- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Whether Ichigo (TSE:2337) Looks Overvalued After Recent Share Price Momentum

Ichigo (TSE:2337) is in focus today as investors weigh its latest share performance and financial profile, including a ¥438 last close price, along with current revenue and net income figures from its diversified real estate and clean energy operations.

See our latest analysis for Ichigo.

Ichigo’s recent share price has been relatively steady day to day, but a 10.05% 1 month share price return alongside a 20.26% 1 year total shareholder return suggests momentum has been building over both shorter and longer horizons.

If Ichigo’s profile has you thinking about where else value and momentum might be lining up, this could be a good moment to check out fast growing stocks with high insider ownership.

With Ichigo trading at ¥438 versus an analyst price target of ¥420 and an intrinsic value estimate pointing to a premium, the central question is whether investors are overpaying today or correctly pricing in future growth potential.

Most Popular Narrative Narrative: 4.3% Overvalued

With Ichigo’s narrative fair value sitting at ¥420 versus a ¥438 last close, the story centers on how future earnings and margins might evolve.

The analysts have a consensus price target of ¥470.0 for Ichigo based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ¥570.0, and the most bearish reporting a price target of just ¥410.0.

Want to see what sits behind that valuation spread? The narrative focuses on measured revenue growth, steady margins, and a future earnings multiple that assumes persistent profitability.

Result: Fair Value of ¥420 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still clear pressure points, including interest rate driven borrowing costs and ongoing clean energy underperformance, that could challenge this positive valuation narrative.

Find out about the key risks to this Ichigo narrative.

Another View Using Earnings Ratios

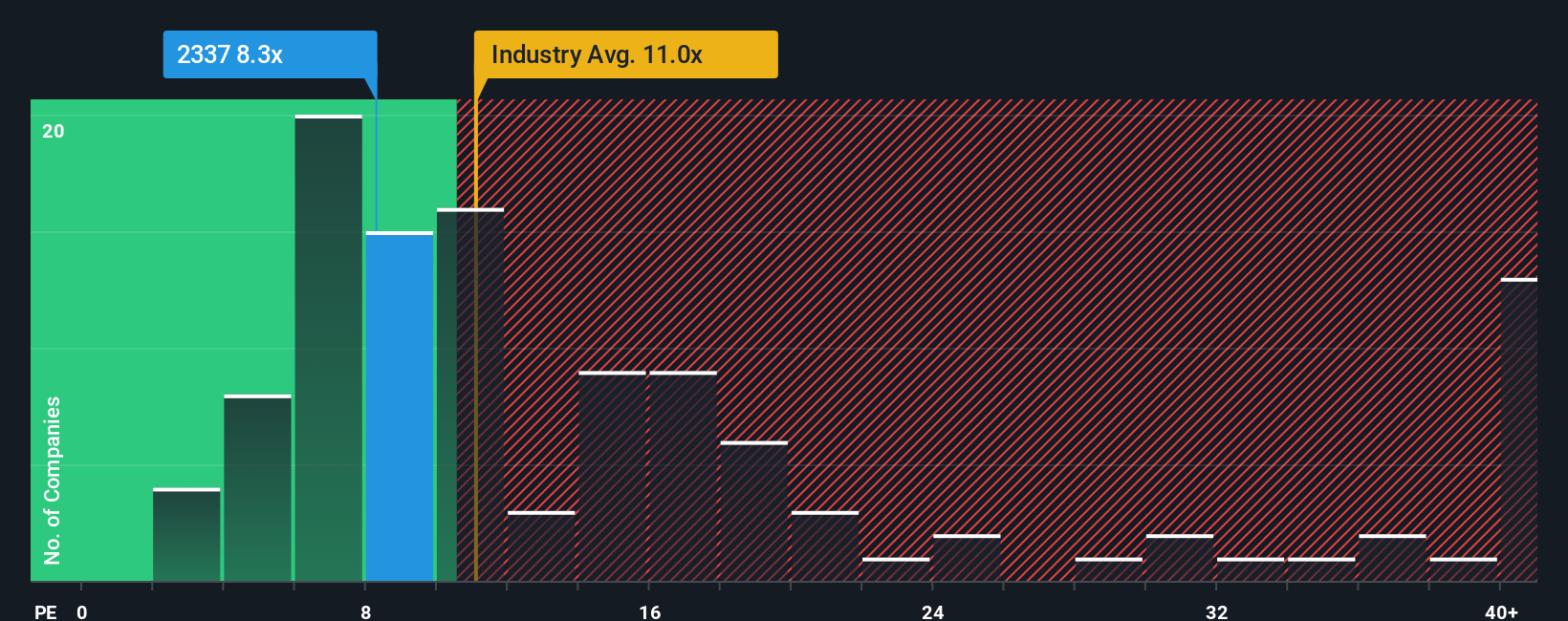

The narrative model flags Ichigo as 4.3% overvalued at ¥438 versus a ¥420 fair value, but its earnings ratio tells a different story. The current P/E of 9.8x sits below both the JP Real Estate industry average of 11.8x and an estimated fair ratio of 12.5x. This suggests a more forgiving price. If the market shifts closer to that fair ratio, today’s level could look less demanding. Which story do you think holds more weight?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Ichigo Narrative

If you look at the numbers and come to a different conclusion, or prefer to test your own view, you can build a custom story in a few minutes by starting with Do it your way.

A great starting point for your Ichigo research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about building a stronger portfolio, do not stop at one stock. Use the screener to spot opportunities you might otherwise miss.

- Spot potential bargains early by scanning these 867 undervalued stocks based on cash flows that could be trading below what their cash flows might justify.

- Tap into future tech themes by zeroing in on these 25 AI penny stocks shaping how artificial intelligence reaches real-world businesses.

- Boost your income focus by reviewing these 14 dividend stocks with yields > 3% that offer higher yields while you assess their fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com