- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalEvaluating Eaton (ETN)’s Valuation After a Recent Pullback in Its Share Price

Eaton (ETN) has quietly pulled back about 3% over the past month and roughly 14% in the past 3 months, giving investors a chance to revisit the long term power management story at a lower entry point.

See our latest analysis for Eaton.

Zooming out, the recent pullback follows a strong multi year run, with Eaton still sitting near record territory after a robust three year total shareholder return of about 112%, even as near term share price momentum cools.

If Eaton’s reset has you thinking about what else could surprise to the upside, this is a good moment to explore fast growing stocks with high insider ownership.

With shares still trading below consensus targets but well above historical levels after a blockbuster multiyear run, the key question now is whether Eaton remains undervalued or if the market has already priced in its next leg of growth.

Most Popular Narrative Narrative: 19% Undervalued

With the narrative fair value sitting around $404 against Eaton’s last close near $327, the story leans toward upside if its roadmap delivers.

Strategic wins and technology leadership in the rapidly expanding data center end market are deepening Eaton's penetration and raising content per megawatt, with major partnerships (e.g., NVIDIA, Siemens Energy) and acquisitions (Fibrebond, Resilient Power) positioning Eaton as the go-to provider for next-generation high-density and AI-centric infrastructure; this supports outsized revenue growth and structurally higher margins due to a richer, more sophisticated product mix.

Want to see how ambitious revenue targets, fatter margins, and a premium future earnings multiple all fit together into that valuation? The full narrative connects the dots.

Result: Fair Value of $404.06 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, stretched data center expectations and ongoing integration risks from recent acquisitions could quickly challenge today’s upbeat earnings and valuation narrative.

Find out about the key risks to this Eaton narrative.

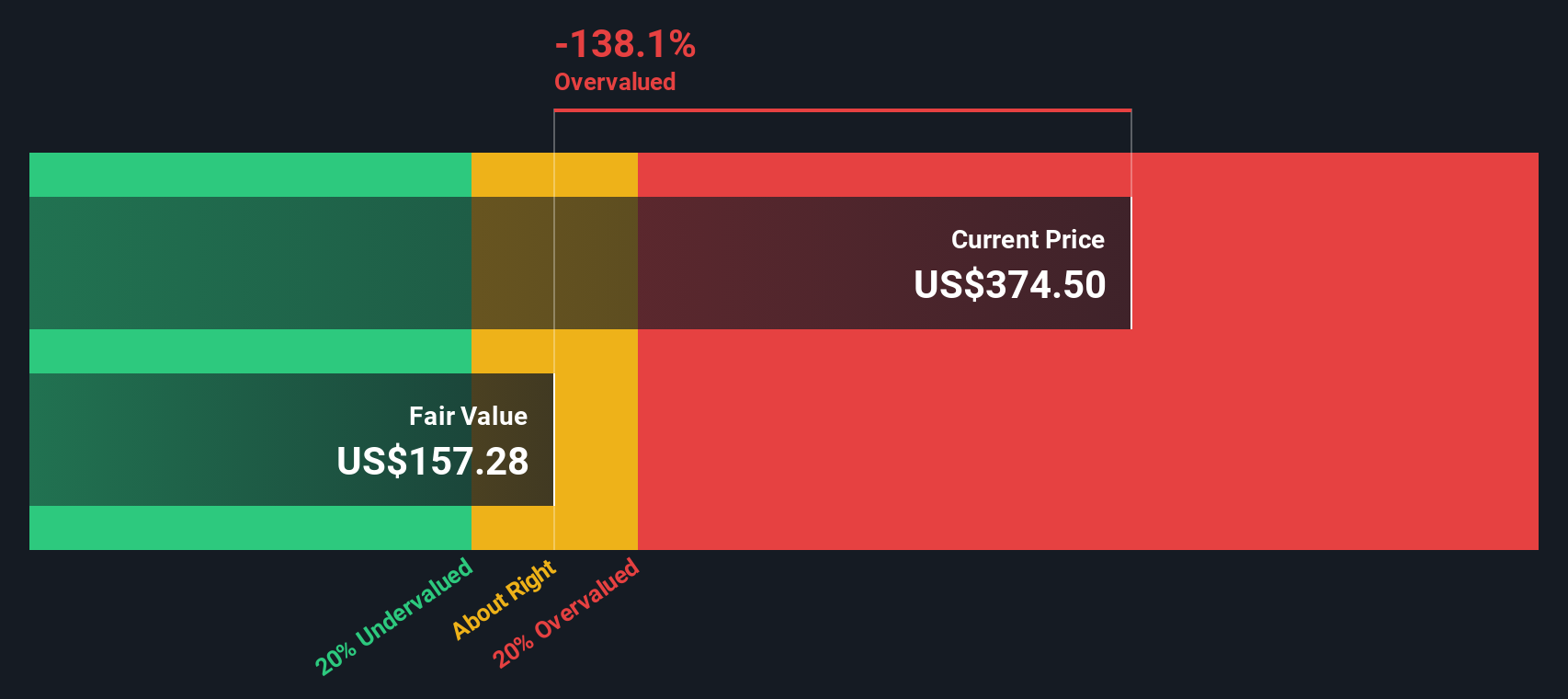

Another Way To Look At Valuation

Our SWS DCF model lands far below the narrative fair value, at about $242 per share versus the current $327 price, flagging Eaton as overvalued on cash flows even as analysts see upside. If growth or margins disappoint, this tougher lens could prove closer to reality.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Eaton for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 875 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Eaton Narrative

If you see the story differently or want to stress test the assumptions with your own research, you can build a complete view in minutes: Do it your way.

A great starting point for your Eaton research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next smart idea?

Do not stop at Eaton. Use the Simply Wall St Screener now to uncover fresh, high conviction opportunities that other investors will only notice later.

- Capture potential income and stability by targeting reliable payers through these 14 dividend stocks with yields > 3% with yields that could support your long term returns.

- Position yourself early in transformative innovation by scanning these 25 AI penny stocks shaping everything from automation to real time data intelligence.

- Strengthen your margin of safety by zeroing in on these 875 undervalued stocks based on cash flows where prices may not yet reflect underlying cash flow power.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com