- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHas Citi’s 74% Surge in 2025 Already Priced In Its Transformation Story?

- If you are wondering whether Citigroup is still a value play after its big run, or if you have already missed the boat, this breakdown will help you decide whether the current price makes sense or is getting ahead of itself.

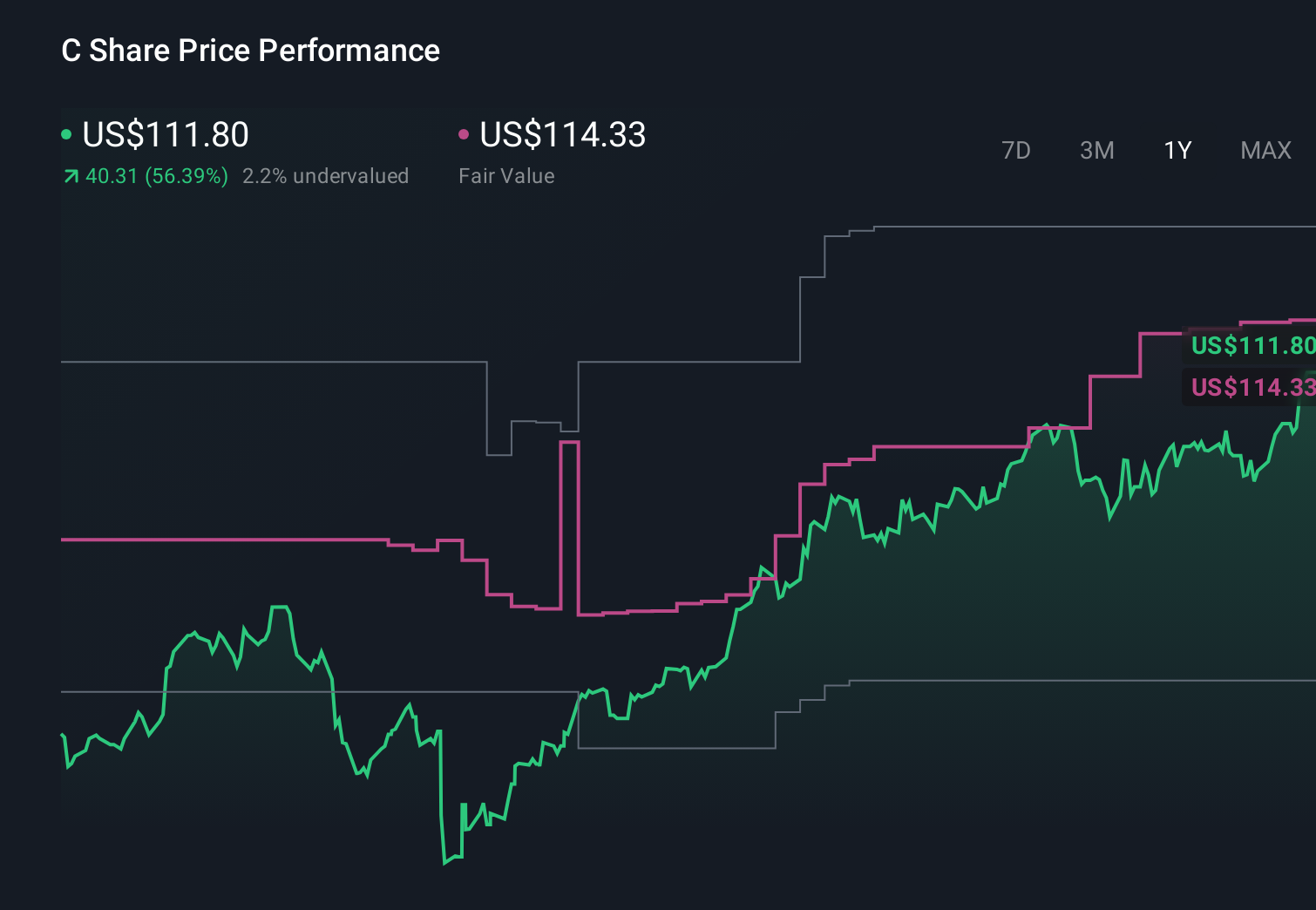

- The stock has surged recently, climbing 9.1% over the last week, 21.9% in the past month, and 73.8% year to date, with a 76.0% gain over the last year and 203.8% over three years.

