Zhitong Special Offer | Hong Kong Stock Market Broker Panorama Analysis: Who controls pricing?

The Zhitong Finance App learned that Hong Kong, as an international financial center, has a complex and diverse structure of participants in the stock market. The brokers' real-time disclosure in the intraday market provides investors with a unique perspective, including understanding pricing rights and types of funds that fluctuate abnormally in individual stocks. The different types of brokers represent very different financial forces. Together, they shape the unique ecology and operating rules of Hong Kong stocks. Large-scale position transfers and storage data will also reveal quite a few trading opportunities. Behind almost every position transfer and deposit, a game involving major shareholders or major shareholders and financial institutions is included.

Part.01 Foreign Brokers: “The Master of the Sea” and “Agitators”

Foreign brokers and the international capital they represent play a key role in the Hong Kong stock market as stock leaders, core controllers of pricing power, global liquidity connectors, and providers of diversified trading strategies. Although the influence of southbound capital has increased in recent years, foreign brokers are still the most important force in determining the trend and ecological characteristics of the Hong Kong stock market due to their huge holdings and mature trading mechanisms.

1. Absolute stock dominance

Although southbound capital (Hong Kong Stock Connect) has continued to flow in recent years, judging from the stock market, foreign capital still dominates. According to the data, as of March 2025, international intermediaries (representing foreign investors) held 43.38% of the market value of Hong Kong stocks, far higher than Hong Kong Stock Connect (about 11.07%), Chinese intermediaries (8.06%), and local Hong Kong intermediaries (3.02%).

According to other data, as of August 2025, the share of foreign investors in the market value of Hong Kong stocks remained around 60%.

2. Significant head effect (Matthew effect)

Foreign brokers' holdings showed a high degree of concentration. Hong Kong Stock Exchange's top 20 escrow brokers (mainly major international banks such as HSBC, Citibank, and Standard Chartered Bank) have reached about 90% of their holdings. For example, as the largest broker, HSBC's holdings in some individual stocks are close to or even greater than the total holdings of Hong Kong Stock Connect.

3. Control over the pricing power of core assets

Since foreign investors hold a large amount of underlying positions in core assets such as Internet technology and finance, their trading behavior directly determines the valuation center of these weighted stocks. For example, in individual stocks such as Alibaba, Tencent, and China Mobile, the flow of foreign capital often dominates short-term fluctuations in stock prices. Even with large purchases of capital from the south, if there is a large outflow of foreign capital, the stock price may still be under pressure.

4. Capital flows driven by international macroeconomic factors

Hong Kong has a linked exchange rate system, where the Hong Kong dollar is linked to the US dollar. Foreign brokers are the main participants in the execution of HKD arbitrage transactions. When the US dollar interest rate is higher than the Hong Kong dollar interest rate, foreign investors tend to borrow Hong Kong dollars for arbitrage, causing capital to flow out of Hong Kong stocks; vice versa. This mechanism makes the liquidity of Hong Kong stocks highly dependent on the Federal Reserve's monetary policy.

Furthermore, foreign brokers' capital flows are highly sensitive to global geopolitics and risk premiums (such as the ERP difference between Hong Kong stocks and Japanese stocks and India). When global risk aversion heats up or geopolitical tension heats up, foreign capital often flows out first, leading to fluctuations in the Hong Kong stock market.

For example, since the September 24 market in 2024, according to statistics from Damo and Goldman Sachs, in fact, foreign capital entering and leaving the Hong Kong stock market is mainly hedge funds (Hedge Funds). The “old money” of long-term long term long term funds (Long Only) still has no specific capital entry due to geopolitical and fundamental factors.

5. The internal “dual nature” of foreign investment: long-term allocation and short-term transactions

Foreign capital is not a monopoly; there is a clear strategic differentiation within it. It can mainly be divided into two major groups: Long Only (Long Only) and Hedge Fund (Hedge Fund):

As active market players, hedge funds (HF) have the following notable characteristics:

Exchange rate sensitivity: HF is extremely sensitive to the US dollar index and the Hong Kong dollar exchange rate. When the US dollar strengthens or the spread between the US and Hong Kong widens, HF often carries out Hong Kong dollar arbitrage transactions (selling Hong Kong dollar assets to buy US dollars), leading to a rapid outflow of capital from Hong Kong stocks. The data shows that during the weakening of the US dollar from May to July 2025, HF returned for a short time, but then quickly flowed out due to the rebound of the US dollar.

