, our DCF model tells a very different story. On that view, A$5.87 compares to an estimated fair value of A$32.13, which suggests a very large gap where the market price sits well below the model output. So which signal do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kingsgate Consolidated for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Kingsgate Consolidated Narrative

If you see the numbers differently or want to stress test your own view, you can pull the data together and craft a full story yourself in just a few minutes, Do it your way.

A great starting point for your Kingsgate Consolidated research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Do not stop with one company when you can quickly scan the market for other clear setups that might better suit your risk profile and goals.

- Spot potential bargains by reviewing these 885 undervalued stocks based on cash flows that the market may be pricing below their cash flow potential.

- Assess these 26 AI penny stocks that are applying artificial intelligence in different parts of the global economy.

- Add fresh growth angles by checking out these 79 cryptocurrency and blockchain stocks tied to blockchain, digital assets and new payment infrastructure themes.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com