- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDoes Ascendis Pharma (ASND) Share Price Reflect Its Strong Multi Year Rally?

- If you are wondering whether Ascendis Pharma's current share price fairly reflects its prospects, you are not alone. Many investors are asking the same question right now.

- The stock recently closed at US$213.28, with returns of 0.0% over 7 days, 3.0% over 30 days, 0.0% year to date and 58.7% over 1 year, while the 3 year and 5 year returns stand at 87.7% and 28.9% respectively.

- Recent coverage has focused on Ascendis Pharma's progress and market position in pharmaceuticals and biotech. This helps frame how investors are thinking about future prospects and risk, and is useful context when looking at a share price that has already moved a lot over multi year periods and may be reacting to changing expectations.

- On our valuation checks, Ascendis Pharma has a value score of 4 out of 6. This suggests some areas of potential undervaluation to unpack. Next we will look at how different valuation approaches view the stock before coming to an even deeper way of thinking about its value by the end of the article.

Approach 1: Ascendis Pharma Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes projections of a company’s future cash flows and discounts them back to today’s value, aiming to estimate what the whole business might be worth right now.

For Ascendis Pharma, the latest twelve month free cash flow stands at a loss of €114 million. Analysts provide detailed estimates out to 2030, with free cash flow projected at €1,568.9 million in that year, and Simply Wall St extrapolates further out to 2035 using a 2 Stage Free Cash Flow to Equity model based on these projections.

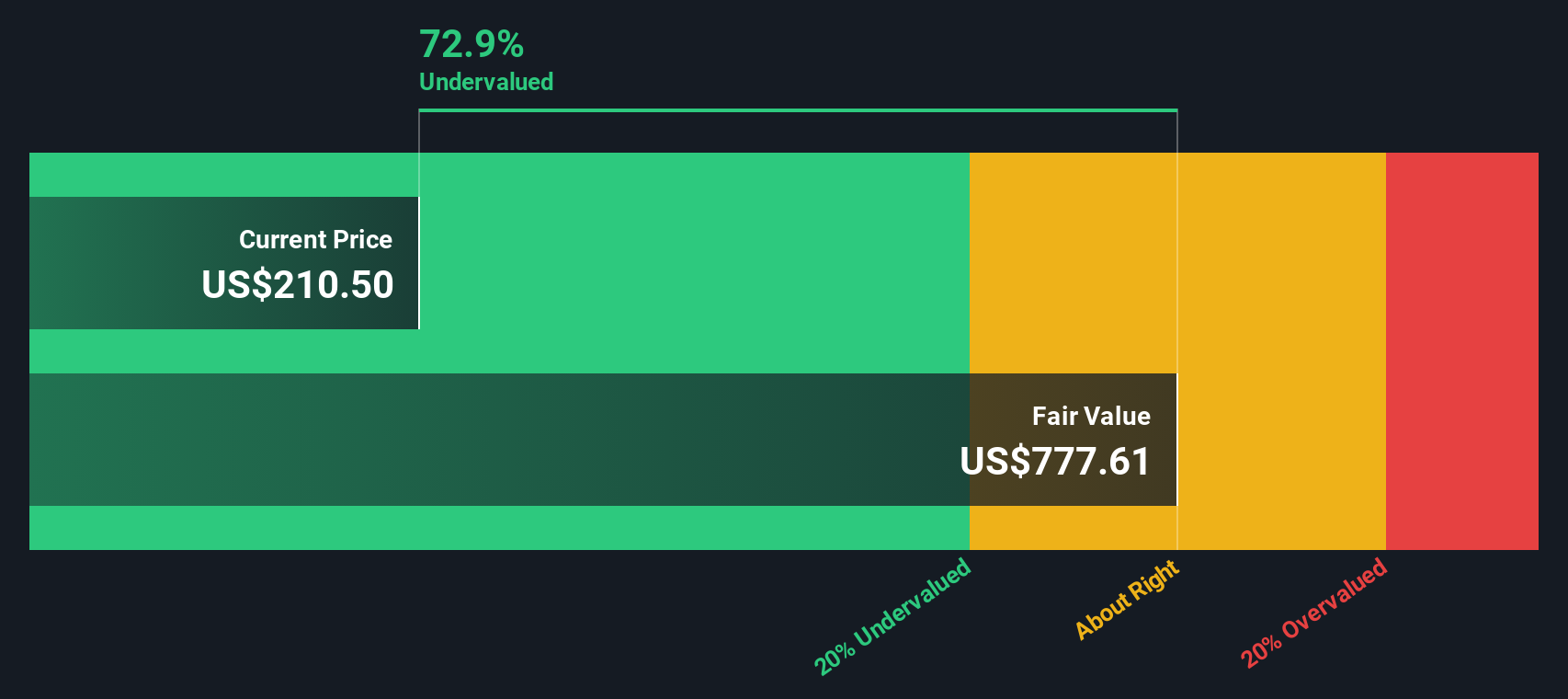

Bringing all those future cash flows back to today using the DCF method gives an estimated intrinsic value of €947.82 per share. Compared with the recent share price of US$213.28, this implies the stock is around 77.5% below that DCF estimate, which points to a large gap between the modelled cash flow value and where the market is currently pricing the shares.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ascendis Pharma is undervalued by 77.5%. Track this in your watchlist or portfolio, or discover 885 more undervalued stocks based on cash flows.