Geopolitical game: HF is the fastest to respond to geopolitical risks (such as Sino-US relations and the situation in the Taiwan Strait). Once the risk premium rises, HF is usually the first batch of funds to be withdrawn, causing sharp short-term market fluctuations.

Part.02 Chinese Brokers: The Rising “Marginal Power”

The capital behind Chinese brokers mainly comes from the mainland. As of December 2025, Hong Kong Stock Connect accounted for about 14.6% of the stock market value, and Hong Kong subsidiaries of Chinese brokerage firms, such as Haitong International, held about 8% of the stock market value. This power is also the most important marginal incremental capital and pricing force for Hong Kong stocks.

1. Internal differences in Chinese capital: Shanghai and Shenzhen-Hong Kong Stock Connect

Similar to the structure of foreign capital, there are also obvious differences in investment preferences: the Shanghai-Hong Kong Stock Connect mainly focuses on long-term allocation funds such as insurance, and favors high-dividend defense; the Shenzhen-Hong Kong Stock Connect mainly focuses on transactional funds such as public and private equity, and favors technological growth.

2. Characteristics of “reverse operation” with foreign investment

Unlike foreign capital, when there is a large outflow of foreign capital due to geopolitical or exchange rate fluctuations, south-bound capital often increases net purchasing power. For example, in the midst of a sharp decline in April 2025, when foreign investors drastically sold the Internet leader, south-bound capital continued to make net purchases, showing the reverse investment characteristics of “others are afraid of me and I am greedy.”

Part.03 Local Brokers: Once Surprised

Local intermediaries in Hong Kong, such as Phillip, Yao Cai, Sun Hung Kai Finance, Emperor, Fu Cheong Securities, etc., currently hold only about 3% of the market value of Hong Kong stocks, and basically only serve local retail and high-net-worth customers in Hong Kong.

Its main holdings are also concentrated in local companies in Hong Kong, especially small market capitalization companies. Although its overall influence is limited, it still plays an important role in local small-cap trading.

Interpretation of market signals: Looking at funding intentions from the perspective of seats

The big difference between Hong Kong stocks and A-shares is that you can see the trading buyers' seats in real time. Learning to check the nature of the different seats can largely determine whether this stock is trending or trading.

“Discerning right and wrong” for foreign investment seats

Take foreign brokers as an example. Hedge funds (HF) and long-term allocation funds (LO) almost always use different seats. By observing the trading behavior of these seats, investors can help determine the nature of capital and market trends:

Therefore, if it is a short-term transaction, more attention is paid to investment bank seats such as Damo and Goldman Sachs, while bank seats such as HSBC and Citibank are more likely to show trending opportunities. After all, pensions, sovereign wealth funds, etc. are more likely to break out of the medium- to long-term trend due to the huge amount of capital and long assessment cycles.

For example, the following are some typical cases

Goldman Sachs trading desk records:

“On May 12, 2025, stimulated by favorable news of lower tariffs between China and the US, Goldman Sachs's Proprietary Trading Division (SB) surged to US$2.4 billion in a single day (a new high since 2021), using the favorable news to decisively settle short-term profits; at the same time, its trading desk bought high-beta stocks such as Kuaishou from small hedge funds to rebound. This large-scale reverse operation within the same time window typically reflects the short-term gaming nature of investment bank seats.”

Note: Seat analysis is not infallible. Major players or bookmakers will also use foreign seats to confuse the market, the so-called “bypass capital.” This portion of capital is usually used to borrow quotas and seats from foreign banks in the form of derivatives such as revenue swaps (TRS). On the surface, they are bought by foreign banks; in fact, they are mainland customers. Although they place orders through seats at foreign banks (such as Goldman Sachs and UBS), their trading style is often strongly influenced by mainland investment (such as violent uptake, etc.), which can easily mislead the market into thinking that foreign investors are grabbing funds.

The way to tell the difference is to go back to common sense and think:

For long-term investors, since their requirements for yield are generally not that high, they pay more attention to the stability of performance and manageable risks, so it is unlikely that they will rush to raise funds.

Even for short-term capital such as quantification of hedge funds, if there is a rush to raise funds on the same day, and when the stock price fluctuates negatively, these seats will inevitably be sold symmetrically due to maintaining the “trend trading” style. If not, it's probably fake foreign investment.

