- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalJanuary 2026's Top Growth Companies With Insider Stakes

As the Dow Jones and S&P 500 reach new all-time highs, driven by a surge in data storage stocks amid an AI rally, investors are keenly observing the landscape for promising growth opportunities. In this buoyant market environment, companies with high insider ownership often attract attention due to their potential alignment of interests between management and shareholders, making them compelling candidates for those looking to capitalize on growth trends.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| TNL Mediagene (TNMG) | 23% | 148.8% |

| Super Micro Computer (SMCI) | 13.9% | 50.7% |

| StubHub Holdings (STUB) | 14.1% | 59% |

| SES AI (SES) | 12% | 68.9% |

| Prairie Operating (PROP) | 32.2% | 100% |

| Niu Technologies (NIU) | 37.2% | 93.7% |

| Credo Technology Group Holding (CRDO) | 10.1% | 30.7% |

| Corcept Therapeutics (CORT) | 11.5% | 43.6% |

| Bitdeer Technologies Group (BTDR) | 33.4% | 135.5% |

| Astera Labs (ALAB) | 10.5% | 29.0% |

Let's uncover some gems from our specialized screener.

Atour Lifestyle Holdings (ATAT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Atour Lifestyle Holdings Limited, with a market cap of $5.52 billion, operates through its subsidiaries to develop lifestyle brands centered around hotel offerings in the People’s Republic of China.

Operations: Atour Lifestyle Holdings generates revenue primarily from its Atour Group segment, which reported CN¥9.09 billion.