- A large part of this momentum reflects investors becoming more positive on large global banks as credit fears ease and capital return stories become more compelling. Citigroup has been in the headlines for its ongoing restructuring efforts, regulatory de-risking moves, and progress on simplifying its global footprint, all of which are feeding into shifting market expectations.

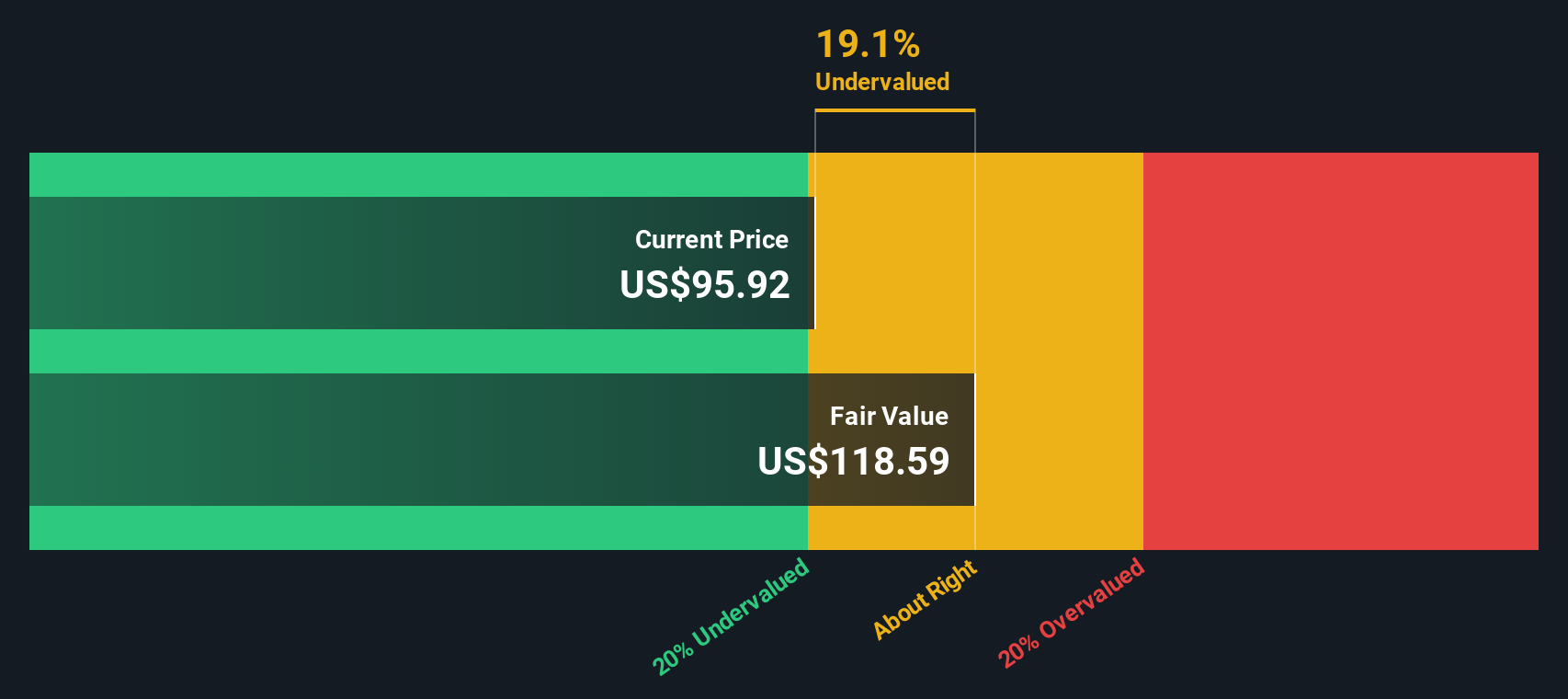

- Even after that rally, Citigroup only scores a 2/6 valuation check score on our framework, suggesting it appears undervalued on some metrics but not others. Next, we will examine discounted cash flow analysis, valuation multiples, and asset-based views, before finishing with a more holistic way to think about the stock's overall value.

