- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

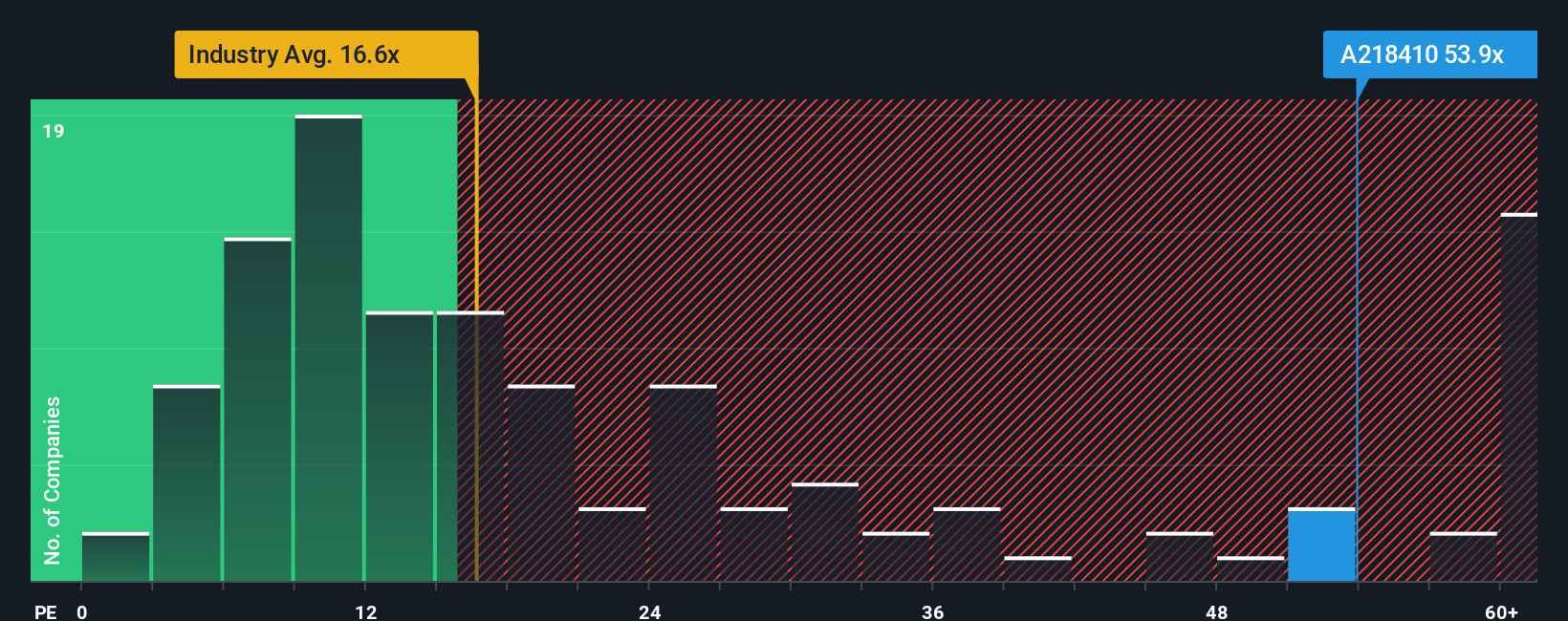

Wall Street JournalRFHIC Corporation (KOSDAQ:218410) Stocks Shoot Up 28% But Its P/E Still Looks Reasonable

RFHIC Corporation (KOSDAQ:218410) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. The last month tops off a massive increase of 157% in the last year.

Since its price has surged higher, given close to half the companies in Korea have price-to-earnings ratios (or "P/E's") below 13x, you may consider RFHIC as a stock to avoid entirely with its 53.9x P/E ratio. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

RFHIC could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

View our latest analysis for RFHIC

Is There Enough Growth For RFHIC?

There's an inherent assumption that a company should far outperform the market for P/E ratios like RFHIC's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 65% decrease to the company's bottom line. Even so, admirably EPS has lifted 269% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Turning to the outlook, the next year should generate growth of 77% as estimated by the three analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 38%, which is noticeably less attractive.

With this information, we can see why RFHIC is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On RFHIC's P/E

RFHIC's P/E is flying high just like its stock has during the last month. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that RFHIC maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

There are also other vital risk factors to consider before investing and we've discovered 2 warning signs for RFHIC that you should be aware of.

Of course, you might also be able to find a better stock than RFHIC. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.