Will Philip Morris's (PM) ESOP-Funded Shift to Smoke-Free Products Reshape Its Core Investment Narrative?

- In late 2025, Philip Morris International Inc. filed a shelf registration for an employee stock ownership plan–related offering of 500,000 common shares, totaling about US$80.53 million.

- This ESOP-linked issuance underscores how Philip Morris International is tying employee incentives to its transition toward smoke-free and alternative nicotine products such as Zyn and Iqos Iluma.

- We’ll now examine how aligning employee ownership with growth in products like Zyn and the pending Iqos Iluma launch may influence Philip Morris International’s investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to believe its shift toward smoke free products like Zyn and the pending Iqos Iluma launch can offset pressure on traditional cigarettes, illicit trade and regulation. The new US$80.53 million ESOP shelf registration does not materially change those near term catalysts or the key risk that smoke free growth could slow or face regulatory setbacks.

Among recent announcements, the reaffirmed 2025 earnings guidance (diluted EPS of US$7.39 to US$7.49) is most relevant here, because it frames how much flexibility PMI has to fund product launches, regulation heavy markets and employee incentives like this ESOP. Together, these updates help you judge whether the smoke free transition is being supported by both capital allocation and operational delivery.

But while the smoke free pivot looks promising, investors should also be aware of how tightening regulation could affect products like Iqos Iluma and Zyn...

Read the full narrative on Philip Morris International (it's free!)

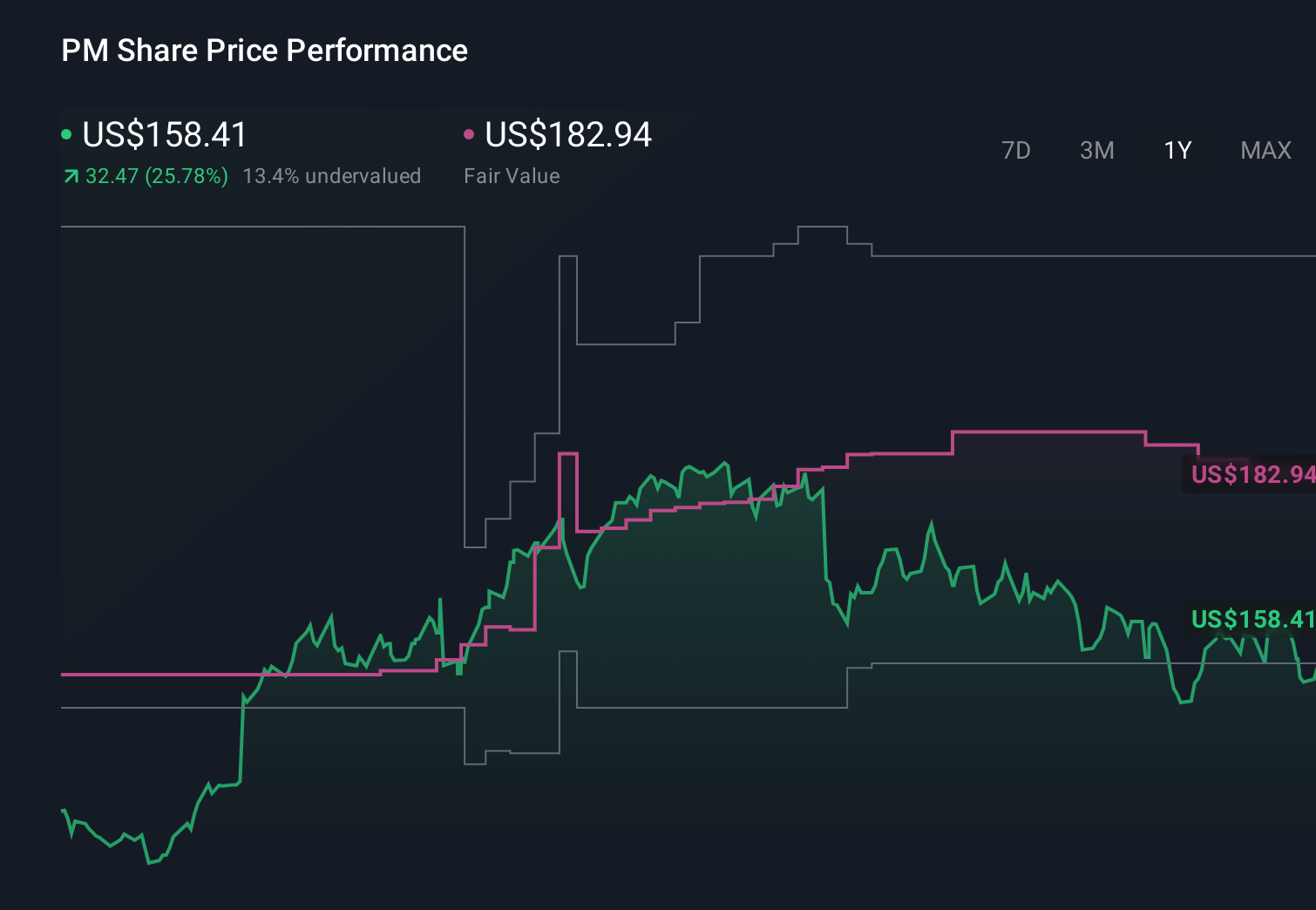

Philip Morris International's narrative projects $49.4 billion revenue and $14.5 billion earnings by 2028. This requires 8.2% yearly revenue growth and about a $6.3 billion earnings increase from $8.2 billion today.

Uncover how Philip Morris International's forecasts yield a $182.94 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts take a far more pessimistic view, even while assuming revenue could reach about US$47.1 billion and earnings US$14.4 billion by 2028, so it is worth asking whether this ESOP news and the risk of heavier regulation on both cigarettes and next generation products might eventually pull expectations closer to their side of the spectrum.

Explore 11 other fair value estimates on Philip Morris International - why the stock might be worth as much as 34% more than the current price!

Build Your Own Philip Morris International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Want Some Alternatives?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Rare earth metals are the new gold rush. Find out which 38 stocks are leading the charge.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com