- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalPowell Industries (POWL) Valuation Check As Investor Interest Builds Before Early February Earnings

Powell Industries (POWL) has drawn fresh attention after its shares moved 10.6% higher on the first U.S. trading day of 2026, with investors positioning in advance of an early February earnings update.

See our latest analysis for Powell Industries.

The early year move has come on top of a 9.9% 7 day share price return and a 14.1% 90 day share price return, while the 1 year total shareholder return of 52.5% and very large 3 and 5 year total shareholder returns suggest that momentum has been building over time as investors reassess Powell Industries' growth potential and risks around its order book, margins and AI infrastructure exposure.

If Powell Industries' recent jump has your attention, this could be a good moment to broaden your watchlist with other aerospace and defense stocks that may be reacting to similar themes in industrial demand and infrastructure spending.

With the shares at US$360 and Powell Industries carrying a low value score of 2 plus an analyst price target of US$267.26, you have to ask: is this a stretched story, or is the market still underpricing future growth?

Most Popular Narrative: 34% Overvalued

With Powell Industries last closing at US$360 and the most followed narrative pointing to fair value of US$269.26, you are looking at a clear valuation gap that hinges on how sustainable current earnings power and discount rates really are.

The analysts have a consensus price target of $245.927 for Powell Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $280.0, and the most bearish reporting a price target of just $224.78.

Curious what kind of mid single digit revenue growth, margin compression and higher required return still point to a lower fair value than today’s price? The core assumptions around future earnings power and the P/E the company might command are sharper than you might expect, and the spread between bullish and bearish views is wider than headlines suggest.

Result: Fair Value of $269.26 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, if revenue visibility, margin trends or the impact of investments like Remsdaq and the Houston capacity buildout track better than projected, today’s case for overvaluation could soften.

Find out about the key risks to this Powell Industries narrative.

Another View: Earnings Power Versus Price Tag

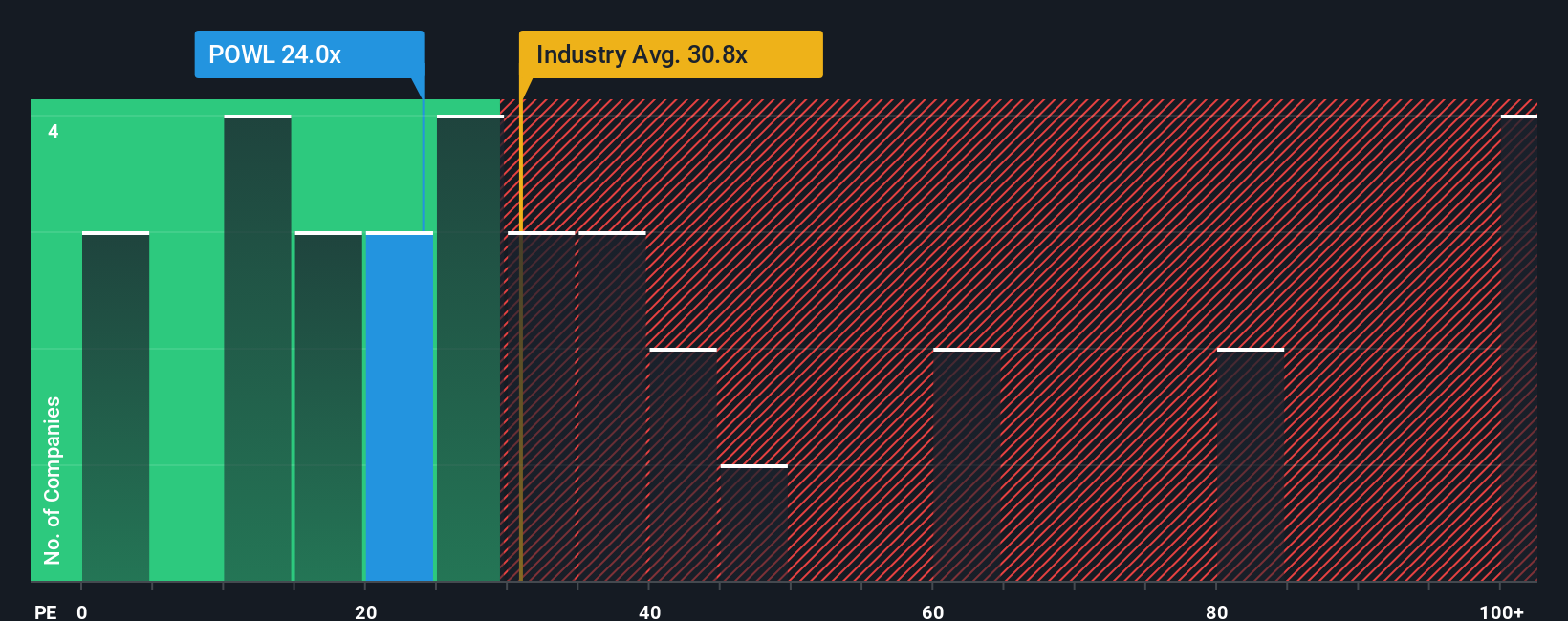

So far the focus has been on fair value estimates around US$269.26, which frame Powell Industries as overvalued at US$360. Yet on a straight P/E basis the picture is more mixed.

Powell trades on a P/E of 24.1x. That is below the US Electrical industry average of 30.8x and well under the peer average of 52x, which points to a cooler rating than many sector names. At the same time, it sits above the fair ratio of 21.1x that our work suggests the market could gravitate toward over time, which hints at valuation risk if expectations reset.

Put simply, the market is charging a premium to that fair ratio, while still pricing Powell at a discount to many industry and peer companies. The question for you is whether current earnings quality and growth expectations justify paying up from 21.1x, or whether that gap eventually closes from above.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Powell Industries Narrative

If you see the data differently or want to stress test these assumptions yourself, it only takes a few minutes to build your own view: Do it your way

A great starting point for your Powell Industries research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Powell Industries is on your radar, do not stop there; broaden your search now so you do not miss other opportunities that could fit your style.

- Target potential value opportunities by scanning these 100+ undervalued stocks based on cash flows that may align better with the prices you are willing to pay.

- Ride fast moving themes in technology by checking out these 26 AI penny stocks where AI is a core part of the business story.

- Tap into income focused opportunities by reviewing these 11 dividend stocks with yields > 3% that could support a steadier stream of cash returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com