- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Mitsubishi UFJ Financial Group (TSE:8306) Valuation After Share Buybacks And Higher Net Interest Income Expectations

Investor attention on Mitsubishi UFJ Financial Group (TSE:8306) has picked up after the bank completed a ¥115,292.29 million share buyback, repurchasing 47,059,100 shares, or 0.41% of its outstanding equity.

See our latest analysis for Mitsubishi UFJ Financial Group.

The buyback sits alongside a 1-year total shareholder return of 41.39% and a very large 5-year total shareholder return, while the 90-day share price return of 11.92% suggests positive momentum has been building recently.

If you are looking beyond large banks, this could be a good moment to broaden your search with fast growing stocks with high insider ownership.

So with a ¥2,625 share price, a 27% intrinsic discount estimate and recent returns already very strong, is Mitsubishi UFJ still offering value or is the market already pricing in the next leg of growth?

Most Popular Narrative: 6.3% Overvalued

With Mitsubishi UFJ Financial Group last closing at ¥2,625 against a narrative fair value of ¥2,470, the current price sits slightly above that estimate, which rests on detailed forecasts for earnings, margins and capital returns.

The analysts have a consensus price target of ¥2317.273 for Mitsubishi UFJ Financial Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥2700.0, and the most bearish reporting a price target of just ¥1830.0.

Curious what kind of earnings climb and margin shift would justify that fair value even with a lower future P/E and discount rate? The most followed narrative lays out a specific path for revenue, profitability and share count that sits behind those numbers. If you want to see exactly how those moving parts fit together, the full narrative joins them into one clear valuation story.

Result: Fair Value of ¥2,470 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can shift quickly if net interest income comes under pressure from a reverse U.S. yield curve, or if equity security sales fall short of assumptions.

Find out about the key risks to this Mitsubishi UFJ Financial Group narrative.

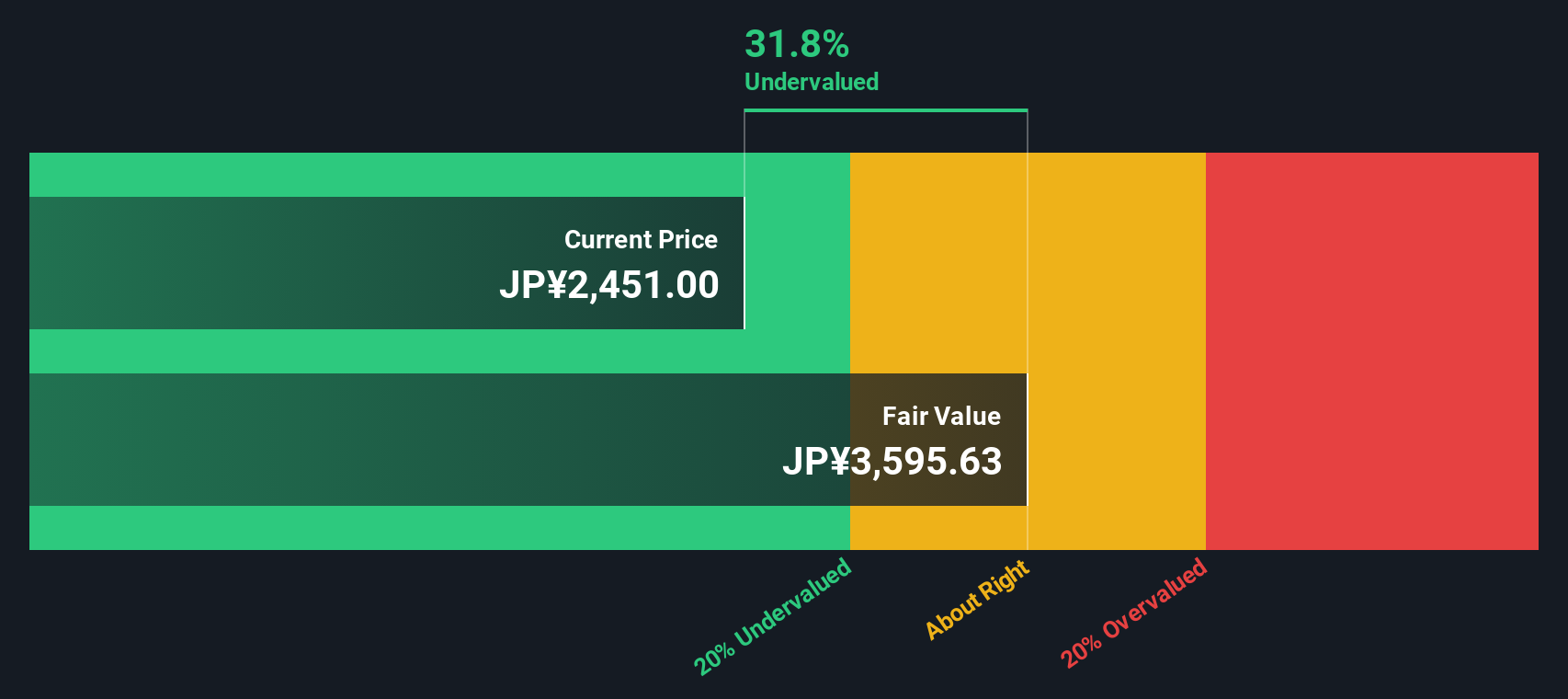

Another View: DCF Points In The Opposite Direction

While the narrative fair value of ¥2,470 suggests Mitsubishi UFJ Financial Group is about 6.3% overvalued, the SWS DCF model points the other way. With a fair value estimate of ¥3,612.52 versus the current ¥2,625 price, it indicates the shares trade at a 27.3% discount. Which story do you think fits your expectations better?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Mitsubishi UFJ Financial Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 880 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Mitsubishi UFJ Financial Group Narrative

If you look at these numbers and come to a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your Mitsubishi UFJ Financial Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about sharpening your portfolio, do not stop at one stock. Use the screener to quickly surface fresh ideas aligned with what you care about most.

- Target potential value opportunities by scanning these 880 undervalued stocks based on cash flows that line up with your preferred risk and return profile.

- Chase growth themes by checking out these 25 AI penny stocks positioned around artificial intelligence trends you want exposure to.

- Build a potential income stream by reviewing these 14 dividend stocks with yields > 3% that might complement or balance your existing holdings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com