- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Inflation-Protected Contracting Reshaping The Cash Flow Story For Enterprise Products Partners (EPD)?

- Enterprise Products Partners L.P. recently highlighted that it secures stable, fee-based income through long-term, inflation-protected contracts and expects additional predictable cash flow from growth projects such as Athena and Mentone West 2, which are planned to be operating by the end of 2026.

- This combination of inflation-linked contracts and a visible project pipeline has reinforced the partnership’s appeal for income-focused investors seeking resilient cash flows.

- We’ll now examine how this emphasis on long-term, inflation-protected contracts could influence Enterprise Products Partners’ broader investment narrative.

AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Enterprise Products Partners Investment Narrative Recap

To own Enterprise Products Partners, you need to believe its fee-based, inflation-linked contracts and expansion projects can keep cash flows resilient despite commodity and macro volatility. The latest update on Athena and Mentone West 2 strengthens the near term growth catalyst of added processing capacity, but it does not materially change the key risk around the partnership’s sizeable debt load and its sensitivity to interest rate and credit market conditions.

In that context, the recent series of quarterly distribution increases to US$0.545 per unit in 2025 stands out, because it directly ties into the income story that those long term, inflation-protected contracts aim to support. For investors watching both the build out of new assets and the balance sheet, the interaction between rising cash payouts and a high level of debt will likely remain central to assessing how durable Enterprise’s income profile really is.

However, investors should also be aware that a high and growing cash distribution alongside substantial debt could...

Read the full narrative on Enterprise Products Partners (it's free!)

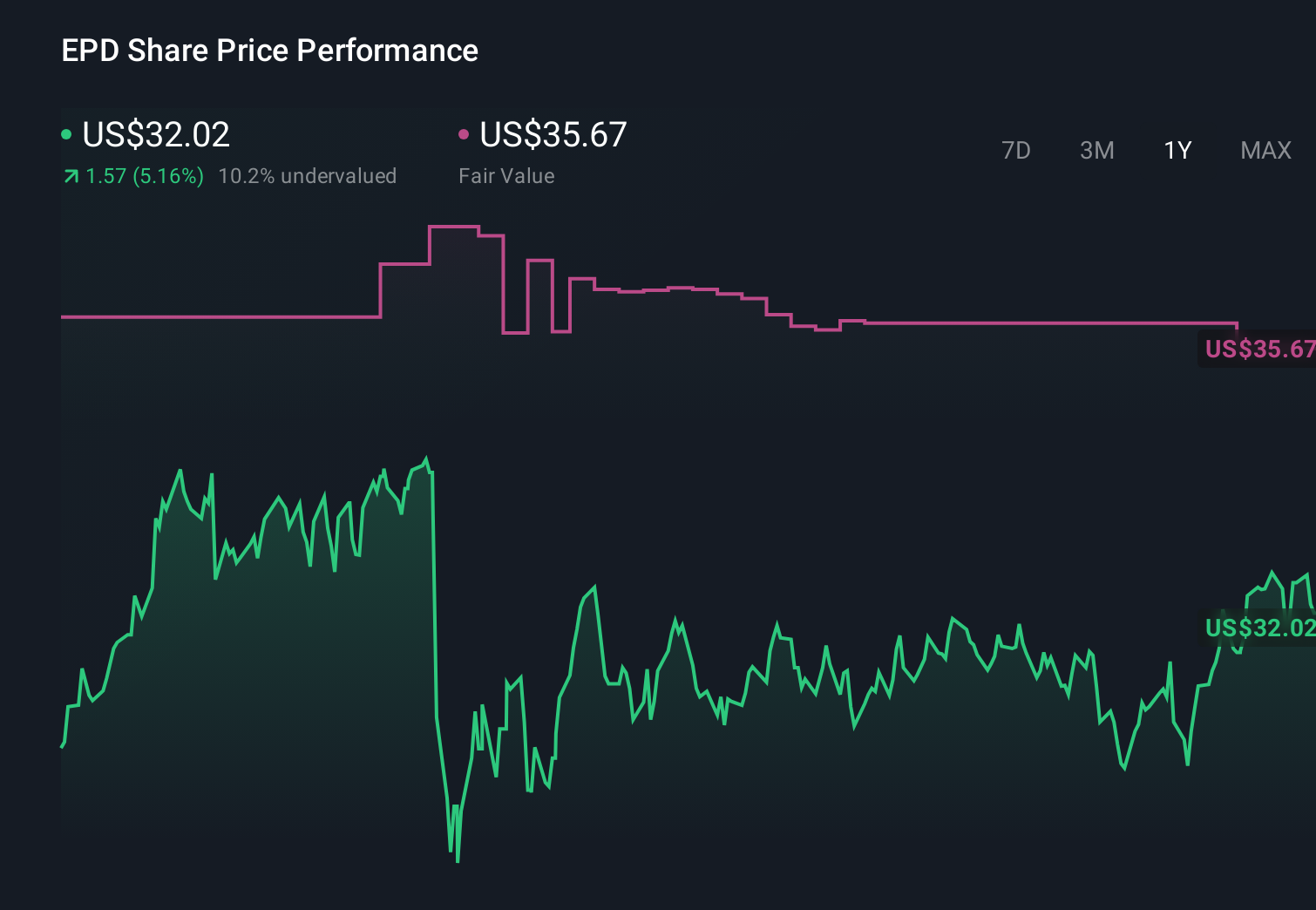

Enterprise Products Partners' narrative projects $53.5 billion revenue and $6.6 billion earnings by 2028. This requires a 0.8% yearly revenue decline and an earnings increase of about $0.8 billion from $5.8 billion today.

Uncover how Enterprise Products Partners' forecasts yield a $35.67 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Ten members of the Simply Wall St Community now place Enterprise’s fair value anywhere between about US$29 and US$75, highlighting how far apart individual views can sit. When you set those against the reliance on long term, inflation linked contracts as a key earnings driver, it becomes even more important to compare several perspectives before forming your own view.

Explore 10 other fair value estimates on Enterprise Products Partners - why the stock might be worth over 2x more than the current price!

Build Your Own Enterprise Products Partners Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Enterprise Products Partners research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enterprise Products Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enterprise Products Partners' overall financial health at a glance.

No Opportunity In Enterprise Products Partners?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com