- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMedpace (MEDP): Assessing Valuation After a Strong Multi‑Year Share Price Run

Medpace Holdings (MEDP) has quietly become one of the stronger long term performers in clinical research, with the stock up around 67% over the past year despite a recent pullback this month.

See our latest analysis for Medpace Holdings.

The recent pullback, including a roughly 7.5% 1 month share price return decline, comes after a powerful run in which the share price has climbed about 71% year to date and contributed to a three year total shareholder return of 174%. This suggests momentum is still firmly intact even as expectations reset at a share price of $571.86.

If Medpace’s run has you thinking about where else strong execution might be hiding, this could be a good moment to explore other promising healthcare stocks that are quietly building long term stories of their own.

With shares now trading above analyst targets but still showing solid double digit earnings growth, the key question is whether Medpace is quietly undervalued or if the market is already pricing in years of future expansion.

Most Popular Narrative: 5.5% Overvalued

With Medpace closing at $571.86 against a popular fair value estimate around $541.92, the narrative leans toward a moderately stretched valuation built on still resilient growth assumptions.

The analysts have a consensus price target of $423.636 for Medpace Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $510.0, and the most bearish reporting a price target of just $305.0.

Want to see what kind of revenue path, margin compression, and future earnings multiple are being baked into this fair value math, and why it still signals downside from here? Take a closer look at how these assumptions stack together before deciding whether the current share price really leaves any cushion.

Result: Fair Value of $541.92 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, resilient trial demand and disciplined buybacks could sustain earnings growth longer than expected, supporting a higher multiple and challenging today’s overvaluation case.

Find out about the key risks to this Medpace Holdings narrative.

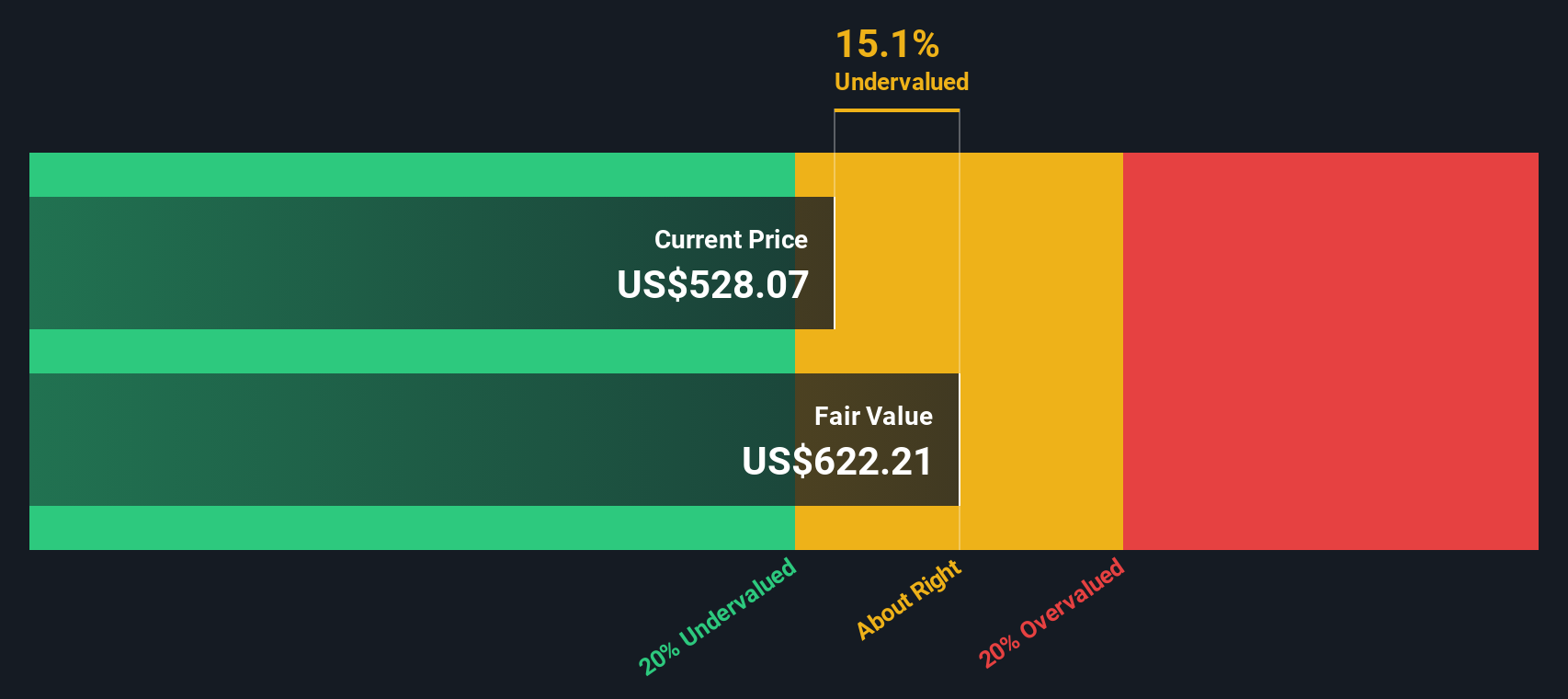

Another View: DCF Points to Hidden Value

While the analyst-based fair value implies Medpace is about 5.5% overvalued, our DCF model paints a different picture. It suggests shares are roughly 15.6% undervalued at $571.86 versus a fair value of $677.67. Which story better captures the next leg of this rally?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Medpace Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 905 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Medpace Holdings Narrative

If you see the story differently or want to dig into the numbers yourself, you can craft a custom view in just minutes: Do it your way.

A great starting point for your Medpace Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Before you move on, put Simply Wall Street’s powerful screener to work and uncover fresh, data driven ideas that could reshape your portfolio’s long term potential.

- Capture potential mispricings by targeting companies trading below intrinsic value with these 905 undervalued stocks based on cash flows, and position yourself ahead of a possible rerating.

- Ride structural growth trends by using these 24 AI penny stocks to focus on innovators harnessing artificial intelligence to scale profits and defend competitive moats.

- Strengthen your income stream by scanning these 10 dividend stocks with yields > 3% that combine dependable payouts with balance sheets built to handle tougher market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com