- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing FirstEnergy (FE) Valuation As Steady Share Performance Meets Conflicting Fair Value Signals

With no single headline event driving attention today, FirstEnergy (FE) is drawing interest as investors weigh its recent share performance, current valuation signals, and the utility’s earnings profile against its long term return history.

See our latest analysis for FirstEnergy.

FirstEnergy’s share price at $45.26 has been relatively steady in the short term, with a small 1-day and 7-day share price gain, while its 1-year and 5-year total shareholder returns suggest longer term momentum has been stronger than recent quarterly moves.

If FirstEnergy’s profile has you looking at other utilities and income names, it can also be worth scanning for pharma stocks with solid dividends as another way to source yield-focused ideas.

With shares near $45 and a modest discount to a $50 analyst target, along with solid long term total returns, the key question is whether FirstEnergy is still undervalued or if the market has already priced in future growth.

Most Popular Narrative Narrative: 9.5% Undervalued

With FirstEnergy last closing at $45.26 and the most followed narrative pointing to a fair value around $50, the valuation hinges heavily on how future earnings and cash flows are expected to develop over the next few years.

Large-scale infrastructure modernization and grid hardening initiatives, including the $28 billion investment plan through 2029 and a 15% CAGR in transmission rate base, enable higher returns on equity, improved reliability, and ultimately enhance net margins and earnings growth.

Curious what earnings and margin path needs to play out for that valuation to stack up. The narrative leans on measured revenue growth, fatter margins, and a future P/E that slightly steps down from today. Want to see exactly how those moving parts add up to the current fair value estimate.

Result: Fair Value of $50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, plenty could still upset that story, including higher interest costs on FirstEnergy’s heavy investment plans or faster adoption of rooftop solar and batteries eroding long term grid demand.

Find out about the key risks to this FirstEnergy narrative.

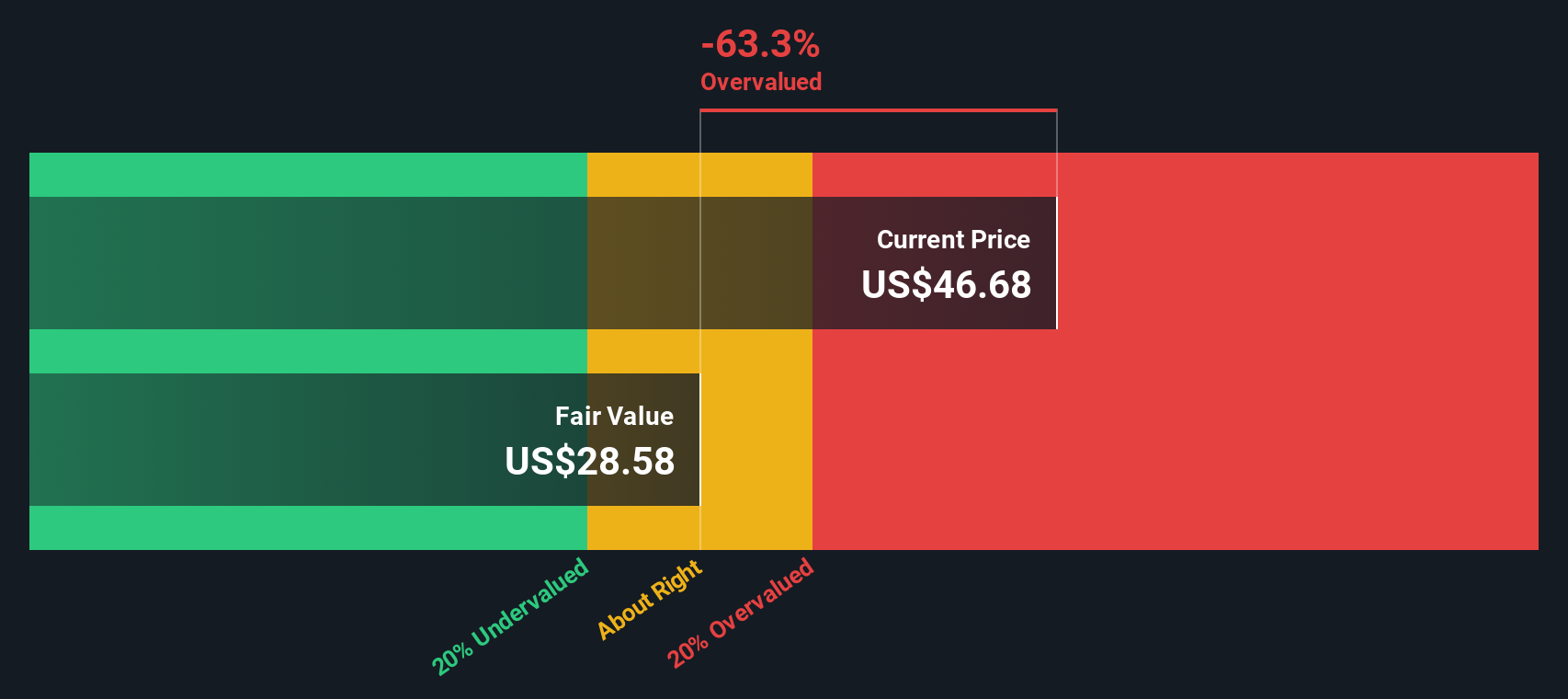

Another Angle: SWS DCF Says Overvalued

That 9.5% undervalued narrative sits awkwardly against the SWS DCF model, which puts FirstEnergy’s fair value at about $28.87 per share, well below the current $45.26 price. Instead of a discount, this view points to a premium. The key question is which set of assumptions you consider more reliable.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out FirstEnergy for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own FirstEnergy Narrative

If the story here does not quite line up with your own view, or you would rather test the assumptions yourself, you can build a custom narrative in just a few minutes with Do it your way.

A great starting point for your FirstEnergy research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If FirstEnergy has caught your eye, do not stop there. Use the screener to quickly surface other focused opportunities that might better fit your goals and risk comfort.

- Target potential value by checking out these 870 undervalued stocks based on cash flows that line up price with underlying cash flow strength.

- Explore technology by scanning these 25 AI penny stocks that are tied to artificial intelligence themes across different parts of the market.

- Increase your income focus by reviewing these 14 dividend stocks with yields > 3% that put distributions at the center of the thesis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com