- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalA Look At NewAmsterdam Pharma (NAMS) Valuation As Late Stage CETP Trial Progress Draws Investor Attention

NewAmsterdam Pharma (NasdaqGM:NAMS) has drawn fresh attention after reporting progress in its late stage clinical trials for its CETP inhibitor. The treatment produced significant LDL reductions without the side effects seen in competing treatments.

See our latest analysis for NewAmsterdam Pharma.

The clinical progress has come after a period of mixed share price returns, with a recent 1 day share price return of 1.61% and a year to date share price return decline of 3.35%. At the same time, the 1 year total shareholder return of 30.65% and 3 year total shareholder return above 2x suggest that longer term momentum has been strong.

If this kind of late stage pipeline story interests you, it could be worth widening the lens to other healthcare stocks that are attempting to reshape treatment options.

With a recent pullback, a value score of 4, a large intrinsic discount, and a price target above the last close, the key question is whether NewAmsterdam is still undervalued or if the market already prices in future growth.

Price to Book of 5.3x: Is it justified?

On a P/B of 5.3x, NewAmsterdam trades close to the peer average of 5.5x, yet well above the wider US biotech group on 2.7x.

P/B compares the market value of the company to its accounting book value and is often used for early stage or loss making biotechs where earnings based ratios are less useful.

For NewAmsterdam, a 5.3x P/B sits slightly under its direct peer average of 5.5x. This points to the market assigning a broadly similar valuation per dollar of net assets to comparable companies.

However, the same 5.3x multiple is much higher than the broader US biotechs industry on 2.7x, so investors are paying a clear premium multiple relative to the sector for this balance sheet.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-book of 5.3x (ABOUT RIGHT)

However, there are clear pressure points here, including clinical trial outcomes for obicetrapib and the current net income loss of US$221.073 million.

Find out about the key risks to this NewAmsterdam Pharma narrative.

Another View: What Our DCF Model Suggests

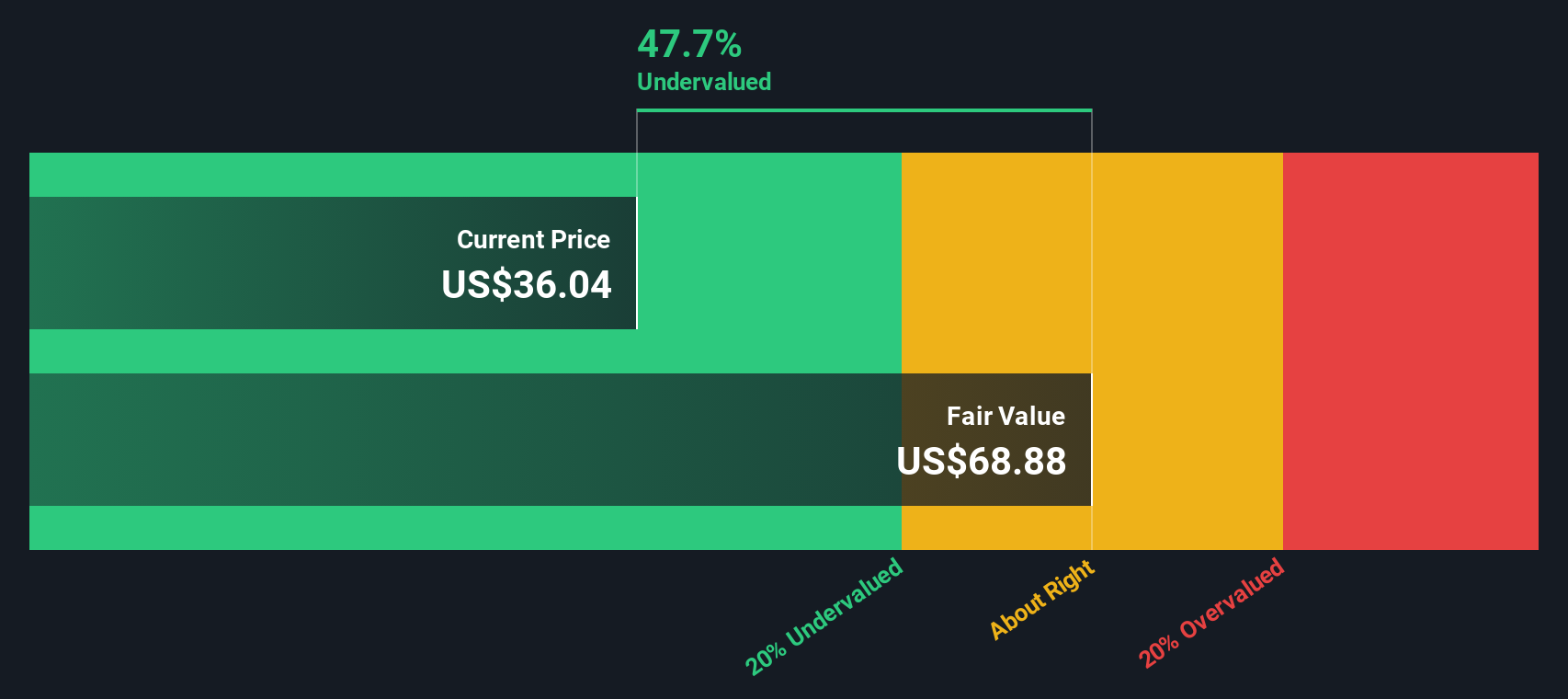

The P/B of 5.3x suggests NewAmsterdam is roughly in line with close peers, but the SWS DCF model points in a very different direction. On that framework, the shares trade at a very large discount to an estimated fair value of US$259.73 per share.

That gap implies the market could be heavily discounting execution risk around trials, funding and long term profitability, or the DCF inputs could simply be too optimistic. The key question is which story you trust more: the balance sheet multiple or the cash flow model?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NewAmsterdam Pharma for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 877 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own NewAmsterdam Pharma Narrative

If you see the numbers differently or want to test your own assumptions, you can build and compare a custom thesis in just a few minutes using Do it your way.

A great starting point for your NewAmsterdam Pharma research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If NewAmsterdam has caught your attention, do not stop here. Broaden your watchlist and let data driven shortlists surface opportunities you might otherwise miss.

- Spot potential value opportunities early by checking out these 877 undervalued stocks based on cash flows, which is built around discounted cash flow signals and balance sheet strength.

- Learn more about major tech shifts by scanning these 25 AI penny stocks, which links artificial intelligence themes with listed companies across different sectors.

- Explore income focused ideas with these 11 dividend stocks with yields > 3%, which highlights companies offering yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com