- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHow EMCOR’s Bigger Dividend, Buybacks and Guidance Hike At EMCOR Group (EME) Has Changed Its Investment Story

- EMCOR Group, Inc. recently approved a 60% increase in its regular quarterly dividend to US$0.40 per share from US$0.25, with the higher payout expected to begin in the first quarter of 2026 alongside an expanded US$500.00 million share repurchase program and higher 2025 earnings guidance.

- This combination of a larger dividend, additional buyback capacity, and raised profit outlook highlights management’s confidence in EMCOR’s cash generation and long-term earnings power.

- We’ll now examine how the sharply higher dividend payout could reshape EMCOR Group’s investment narrative and appeal to investors.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

EMCOR Group Investment Narrative Recap

To own EMCOR Group, you have to believe its diversified construction and services platform can keep converting project demand into steady cash generation, even as labor, energy, and end-market cycles shift. The sharply higher dividend and expanded buyback do not materially change the key near term catalyst, which is continued execution on its strong project backlog, nor the biggest risk, which remains cost and margin pressure from tight labor markets and rising wages.

Among recent announcements, the upward revision to 2025 earnings guidance stands out alongside the dividend hike, as both are tied to EMCOR’s ability to sustain revenue growth and profitability from large, complex projects. That same concentration in project driven revenue, particularly in cyclical industrial and high tech manufacturing work, can amplify earnings swings if awards slow or sector momentum cools, which matters when investors are reassessing the stock’s income appeal.

Yet while the upgraded dividend story is appealing, investors should be aware of how persistent labor cost pressures could affect margins and cash flows over time...

Read the full narrative on EMCOR Group (it's free!)

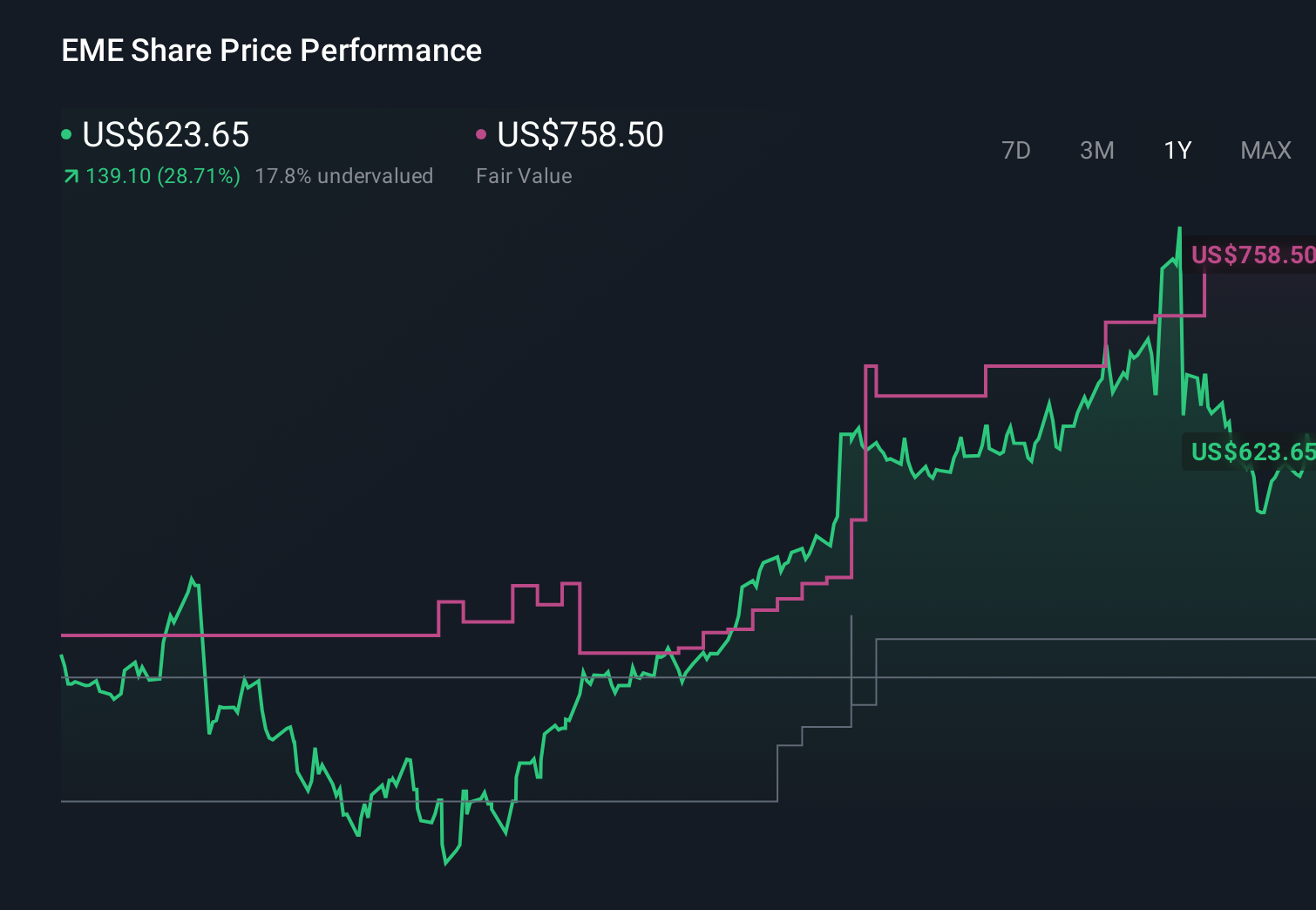

EMCOR Group's narrative projects $20.6 billion revenue and $1.4 billion earnings by 2028.

Uncover how EMCOR Group's forecasts yield a $758.50 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Eight fair value estimates from the Simply Wall St Community range from US$468.79 to US$912.02, underscoring how far apart individual views can be. When you set that against the current focus on EMCOR’s dividend increase and buyback capacity, it becomes even more important to weigh how labor cost inflation and project volatility could influence the company’s ability to support those shareholder returns over time.

Explore 8 other fair value estimates on EMCOR Group - why the stock might be worth as much as 49% more than the current price!

Build Your Own EMCOR Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your EMCOR Group research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free EMCOR Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate EMCOR Group's overall financial health at a glance.

Contemplating Other Strategies?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 12 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com