- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs EQT (EQT) Pricing Reflect Its DCF And P/E Valuation Signals?

- If you are wondering whether EQT is offering fair value right now, its current share price of US$53.46 raises some important questions about what is already priced in.

- The stock has seen mixed returns, with a 2% decline over the last 7 days and an 11.9% decline over the last 30 days, while the 1 year return stands at 13.6% and the 3 year return at 61.5%.

- Recent attention on the company has been shaped by ongoing sector wide interest in energy producers and how investors are weighing long term demand for natural gas against changing capital allocation priorities. In this context, EQT remains on the radar for investors who are watching how market sentiment lines up with fundamentals.

- EQT currently holds a valuation score of 4 out of 6. Next, we will look at what traditional methods like DCFs and multiples indicate about that number, before turning to a more rounded way of thinking about value at the end of the article.

Approach 1: EQT Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model looks at the cash EQT is expected to generate in the future and discounts those projected cash flows back into today’s dollars to estimate what the whole business might be worth now.

For EQT, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections. The latest twelve month free cash flow is about US$2.13b. Analysts provide forecasts for several years, and Simply Wall St extends these, giving a projected free cash flow of US$3.07b in 2030, with a series of annual figures between. All of these future cash flows, such as the discounted US$3.61b in 2026 and US$2.20b in 2030, are brought back to a present value estimate per share.

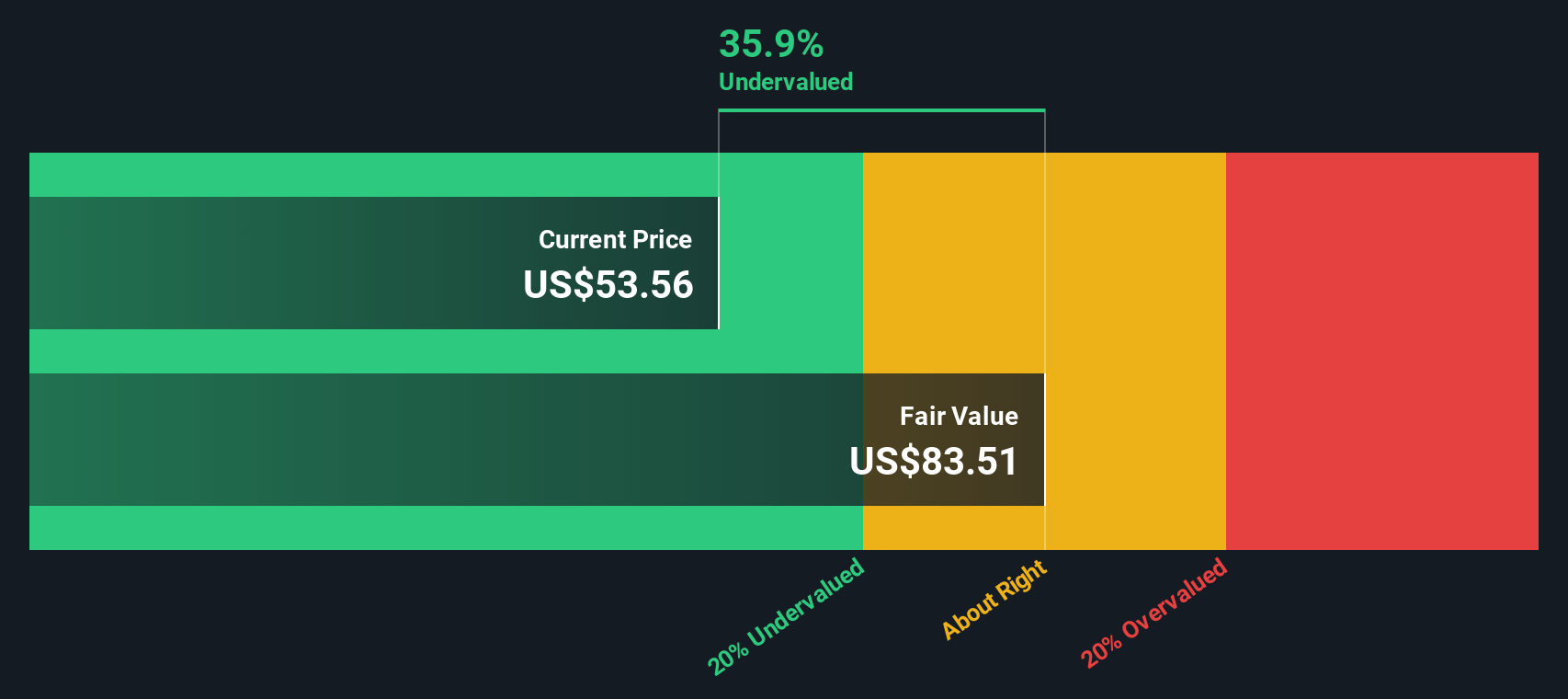

On this basis, the DCF model suggests an intrinsic value of about US$97.26 per share, compared with the current share price of US$53.46. That implies the stock is trading at roughly a 45.0% discount to this estimate. On this model alone, this points to a materially undervalued reading.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests EQT is undervalued by 45.0%. Track this in your watchlist or portfolio, or discover 868 more undervalued stocks based on cash flows.

Approach 2: EQT Price vs Earnings (P/E)

For a profitable company like EQT, the P/E ratio is a useful sense check because it links what you pay today directly to the earnings the business is already producing. It also reflects what the market is willing to pay for each dollar of current earnings.

What counts as a "normal" P/E depends a lot on growth expectations and risk. Higher expected earnings growth or lower perceived risk can justify a higher multiple, while slower growth or higher risk usually supports a lower one. EQT currently trades on a P/E of 18.7x, compared with the Oil and Gas industry average of 13.2x and a peer average of 15.4x, so the stock is pricing in a higher multiple than these simple benchmarks.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what P/E might make sense for EQT given its earnings growth profile, industry, profit margins, market cap and specific risks. For EQT, this Fair Ratio is 21.3x, which is higher than both the industry and peer averages. Because EQT’s actual P/E of 18.7x sits below this 21.3x Fair Ratio by a more than modest margin, the shares screen as undervalued on this metric.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1464 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your EQT Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St’s Community page you can use Narratives, where you write a clear story about EQT that links your view on catalysts like LNG contracts, data center demand or regulatory risks to a forecast for revenue, earnings, margins and a fair value. You can then compare that fair value with the current price to help decide when to buy or sell, while the platform keeps your view updated as new news or earnings arrive. One investor might lean toward the higher US$80 analyst target and build a Narrative around long term AI and LNG demand, while another might anchor closer to the US$42 lower target with a more cautious Narrative around decarbonization, regulation and concentration in Appalachia.

Do you think there's more to the story for EQT? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com