Citigroup scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Citigroup Excess Returns Analysis

The Excess Returns model estimates what Citigroup can earn on shareholders' equity above its required cost of capital, and then capitalizes those surplus profits into a fair value per share.

For Citigroup, the starting point is a Book Value of $108.41 per share and a Stable EPS of $10.34 per share, based on weighted future return on equity estimates from 13 analysts. The market is not just paying for that profit stream; it is also judging whether those earnings exceed the bank's Cost of Equity of $9.79 per share. The difference, an Excess Return of $0.55 per share, signals that Citigroup is expected to generate value over and above what investors demand.

The model also assumes a Stable Book Value of $119.29 per share, informed by estimates from 11 analysts, and an Average Return on Equity of 8.67%. Combining these inputs, the Excess Returns framework arrives at an intrinsic value of about $130.41 per share, which implies the stock is roughly 6.8% below its estimated fair value.

This suggests the current price is slightly on the cheap side, but not a screaming bargain.

Result: ABOUT RIGHT

Citigroup is fairly valued according to our Excess Returns, but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: Citigroup Price vs Earnings

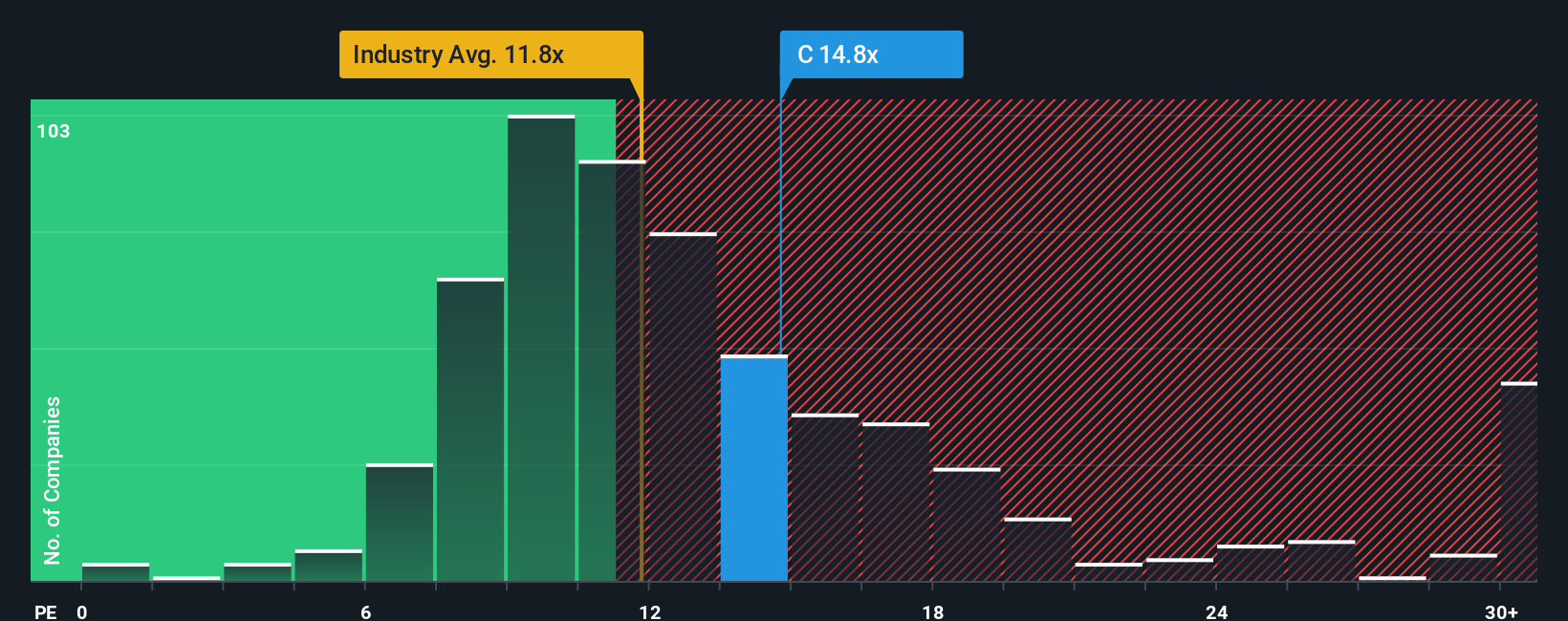

For a profitable bank like Citigroup, the price to earnings, or PE, ratio is a practical way to gauge how much investors are willing to pay for each dollar of earnings. It captures not just current profitability, but what the market expects those earnings to do over time.

In general, faster growth and lower perceived risk warrant a higher PE ratio, while slower growth or elevated risk justify a lower one. Citigroup currently trades on a PE of 16.19x, above the broader Banks industry average of about 11.94x and ahead of its peer group average of 13.91x. This suggests investors are already pricing in some improvement relative to typical large banks.

Simply Wall St’s Fair Ratio, at 17.06x, estimates the PE you might expect for Citigroup given its specific mix of earnings growth, profitability, risk profile, industry, and market cap. This is more tailored than a simple comparison to peers or sector averages, which can overlook differences in balance sheet strength, business mix, and risk. With the Fair Ratio only slightly above the current 16.19x, the stock looks close to fairly valued on an earnings multiple basis.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1459 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Citigroup Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach a clear story to your numbers for Citigroup.

