- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalCanso Select Opportunities Corporation's (CVE:CSOC.A) Shares Bounce 110% But Its Business Still Trails The Market

Canso Select Opportunities Corporation (CVE:CSOC.A) shareholders have had their patience rewarded with a 110% share price jump in the last month. The last month tops off a massive increase of 246% in the last year.

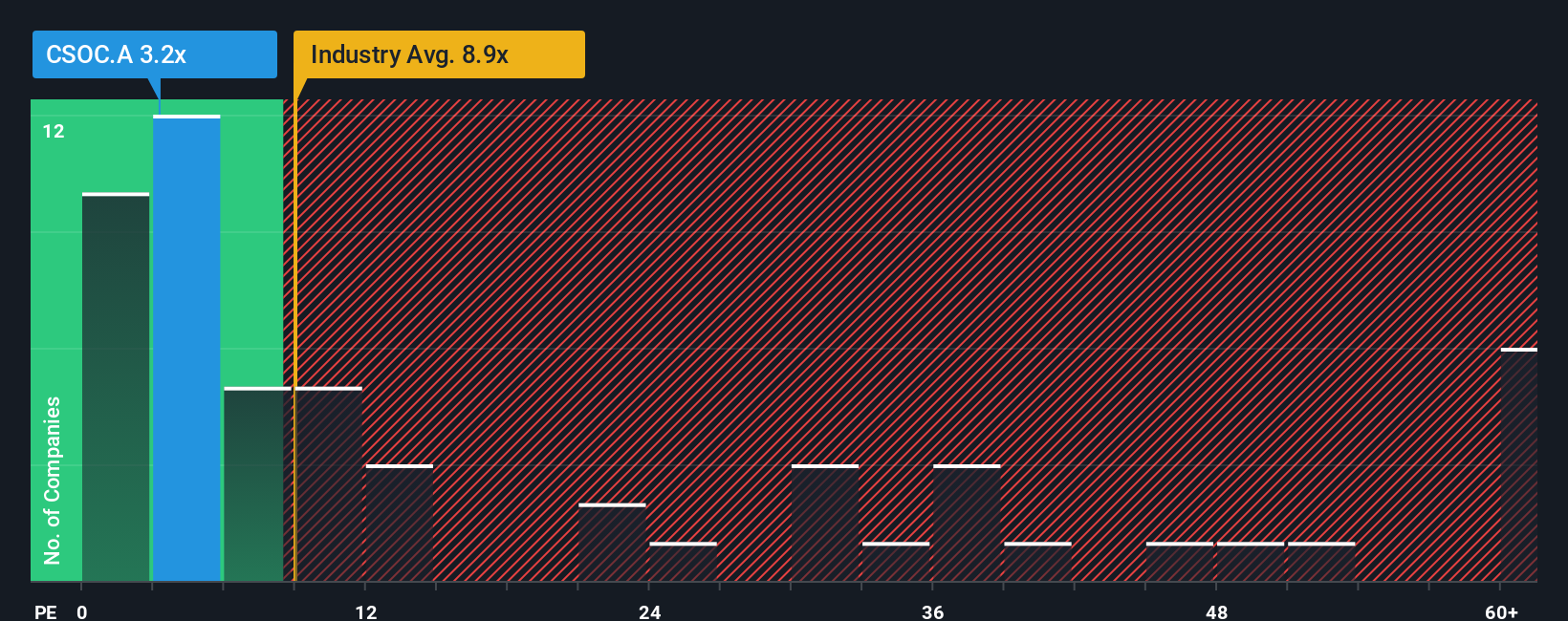

Even after such a large jump in price, given about half the companies in Canada have price-to-earnings ratios (or "P/E's") above 17x, you may still consider Canso Select Opportunities as a highly attractive investment with its 3.2x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With earnings growth that's exceedingly strong of late, Canso Select Opportunities has been doing very well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Canso Select Opportunities

Is There Any Growth For Canso Select Opportunities?

The only time you'd be truly comfortable seeing a P/E as depressed as Canso Select Opportunities' is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered an exceptional 99% gain to the company's bottom line. However, the latest three year period hasn't been as great in aggregate as it didn't manage to provide any growth at all. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 24% shows it's noticeably less attractive on an annualised basis.

With this information, we can see why Canso Select Opportunities is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Final Word

Even after such a strong price move, Canso Select Opportunities' P/E still trails the rest of the market significantly. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Canso Select Opportunities revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Canso Select Opportunities (1 is a bit unpleasant!) that you need to be mindful of.

Of course, you might also be able to find a better stock than Canso Select Opportunities. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.