Assessing TransMedics Group (TMDX) Valuation As Investors Reassess Growth Potential And Execution Risks

Why TransMedics Group is back in focus

TransMedics Group (TMDX) is back on many watchlists after recent stock swings tied to investor reassessment of its expanding organ care platform and integrated logistics, alongside ongoing debate over long term growth versus near term execution risks.

See our latest analysis for TransMedics Group.

The recent 1-day share price return of 2.93% and 7-day share price return of 3.58% come after a 30-day share price return decline of 7.49%. However, the 1-year total shareholder return of 60.52% and very large 5-year total shareholder return indicate that longer term momentum is still strong.

If TransMedics has you rethinking opportunities in medical technology, this could be a good moment to broaden your watchlist with other healthcare stocks.

With TransMedics trading at $126.28, sitting at a discount to both some analyst targets and certain intrinsic value estimates, you have to ask yourself: is there still mispricing here, or is any potential future growth already fully reflected?

Most Popular Narrative: 13% Undervalued

With TransMedics last closing at $126.28 versus a narrative fair value near $144.73, the current price sits below what this model implies.

International geographic expansion, especially the planned replication of the U.S. NOP model in Europe (representing 45% of global transplant volumes), could nearly double the company's total addressable market, increasing both top-line revenue potential and the ability to achieve greater operating leverage.

Curious what kind of transplant volume ramp, margin profile, and earnings multiple need to line up to support that fair value gap? The full narrative lays out a detailed revenue trajectory, changing profitability assumptions, and a future P/E that leans well above current sector averages. The exact mix of growth, margins, and discount rate might surprise you.

Result: Fair Value of $144.73 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh the risk that key heart and lung trials disappoint, or that tougher regulation and reimbursement slow international adoption of the OCS platform.

Find out about the key risks to this TransMedics Group narrative.

Another way to look at valuation

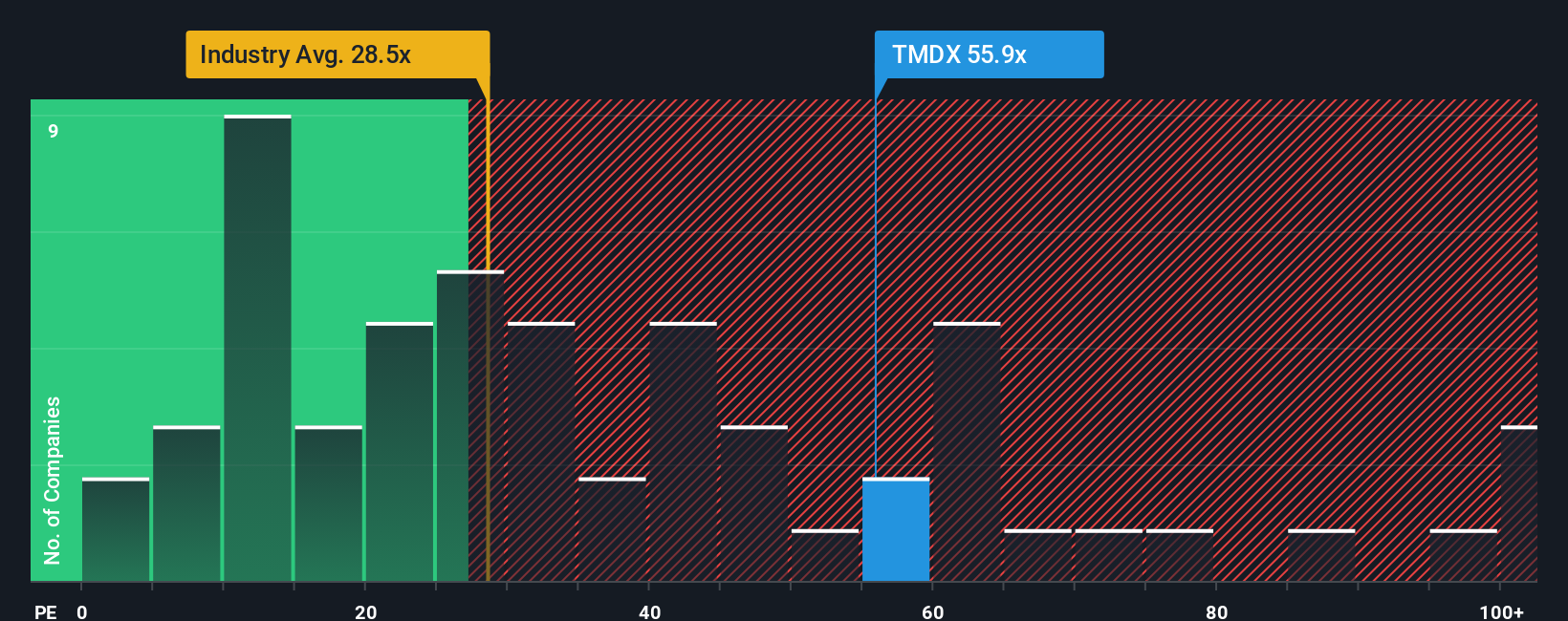

The narrative fair value near $144.73 paints TransMedics as undervalued, but its P/E of 47x is well above the US Medical Equipment industry at 29.9x, the peer average at 39.3x, and the fair ratio of 23.8x. That kind of gap can point to real valuation risk, so which story do you trust more?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own TransMedics Group Narrative

If you see the data differently or simply prefer to test your own assumptions, you can build a tailored TransMedics view in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding TransMedics Group.

Looking for more investment ideas?

If TransMedics has sharpened your thinking, do not stop here. Broaden your opportunity set with a few focused stock ideas that match your style.

- Target potential mispricing by scanning these 878 undervalued stocks based on cash flows that may be trading below what their cash flows imply.

- Capture growth themes by checking out these 25 AI penny stocks positioned around artificial intelligence adoption.

- Strengthen your watchlist with these 14 dividend stocks with yields > 3% that can add income alongside potential capital gains.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com