- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalShould Wolters Kluwer’s Expanded AI Workflow Tools Reshape Its Recurring Revenue Story (ENXTAM:WKL)?

- In recent months, Wolters Kluwer has drawn fresh attention for expanding AI-powered capabilities across its professional information and software platforms in health, tax, accounting, legal, and compliance workflows.

- This renewed focus on embedding AI directly into expert workflows highlights how Wolters Kluwer is aiming to deepen its role in customers’ everyday decision-making processes.

- Next, we’ll examine how Wolters Kluwer’s AI-infused software push may influence its investment narrative built around recurring revenues.

These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Wolters Kluwer Investment Narrative Recap

To own Wolters Kluwer, you need to believe its shift toward AI-enhanced, cloud-based expert tools can keep reinforcing a high share of recurring revenues while offsetting drag from declining print and lumpy transactional streams. The recent AI product rollouts look additive to that recurring revenue story, but do not fundamentally change the near term catalyst around SaaS adoption or the key risks tied to competition and on-premise to cloud migration.

Among recent announcements, the preparation to launch CCH Axcess Advisor, an advisory-first tax and accounting platform built on Expert AI, is especially relevant. It ties directly into the company’s effort to deepen its role in clients’ daily workflows, potentially supporting subscription stickiness and pricing power at a time when open-access and AI-native competitors are pushing hard on professional users’ budgets.

Yet behind the appeal of AI enabled tools, investors should be aware of the growing risk of intensifying competition and potential pressure on...

Read the full narrative on Wolters Kluwer (it's free!)

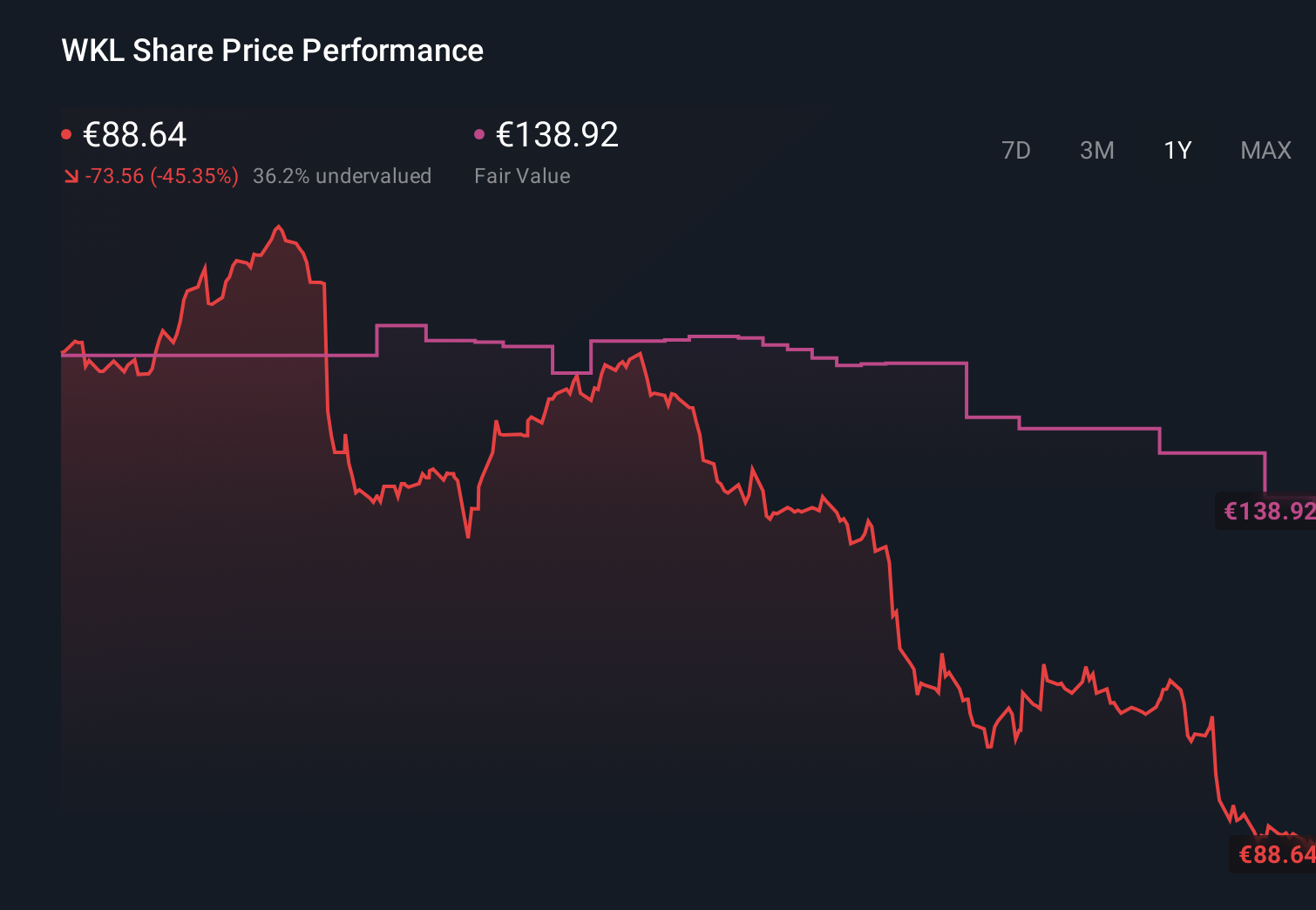

Wolters Kluwer's narrative projects €7.1 billion revenue and €1.4 billion earnings by 2028. This requires 5.2% yearly revenue growth and roughly a €0.3 billion earnings increase from €1.1 billion today.

Uncover how Wolters Kluwer's forecasts yield a €138.00 fair value, a 52% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s eight fair value estimates for Wolters Kluwer span roughly €75.79 to €146, underlining how far apart individual views can be. Against this backdrop, the company’s push into AI infused SaaS platforms puts extra focus on how securely its recurring revenues can hold up under competitive and technological pressure, which readers may want to compare with these varied community perspectives.

Explore 8 other fair value estimates on Wolters Kluwer - why the stock might be worth 16% less than the current price!

Build Your Own Wolters Kluwer Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wolters Kluwer research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wolters Kluwer research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wolters Kluwer's overall financial health at a glance.

Looking For Alternative Opportunities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 39 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com