- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Telix Pharmaceuticals (ASX:TLX) Valuation After Class Action Lawsuit And Regulatory Setbacks

Telix Pharmaceuticals (ASX:TLX) is under pressure after a securities class action lawsuit, which followed an SEC subpoena and an FDA Complete Response Letter on TLX250-CDx, raising fresh questions about disclosure and manufacturing controls.

See our latest analysis for Telix Pharmaceuticals.

The legal and regulatory setbacks have coincided with a sharp shift in sentiment, with a 30 day share price return of negative 24.04% and a 1 year total shareholder return decline of 54.49%, contrasting with a very large 5 year total shareholder return.

If Telix's recent volatility has you reassessing your options, this can be a good moment to scan other healthcare stocks that balance medical progress with different risk profiles.

With Telix now trading at A$11.25 after a 54.49% 1 year total return decline, yet carrying an implied discount to some valuation estimates, you have to ask: is sentiment overshooting the risks, or is the market already pricing in future growth?

Price-to-Sales of 3.8x: Is it justified?

On a P/S of 3.8x at A$11.25, Telix Pharmaceuticals screens as inexpensive compared to both its peers and the broader Australian Biotechs industry.

The P/S ratio compares the company’s market value with its revenue and is often used for biopharma names where earnings can be volatile through the development cycle. For Telix, this helps you benchmark what investors are currently willing to pay for each dollar of reported sales.

Telix is flagged as trading at good value relative to peers and the sector. Its 3.8x P/S sits well below both the Australian Biotechs industry average of 17.4x and a peer average of 31.5x. It is also below an estimated fair P/S ratio of 6.9x, a level the market could theoretically move toward if sentiment and fundamentals align with that model.

Explore the SWS fair ratio for Telix Pharmaceuticals

Result: Price-to-sales of 3.8x (UNDERVALUED)

However, you still have to weigh the SEC subpoena and FDA Complete Response Letter on TLX250-CDx, along with the ongoing class action, as potential overhangs on sentiment.

Find out about the key risks to this Telix Pharmaceuticals narrative.

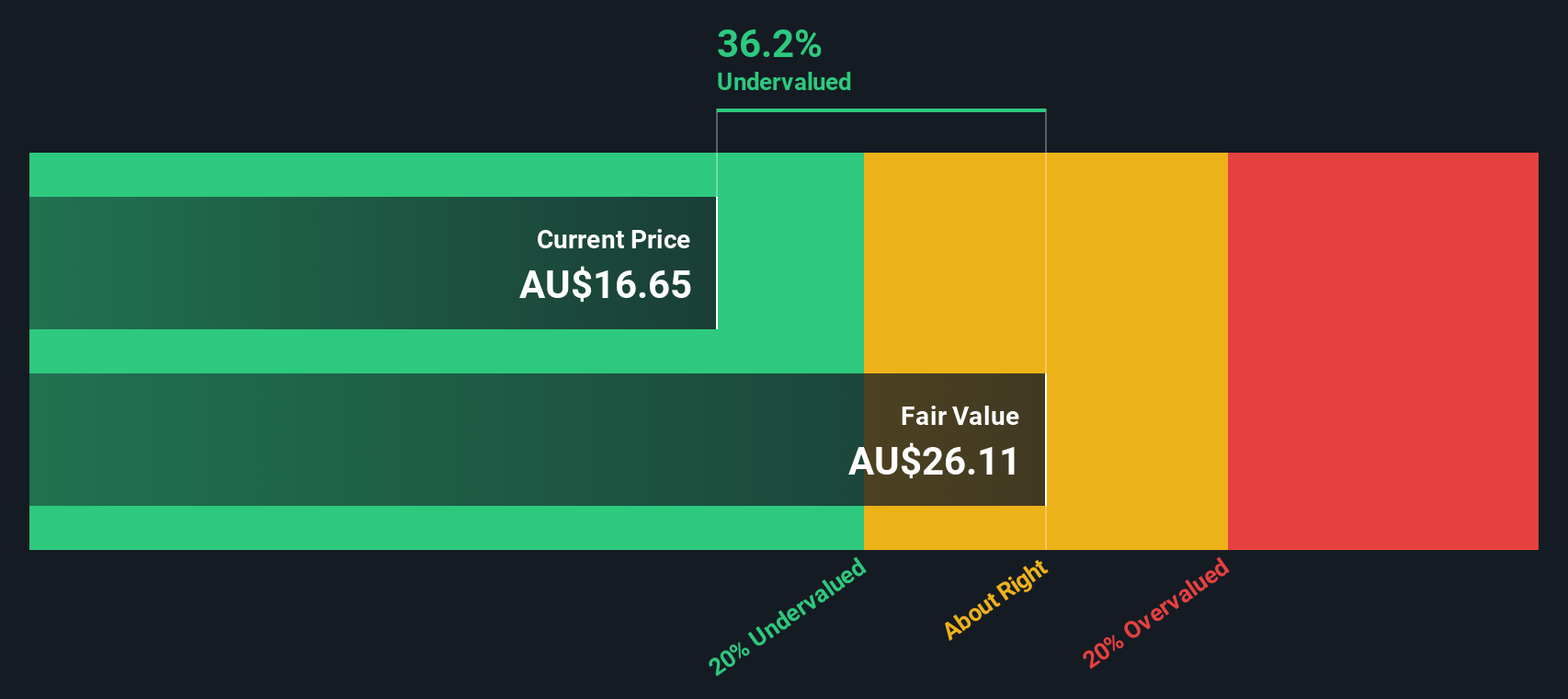

Another View: DCF points to deeper undervaluation

While the 3.8x P/S hints at a discount, our DCF model goes further, suggesting Telix’s fair value is A$29.53 versus the current A$11.25, a 61.9% discount. That is a wide gap, especially for a company facing regulatory and legal scrutiny. This raises an important question: is the model too optimistic, or is sentiment too harsh?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Telix Pharmaceuticals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 870 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Telix Pharmaceuticals Narrative

If you see the numbers differently or want to weigh the risks and rewards in your own way, you can build a full view in just a few minutes: Do it your way.

A great starting point for your Telix Pharmaceuticals research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Telix has you rethinking your exposure, do not stop here. Your next strong idea could already be on the radar in a curated screener set.

- Hunt for turnaround potential in beaten down names that still have solid fundamentals using these 870 undervalued stocks based on cash flows, tailored to cash flow based opportunities.

- Spot growth stories tied to artificial intelligence by scanning these 25 AI penny stocks, which link real business models with this fast evolving technology theme.

- Tap into income focused opportunities with these 14 dividend stocks with yields > 3%, targeting companies offering yields above 3% alongside fundamental checks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com