Bet Shemesh Engines Holdings (1997) Ltd (TLV:BSEN) Stocks Shoot Up 30% But Its P/E Still Looks Reasonable

Bet Shemesh Engines Holdings (1997) Ltd (TLV:BSEN) shareholders would be excited to see that the share price has had a great month, posting a 30% gain and recovering from prior weakness. The annual gain comes to 159% following the latest surge, making investors sit up and take notice.

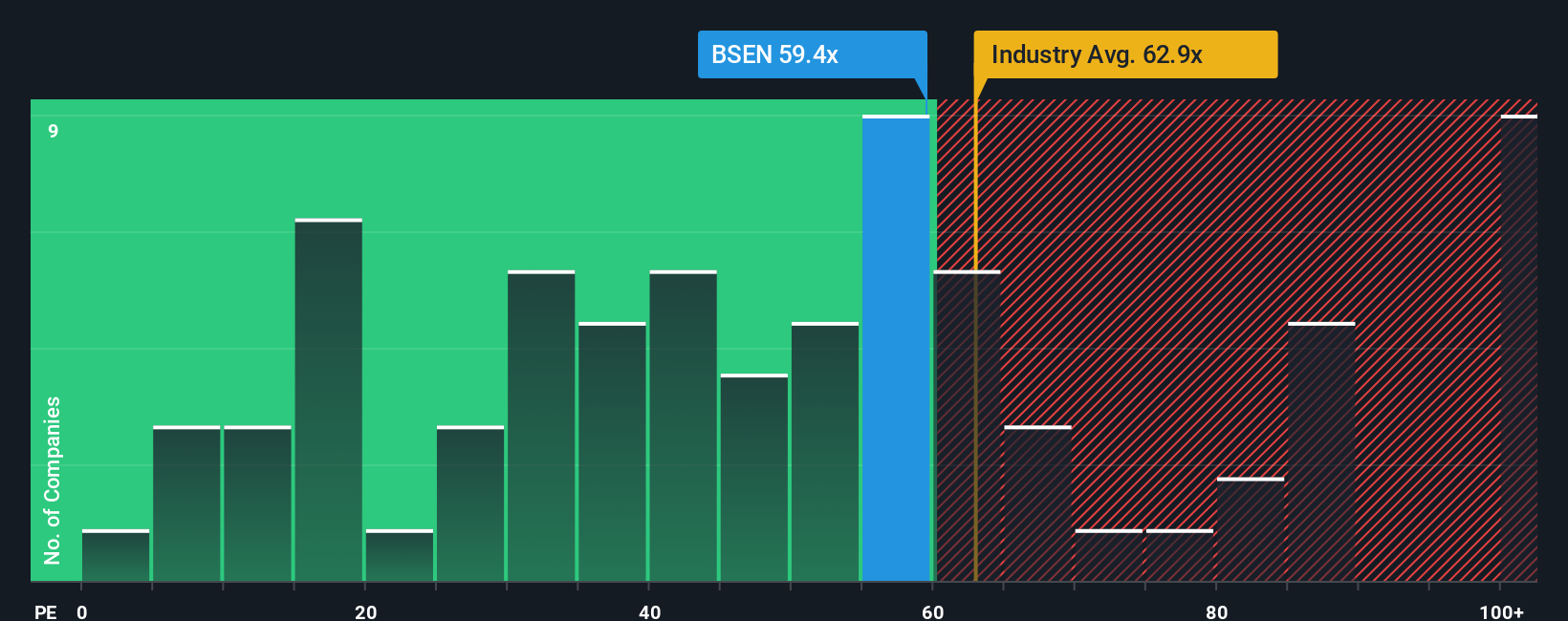

After such a large jump in price, Bet Shemesh Engines Holdings (1997)'s price-to-earnings (or "P/E") ratio of 59.4x might make it look like a strong sell right now compared to the market in Israel, where around half of the companies have P/E ratios below 16x and even P/E's below 11x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

The earnings growth achieved at Bet Shemesh Engines Holdings (1997) over the last year would be more than acceptable for most companies. One possibility is that the P/E is high because investors think this respectable earnings growth will be enough to outperform the broader market in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

View our latest analysis for Bet Shemesh Engines Holdings (1997)

Does Growth Match The High P/E?

Bet Shemesh Engines Holdings (1997)'s P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

Retrospectively, the last year delivered an exceptional 25% gain to the company's bottom line. The latest three year period has also seen an excellent 873% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Comparing that to the market, which is only predicted to deliver 23% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised earnings results.

With this information, we can see why Bet Shemesh Engines Holdings (1997) is trading at such a high P/E compared to the market. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

The strong share price surge has got Bet Shemesh Engines Holdings (1997)'s P/E rushing to great heights as well. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Bet Shemesh Engines Holdings (1997) maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Bet Shemesh Engines Holdings (1997) that you should be aware of.

If you're unsure about the strength of Bet Shemesh Engines Holdings (1997)'s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.