A Narrative is your view of the company, written as a story that connects what you think will happen to Citi’s business with concrete assumptions about its future revenue, earnings, margins, and ultimately its fair value.

On Simply Wall St, inside the Community page used by millions of investors, Narratives make this process accessible by guiding you to link Citi’s story to a forecast and to a fair value estimate that you can then compare directly with today’s share price to decide whether to buy, hold, or sell.

Because Narratives are updated dynamically when new information like quarterly earnings, regulatory changes, or major news hits, your fair value view stays aligned with the latest data rather than going stale.

For example, one Citigroup Narrative on the platform currently sees fair value at about $233 per share while another pegs it closer to $116, showing how different investors can reasonably reach very different conclusions from the same underlying company by telling, and quantifying, different stories about its future.

For Citigroup however we will make it really easy for you with previews of two leading Citigroup Narratives:

Fair value: $233.04

Implied undervaluation: 47.8%

Forecast revenue growth: 6.0%

- Sees Citi as a long term potential beneficiary of the GENIUS Act and stablecoin regulation, with Citi Token Services positioned as a key infrastructure component for institutional digital payments.

- Argues that core franchises in Services, Markets, Investment Banking, Wealth, and U.S. Personal Banking are all growing, with rising RoTCE and disciplined capital returns.

- States that Citi could more than double net income over the next decade, which in this view would support a fair value around $230 plus an estimated total shareholder yield of roughly 6% from dividends and buybacks.

Fair value: $116.00

Implied overvaluation: 4.8%

Forecast revenue growth: 5.49%

- Views Citi’s transformation and digital initiatives as positive but largely reflected in the price, with only modest upside compared with the analyst consensus target.

- Highlights risks from intense digital competition, regulatory pressure, high transformation costs, and execution challenges that could limit margins and RoTCE versus peers.

- Suggests current pricing already factors in mid single digit revenue growth and margin improvement, leaving limited room for disappointment without a potential pullback toward the $100 to $115 range.

Do you think there's more to the story for Citigroup? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com