A Look At Estée Lauder (EL) Valuation After Raymond James Strong Buy Upgrade

Raymond James’ upgrade of Estée Lauder Companies (EL) to Strong Buy puts fresh attention on the company’s turnaround story, with the firm highlighting better U.S. market share trends and recovering category growth in China.

See our latest analysis for Estée Lauder Companies.

The upgrade comes after a period where the 90-day share price return of 12.95% suggests improving momentum, while the 1-year total shareholder return of 48.40% contrasts with weak 3 and 5 year total shareholder returns, hinting at a long term story that is still being repaired.

If Estée Lauder’s reset has your attention, it could be a good moment to widen your watchlist with quality healthcare stocks that sit elsewhere in the consumer and health ecosystem.

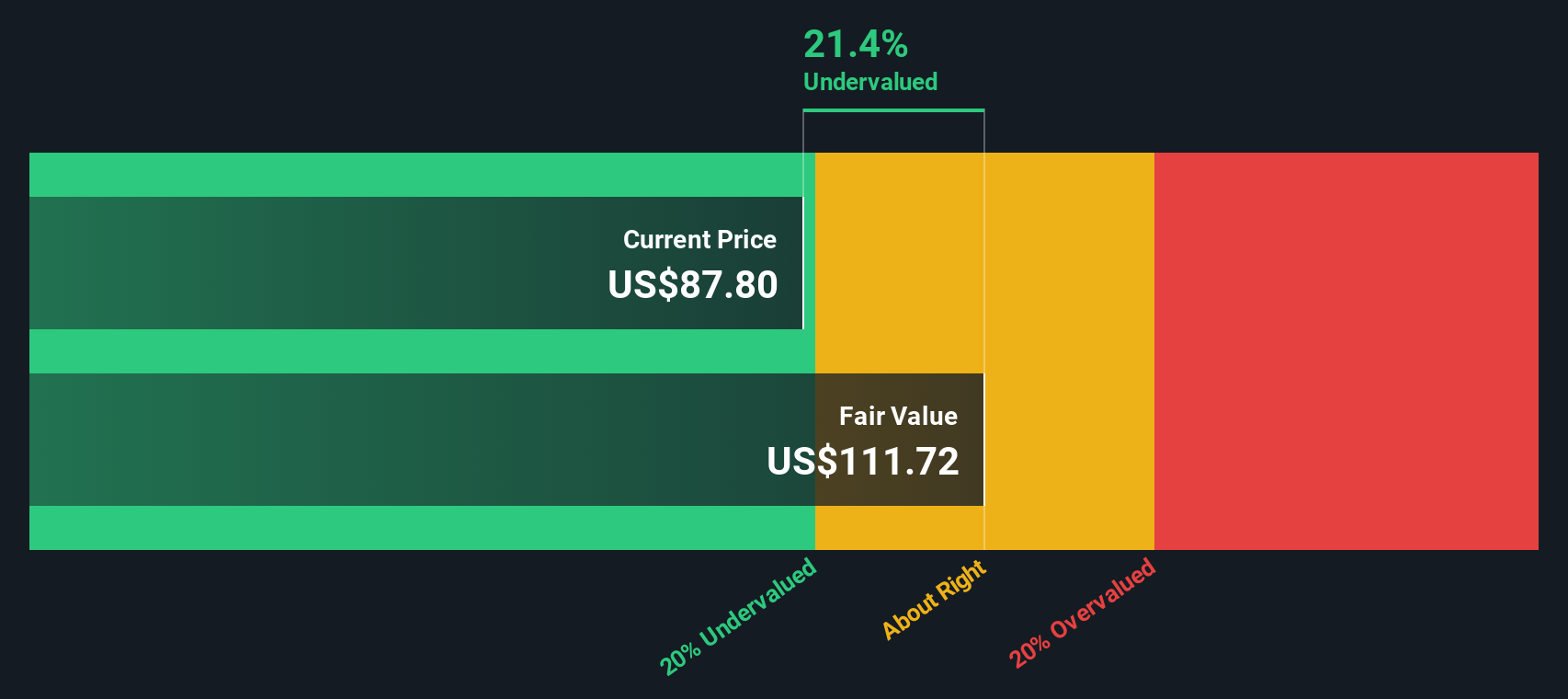

So with Estée Lauder trading around US$108, sitting close to its average analyst target and a modest intrinsic discount, are you looking at a genuine reset opportunity here, or has the market already priced in the turnaround?

Most Popular Narrative: 3.7% Overvalued

With Estée Lauder last closing at US$108.16 against a narrative fair value of about US$104.30, the current setup leans slightly ahead of that story.

• The analysts have a consensus price target of $91.435 for Estée Lauder Companies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $120.0, and the most bearish reporting a price target of just $61.0.

Curious what kind of revenue lift, margin rebuild and future P/E multiple have to line up to support that valuation gap? The narrative spells it out.

Result: Fair Value of $104.30 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still real pressure points here, including ongoing travel retail weakness and high restructuring and impairment costs that could keep earnings and margins under strain.

Find out about the key risks to this Estée Lauder Companies narrative.

Another View: DCF Points to a Slight Discount

While the narrative fair value of about US$104.30 suggests Estée Lauder is 3.7% overvalued, our DCF model points in a slightly different direction. With shares at US$108.16 versus an estimate of US$109.83, the stock sits roughly 1.5% below that fair value. This raises the question of which story you put more weight on.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Estée Lauder Companies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 882 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Estée Lauder Companies Narrative

If you see the numbers differently or simply prefer to test your own assumptions, you can shape a full Estée Lauder view in minutes: Do it your way.

A great starting point for your Estée Lauder Companies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready For Your Next Investment Idea?

If Estée Lauder is just one piece of your watchlist, now is the time to broaden your opportunities and stress test your thinking across different themes.

- Spot potential mispricings by checking out these 882 undervalued stocks based on cash flows that may offer stronger cash flow support for their current prices.

- Ride powerful technology shifts by scanning these 25 AI penny stocks that connect AI growth stories with listed companies.

- Lock in the income angle by reviewing these 14 dividend stocks with yields > 3% that may support a more consistent return profile in your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com