- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalA Look At Dollar General (DG) Valuation After Analyst Upgrades And Profit Outlook Raise

Dollar General (DG) has moved back into focus after JPMorgan upgraded the stock and Wells Fargo revised its outlook, following the retailer’s raised full-year profit guidance and better-than-expected third-quarter results.

See our latest analysis for Dollar General.

At a share price of $136.82, Dollar General has seen a 41.97% 90 day share price return and an 85.01% 1 year total shareholder return, although the 3 and 5 year total shareholder returns remain negative. As a result, recent momentum is building off a weaker longer term base.

If Dollar General’s rebound has you rethinking retail exposure, it could be a useful moment to broaden your search with fast growing stocks with high insider ownership.

With the shares up strongly in the past year, trading slightly above the average analyst price target but at a discount to one estimate of intrinsic value, you have to ask: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 11.5% Overvalued

With Dollar General last closing at $136.82 against a narrative fair value of $122.68, the gap raises questions about what future earnings justify that difference.

Analysts are assuming Dollar General's revenue will grow by 4.1% annually over the next 3 years.

Analysts assume that profit margins will increase from 2.9% today to 3.6% in 3 years time.

Curious what combination of modest revenue growth, higher margins and a premium earnings multiple add up to this valuation call? The full narrative lays out the exact earnings and cash flow path behind that $122.68 fair value, including how long it could take for profits to reach the level implied by those projections.

Result: Fair Value of $122.68 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, those projections could be challenged if store expansion leads to saturation in core markets, or if higher labor costs keep squeezing margins and offsetting efficiency gains.

Find out about the key risks to this Dollar General narrative.

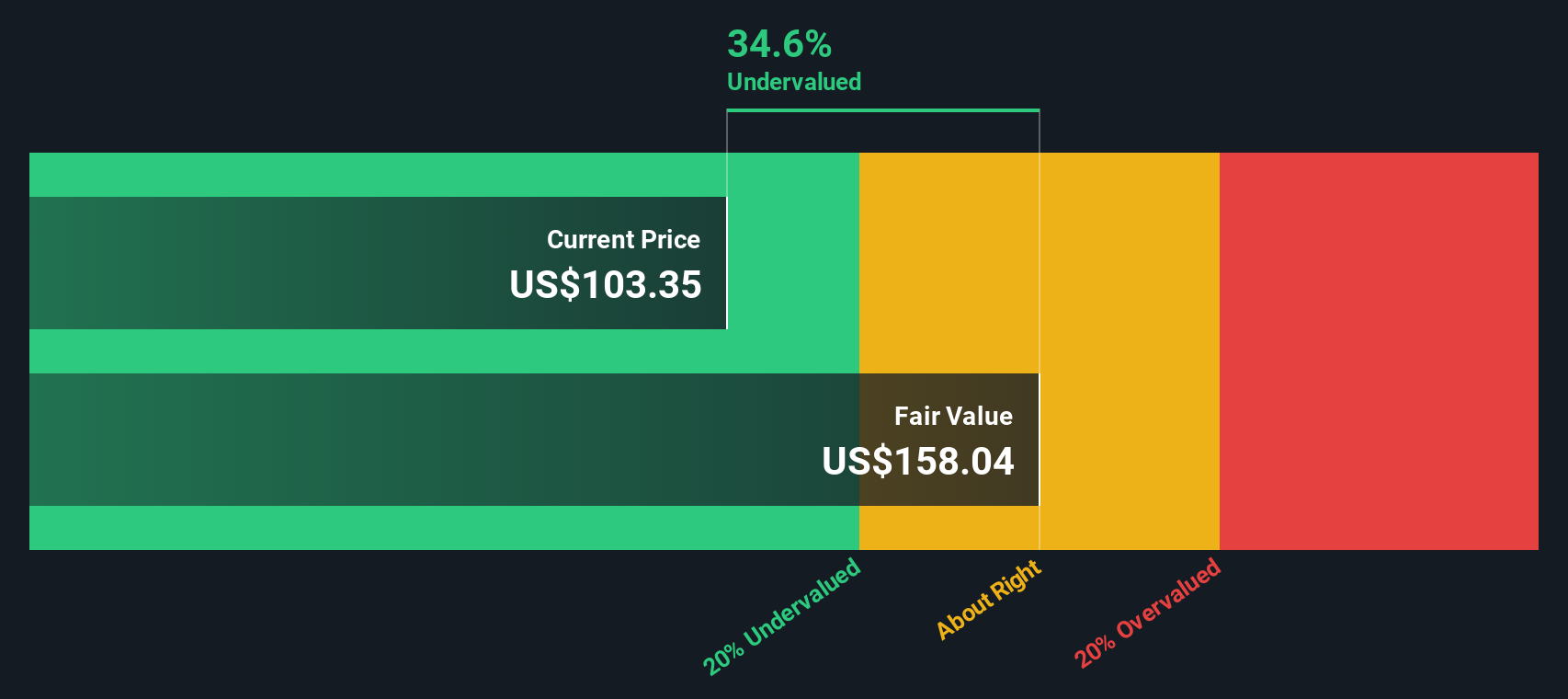

Another View: DCF Points the Other Way

While the AI narrative tags Dollar General as 11.5% overvalued at $122.68, our DCF model tells a different story. On that approach, the fair value sits at $174 per share, which is about 21.4% above the current $136.82 price. This suggests the market may be underestimating future cash flows.

Those are very different answers to the same question. The real issue for you is which set of assumptions on growth, margins and risk feels more realistic for the next few years.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dollar General for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Dollar General Narrative

If you look at these assumptions and feel they miss something, or you just prefer your own work, you can build a custom view in minutes, starting with Do it your way.

A great starting point for your Dollar General research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Dollar General has sharpened your thinking, do not stop there. Use the Simply Wall St screener to spot other opportunities that might fit your style.

- Target potential mispricings by scanning these 868 undervalued stocks based on cash flows that may offer stronger cash flow support for their current share prices.

- Ride powerful technology trends by checking out these 25 AI penny stocks shaping how data, automation and productivity tools are built and used.

- Tap into income-focused opportunities by reviewing these 14 dividend stocks with yields > 3% that offer yields above 3% alongside listed business fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com