- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMarket Cool On loanDepot, Inc.'s (NYSE:LDI) Revenues Pushing Shares 25% Lower

To the annoyance of some shareholders, loanDepot, Inc. (NYSE:LDI) shares are down a considerable 25% in the last month, which continues a horrid run for the company. Indeed, the recent drop has reduced its annual gain to a relatively sedate 9.8% over the last twelve months.

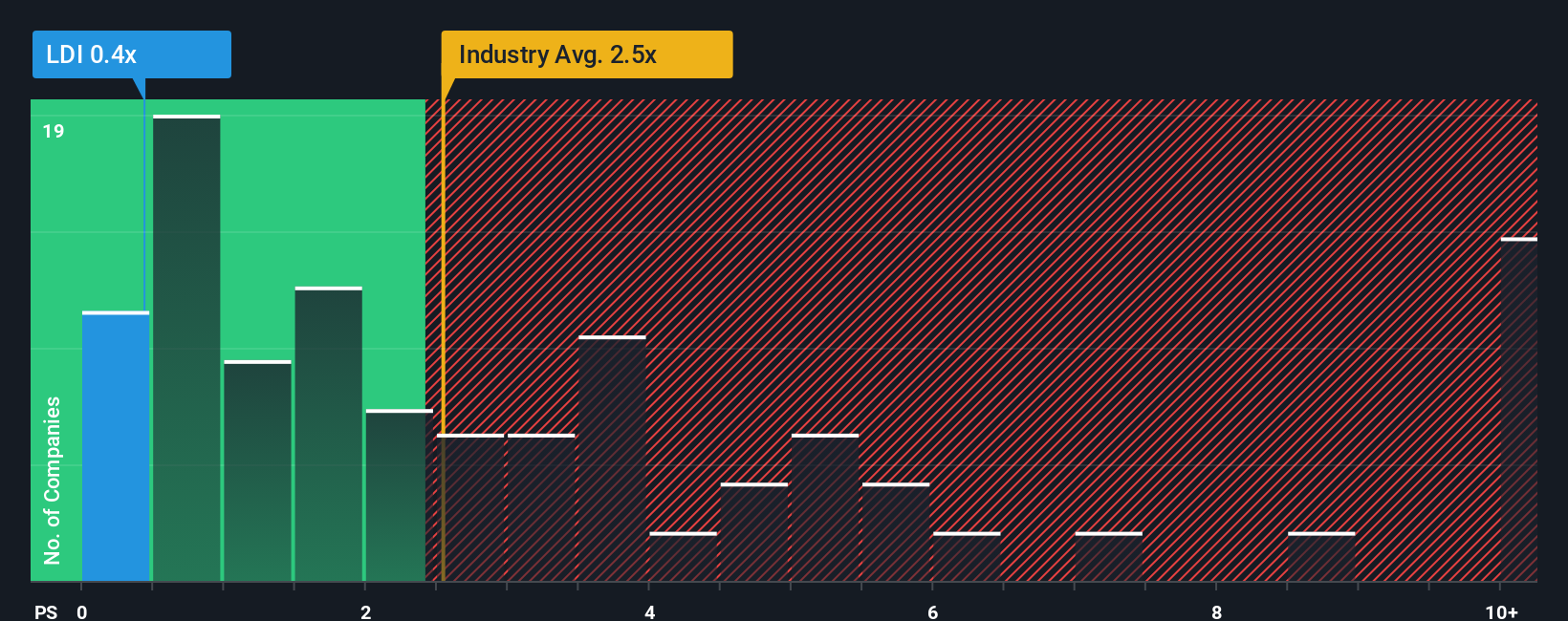

Since its price has dipped substantially, loanDepot may be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.4x, since almost half of all companies in the Diversified Financial industry in the United States have P/S ratios greater than 2.5x and even P/S higher than 5x are not unusual. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for loanDepot

What Does loanDepot's Recent Performance Look Like?

Recent revenue growth for loanDepot has been in line with the industry. It might be that many expect the mediocre revenue performance to degrade, which has repressed the P/S ratio. If you like the company, you'd be hoping this isn't the case so that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on loanDepot.Is There Any Revenue Growth Forecasted For loanDepot?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like loanDepot's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 11% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 33% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next year should generate growth of 29% as estimated by the five analysts watching the company. With the industry only predicted to deliver 7.1%, the company is positioned for a stronger revenue result.

With this information, we find it odd that loanDepot is trading at a P/S lower than the industry. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

What We Can Learn From loanDepot's P/S?

loanDepot's P/S looks about as weak as its stock price lately. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

To us, it seems loanDepot currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. The reason for this depressed P/S could potentially be found in the risks the market is pricing in. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

Having said that, be aware loanDepot is showing 2 warning signs in our investment analysis, you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.