- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSchneider Electric (ENXTPA:SU): Revisiting Valuation After Recent Gains and Longer-Term Shareholder Returns

Schneider Electric (ENXTPA:SU) has been quietly grinding higher over the past month, adding about 6% even after a softer past week. That mix of short term noise and steady gains makes the current setup interesting.

See our latest analysis for Schneider Electric.

That recent 6.4% 1 month share price return sits against a slightly negative year to date move, while a modest 1 year total shareholder return of 0.7% caps a far stronger 3 year total shareholder return above 90%. This suggests Schneider Electric’s longer term momentum remains firmly intact even if near term sentiment is mixed.

If Schneider Electric’s steady compounding appeals to you, this could be a good moment to explore fast growing stocks with high insider ownership and see which other names are quietly building powerful long term stories.

With shares treading water this year despite solid double digit earnings growth and a healthy gap to analyst price targets, investors now face a key question: is Schneider Electric a mispriced compounder, or is the market already baking in years of future growth?

Most Popular Narrative Narrative: 13% Undervalued

With a fair value near €270 and the last close at €236.55, the most followed narrative points to meaningful upside if its assumptions play out.

The analysts have a consensus price target of €253.098 for Schneider Electric based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish ones reporting a price target of €289.0, and the most bearish reporting a price target of just €220.0.

Curious how steady, mid teens earnings growth and rising margins can still justify a premium multiple in a cyclical sector? The narrative spells out the earnings path, valuation bridge, and one crucial assumption that has to hold for this upside case to work. Want to see what the market might be missing in those projections?

Result: Fair Value of €270.55 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent margin pressure and a weaker-for-longer Industrial Automation recovery could quickly challenge the upbeat growth and valuation assumptions underpinning this narrative.

Find out about the key risks to this Schneider Electric narrative.

Another Angle on Valuation

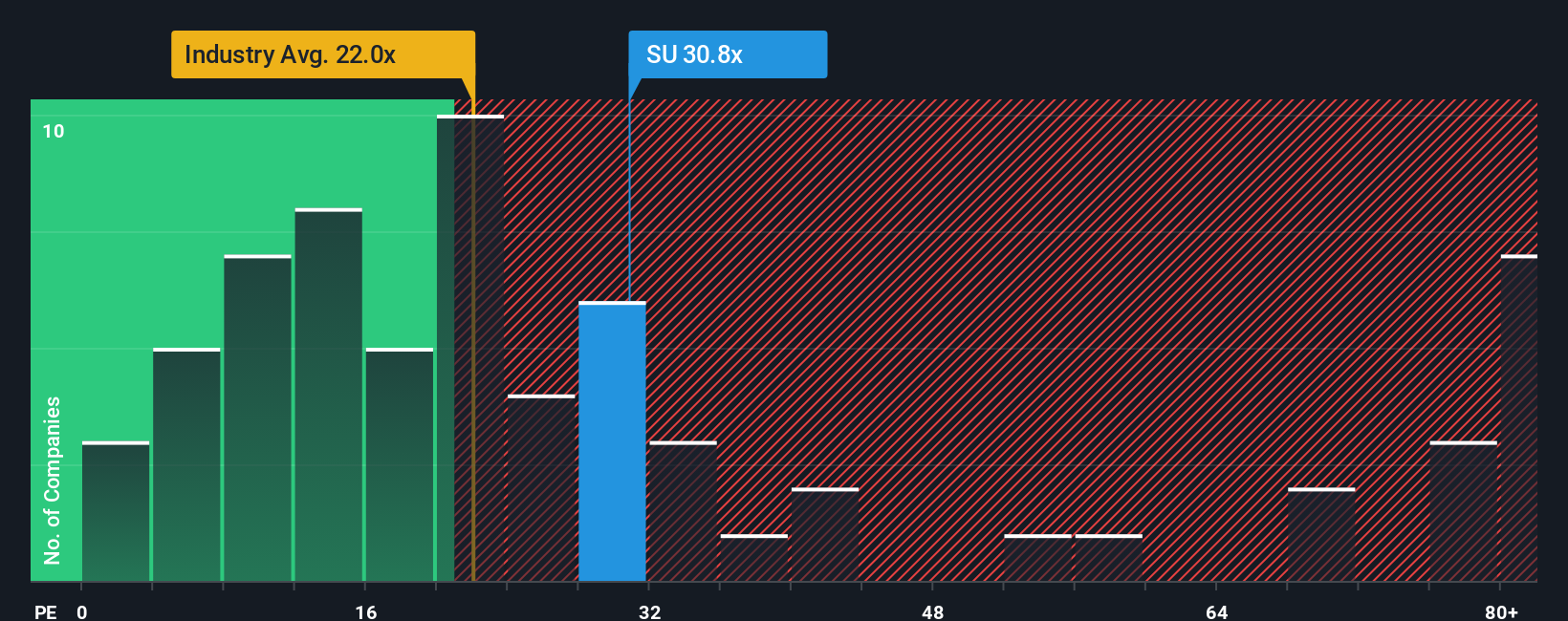

On earnings, Schneider Electric does not look cheap. It trades on a 30.9x price to earnings ratio versus about 24.5x for peers and 23.9x for the wider European Electrical industry, even though a fair ratio near 33.6x suggests the market could still push the multiple higher. Is that premium a cushion or a risk if growth stumbles?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Schneider Electric Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your Schneider Electric research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next smart move with a few targeted screeners that surface opportunities you will not want to overlook.

- Capture potential multi-baggers early by scanning these 3630 penny stocks with strong financials that already show strong financial foundations instead of just speculative hype.

- Ride structural growth trends by targeting these 29 healthcare AI stocks that blend resilient demand with cutting edge innovation in patient care and diagnostics.

- Strengthen your income stream by focusing on these 10 dividend stocks with yields > 3% that balance attractive yields with solid payout support and room for future increases.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com