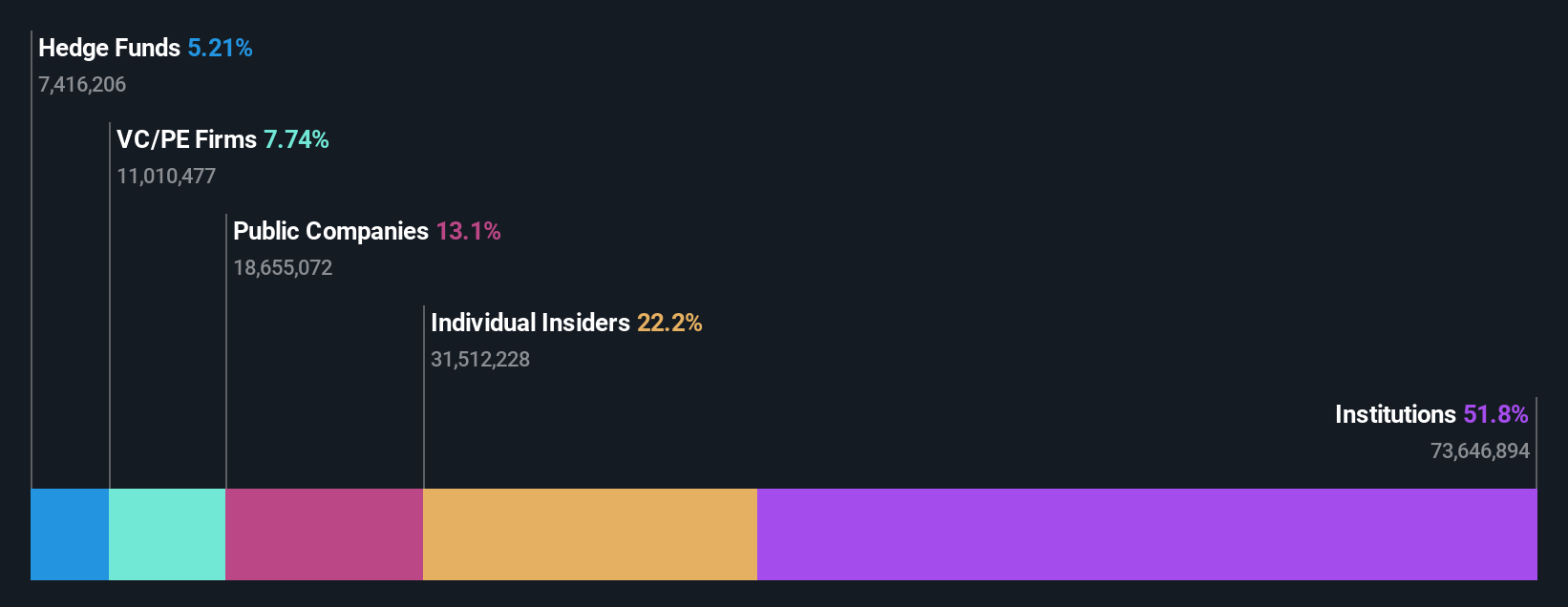

Insider Ownership: 18%

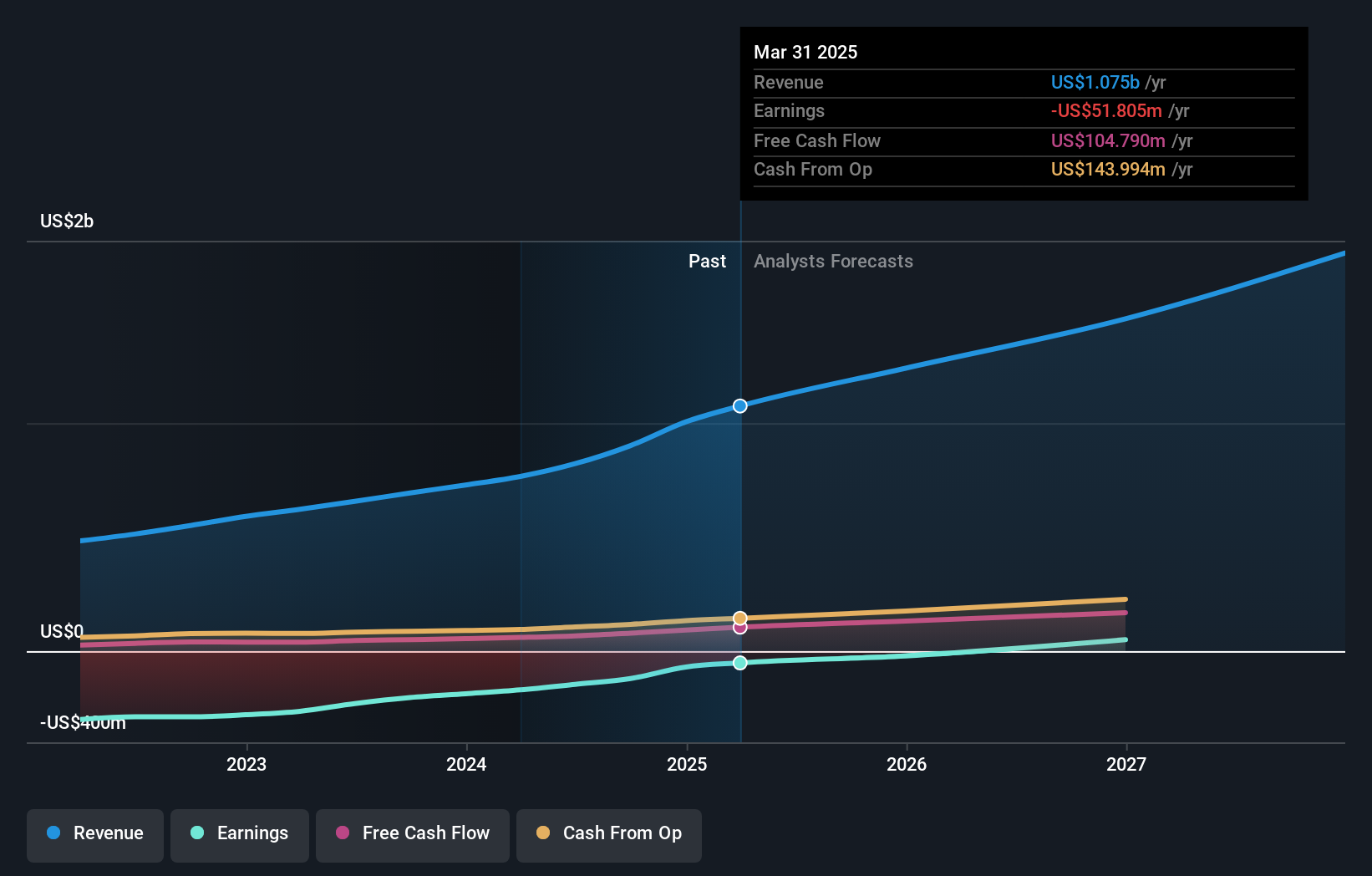

Atour Lifestyle Holdings demonstrates significant growth potential, with earnings expected to grow 24.6% annually, surpassing the US market average. Despite a slower revenue growth forecast of 16.3%, it remains above market expectations. Recent financials show robust performance with net income rising to CNY 473.72 million in Q3 2025, up from CNY 384.39 million a year prior. The company also declared substantial dividends totaling approximately US$108 million for 2025, reflecting strong cash flow management and shareholder commitment amidst leadership changes on its board.

- Click here to discover the nuances of Atour Lifestyle Holdings with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Atour Lifestyle Holdings is trading behind its estimated value.

Klarna Group (KLAR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Klarna Group plc is a digital bank and flexible payments provider operating in the United Kingdom, the United States, Germany, Sweden, and internationally with a market cap of $11.04 billion.

Operations: Klarna generates revenue primarily from its data processing segment, which amounts to $3.21 billion.

Insider Ownership: 20.1%

Klarna Group is navigating a complex landscape with its recent IPO facing legal challenges over alleged misstatements. Despite this, Klarna's growth trajectory is supported by innovative product launches like the Agentic Product Protocol and strategic partnerships with Apple Pay and Lufthansa. The company aims for profitability within three years, forecasting earnings growth of 52.7% annually. While revenue growth at 17.9% lags behind some peers, it still outpaces the broader US market expectations of 10.5%.

- Click here and access our complete growth analysis report to understand the dynamics of Klarna Group.

- Our valuation report here indicates Klarna Group may be overvalued.

Zeta Global Holdings (ZETA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zeta Global Holdings Corp. operates an omnichannel data-driven cloud platform offering consumer intelligence and marketing automation software to enterprises globally, with a market cap of approximately $5.33 billion.

Operations: The company generates revenue of $1.22 billion from its Internet Software & Services segment.

Insider Ownership: 16.4%

Zeta Global Holdings is poised for significant growth, with revenue forecasted to grow 17.4% annually, surpassing the US market's average. The company recently raised its earnings guidance, projecting a robust 34% increase in 2026 revenue. Despite no substantial insider buying in recent months, Zeta's strategic initiatives like the Athena AI platform enhance its market offerings. Trading below fair value and expected to achieve profitability within three years, Zeta remains a compelling growth story amidst high insider ownership dynamics.

- Dive into the specifics of Zeta Global Holdings here with our thorough growth forecast report.

- According our valuation report, there's an indication that Zeta Global Holdings' share price might be on the cheaper side.

Key Takeaways

- Get an in-depth perspective on all 212 Fast Growing US Companies With High Insider Ownership by using our screener here.

- Curious About Other Options? The end of cancer? These 29 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com