Part.04Hong Kong Stock Specific Mechanisms: Deposit and Transfer

“Deposit” and “transfer” in the Hong Kong market are the core links of securities custody, settlement and cross-border transactions. The Hong Kong stock market has an indirect holding system with the central settlement system (CCASS) as the core, and the vast majority of shares in circulation are held on behalf of intermediaries.

The underlying escrow structure for Hong Kong stocks

The Hong Kong market implements a multi-level holding system based mainly on indirect holding methods:

Electronic depository: Currently, most investors' shares in the Hong Kong market are deposited in the Hong Kong Stock Exchange's Central Clearing and Settlement System (CCASS) and held on behalf of customers by intermediaries (such as brokerage firms and banks).

Nominal holder: In the CCASS system, shares are registered in the shareholder register of listed companies under the name “Hong Kong Central Clearing (Agent) Limited”.

Part.05 Warehousing: The transformation from paper to electronic

“Deposit” generally refers to the process of depositing physical stock certificates into the CCASS system and converting them into electronic shares for trading in the secondary market. In movies and TV dramas depicting the Hong Kong stock market in the early days, there are many dramas that directly take unregistered paper stocks. Unlike the mainland, Hong Kong still has a large number of paper stocks.

Trading premise: Physical stocks (paper stocks) of Hong Kong stocks cannot be directly traded within the exchange system. Investors must first deposit physical stocks into a CCASS account through the brokerage channel, then convert them to electronic stocks before they can trade.

Operation process: Investors holding physical stocks must deliver the stock certificate and signed transfer forms (Transfer Forms) to their broker or custodian before the settlement date and deposit them in CCASS on their behalf.

Time period:

Electronic shares: If the transfer is made within the CCASS system, it usually takes 2 working days.

Physical storage: If physical stock deposit and verification is involved, the entire process can take 14 business days or more.

Part.06 Significance of market signals of storage (signs of majority shareholders' holdings reduction)

Unban and cash out: The cornerstone investors or majority shareholders in the early stages of an IPO often hold physical stocks. When the ban period ends (the ban is lifted) and shareholders are willing to cash out, they must first convert “paper stocks” into “electronic shares” and deposit them into CCASS.

Monitoring metrics: Therefore, market analysts often predict the majority shareholders' intention to reduce holdings by tracking sudden increases in positions (storage behavior) of specific broker seats in the CCASS database. For example, before a shareholder reduced their holdings, the market monitored large-scale transfer/deposit data, which is regarded as a leading indicator of a reduction in holdings.

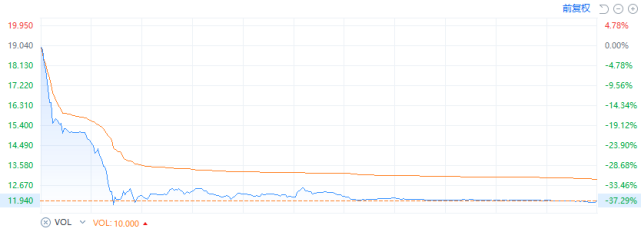

Take Starry Sky Chinese (06698) as an example. The stock price plummeted by more than 37% in a single day after deposit, which was already evident the day before.

Part.07 Transfer: Generally refers to the transfer of shares between brokerage firms

“Transferring positions” is better understood. Shares from Broker A are about to be transferred to Broker B. Generally, the act of transferring positions is more often accompanied by business requirements such as stock pledges. The rollover itself usually does not directly affect stock prices, but large transfers may suggest shareholders' financing needs or investment strategy adjustments.

In particular, it is necessary to pay attention to which bank positions are transferred to brokerage firms, especially small brokerage seats. Many of them are due to equity pledges by major shareholders, and it is easy to collapse after a continuous decline.

For example, recently, HSSP INTL (03626) saw a roller coaster market on October 31, with a one-day amplitude of 95% and a sharp drop of 61.28% at the end of the session. In fact, there was an abnormal transfer behavior as early as October 22.

Part.08Understanding Market Participants and Seizing Investment Initiatives

The appeal of the Hong Kong stock market is its highly international and diverse participant structure. From major foreign investors that control pricing, to rising south-bound capital, to local brokers, each type of participant has its own unique behavioral pattern and market influence.

For investors, an in-depth understanding of the characteristics and trends of these participants can not only help interpret market signals, but also seize investment initiative in a complex and changing market environment. Whether it is judging the nature of capital through seat analysis or predicting the behavior of major shareholders through deposit data, this expertise will be a powerful tool for investors to overcome difficulties in the Hong Kong stock market.