- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSome Shareholders Feeling Restless Over Svenska Cellulosa Aktiebolaget SCA (publ)'s (STO:SCA B) P/E Ratio

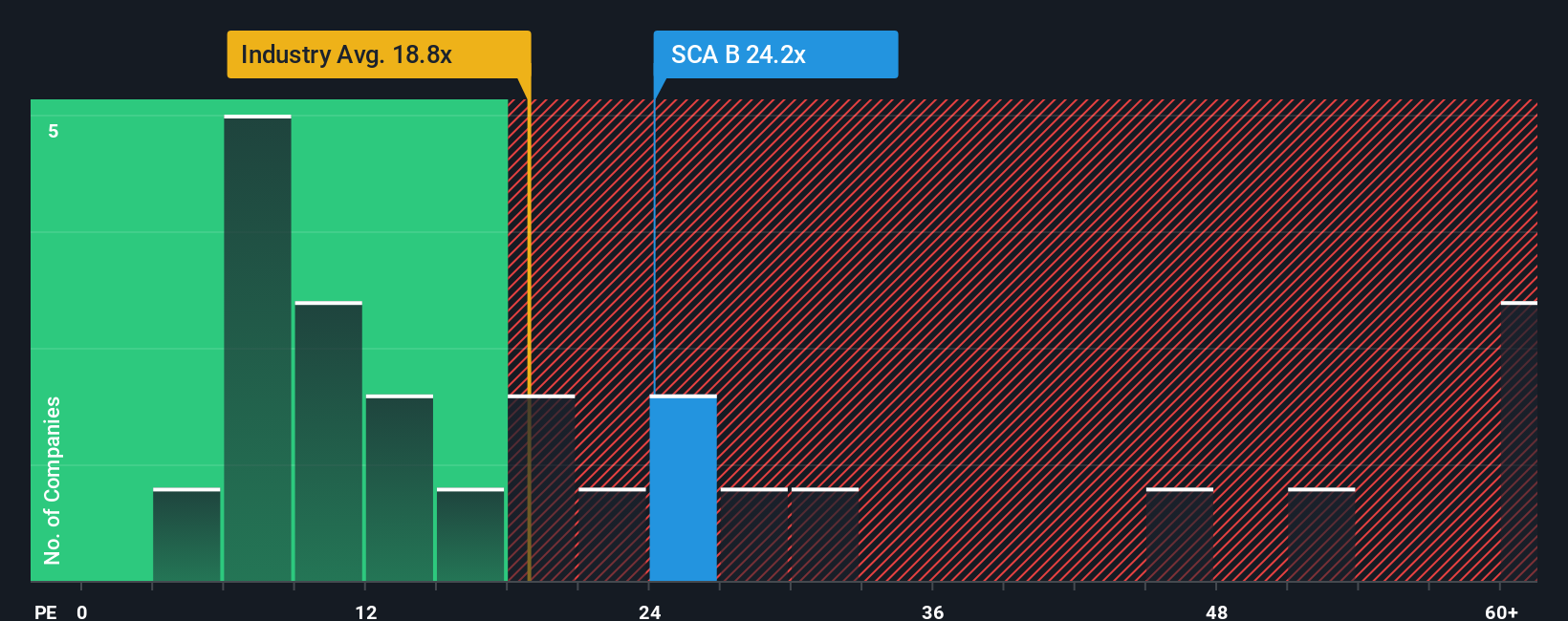

It's not a stretch to say that Svenska Cellulosa Aktiebolaget SCA (publ)'s (STO:SCA B) price-to-earnings (or "P/E") ratio of 24.2x right now seems quite "middle-of-the-road" compared to the market in Sweden, where the median P/E ratio is around 22x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Svenska Cellulosa Aktiebolaget could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to strengthen positively, which has kept the P/E from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

View our latest analysis for Svenska Cellulosa Aktiebolaget

What Are Growth Metrics Telling Us About The P/E?

In order to justify its P/E ratio, Svenska Cellulosa Aktiebolaget would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 3.7%. As a result, earnings from three years ago have also fallen 53% overall. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next three years should generate growth of 4.2% per annum as estimated by the twelve analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 21% per year, which is noticeably more attractive.

In light of this, it's curious that Svenska Cellulosa Aktiebolaget's P/E sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Bottom Line On Svenska Cellulosa Aktiebolaget's P/E

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Svenska Cellulosa Aktiebolaget's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. Right now we are uncomfortable with the P/E as the predicted future earnings aren't likely to support a more positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Svenska Cellulosa Aktiebolaget that you need to be mindful of.

Of course, you might also be able to find a better stock than Svenska Cellulosa Aktiebolaget. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.