Approach 2: Ascendis Pharma Price vs Sales

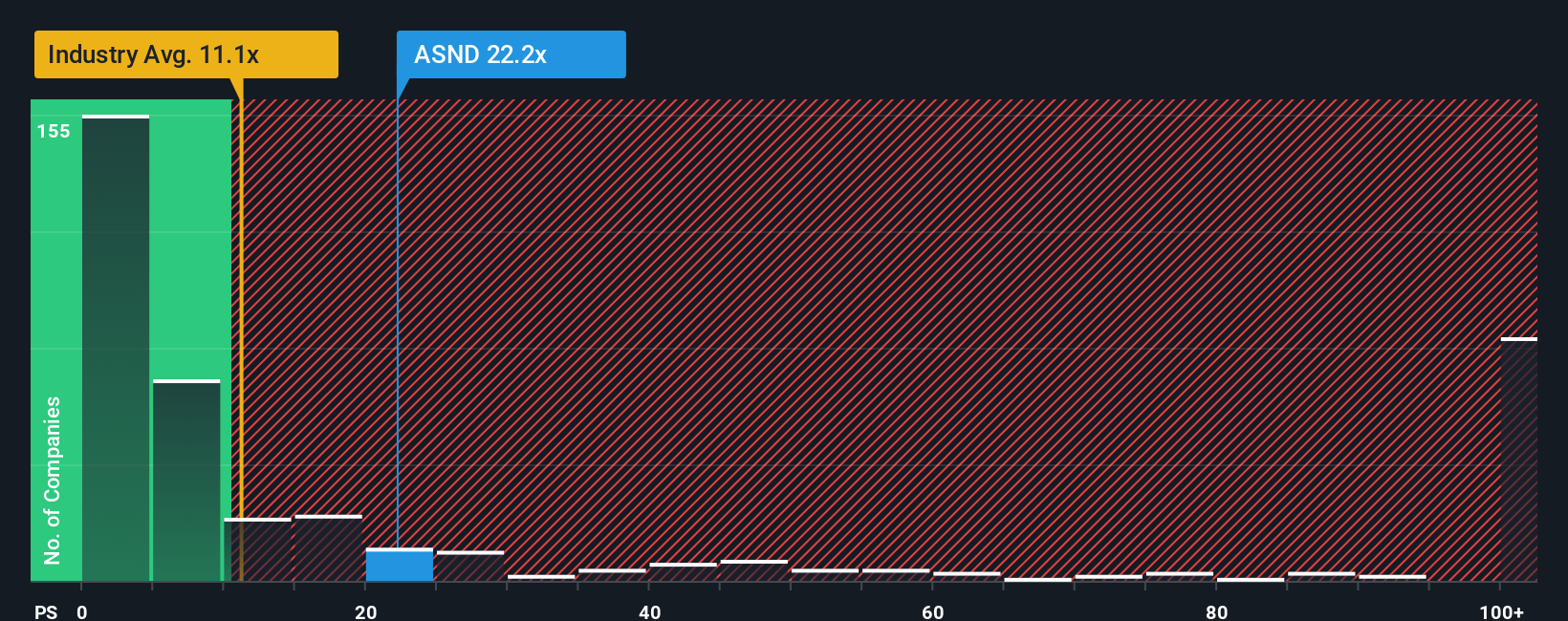

For companies where earnings are not the main focus yet, price to sales, or P/S, is often a useful yardstick because it compares what investors are paying to the revenue the business is generating right now.

What counts as a “normal” P/S ratio depends on how quickly revenue is expected to grow and how risky that growth might be. Higher growth and lower perceived risk can justify a higher multiple, while slower growth or higher risk usually point to a lower, more conservative range.

Ascendis Pharma currently trades on a P/S ratio of 17.33x. This is above the Biotechs industry average of 11.66x and below the peer group average of 28.67x. Simply Wall St’s Fair Ratio, which estimates what the P/S should be once factors like growth outlook, profitability, industry, market cap and company specific risks are considered, is 16.63x.

Because the Fair Ratio adjusts for these company specific characteristics, it can be more informative than a simple comparison with industry or peer averages alone.

Compared with the Fair Ratio of 16.63x, Ascendis Pharma’s current 17.33x P/S suggests the shares are trading somewhat above that modelled level.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1450 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ascendis Pharma Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. These let you write a simple story about Ascendis Pharma that connects your view of its drugs, risks and opportunities to a set of revenue, earnings and margin assumptions. Narratives then roll those assumptions into a forecast and fair value, and compare that fair value with today’s share price so you can judge whether it looks attractive or stretched. All of this happens inside Simply Wall St’s Community page, where Narratives are updated automatically when new news or earnings arrive. One investor might build a very optimistic Ascendis Pharma Narrative around strong uptake of YORVIPATH and SKYTROFA, with higher 2028 earnings and a fair value closer to the US$306.97 bullish target. Another might focus on pricing pressure, competition and execution risks, and settle on assumptions that line up more with the US$202.53 bearish target instead.

Do you think there's more to the story for Ascendis Pharma? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com