Assessing Banco Santander’s (BME:SAN) Valuation After a Strong Multi-Year Share Price Rally

Banco Santander (BME:SAN) has quietly turned into one of the stronger stories in European banking, with the share price climbing about 13% over the past month and roughly 16% in the past 3 months.

See our latest analysis for Banco Santander.

Zooming out, the latest move builds on hefty momentum, with a year to date share price return of more than 120% and a three year total shareholder return nearing 300%. This suggests investors are steadily re-rating Santander’s growth and risk profile.

If Santander’s renewed momentum has you rethinking the sector, it could also be a good moment to scout other well positioned solid balance sheet and fundamentals stocks screener (None results).

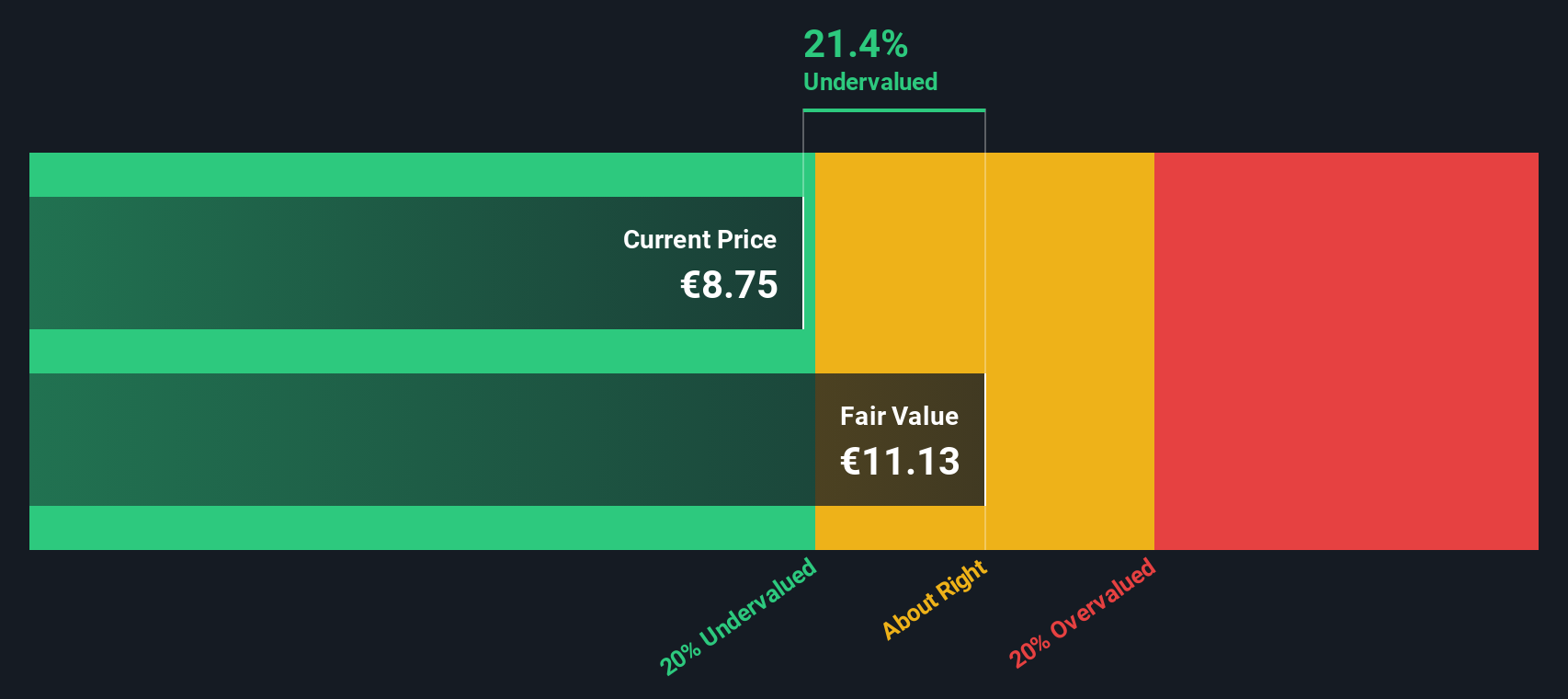

Yet despite that surge, Santander still trades at a meaningful discount to some fair value estimates and its earnings are growing steadily. So is there more upside to capture here, or is the market already banking on further growth?

Most Popular Narrative: 4.6% Overvalued

Compared with the last close at €9.97, the most followed fair value estimate of €9.53 implies a modest premium baked into today’s price.

The analysts have a consensus price target of €7.997 for Banco Santander based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €9.5, and the most bearish reporting a price target of just €5.8.

Want to see what is driving that higher long run earnings base and richer future multiple assumptions? The full narrative lays out the revenue runway, margin path, and valuation bridge in detail.

Result: Fair Value of €9.53 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent loan quality pressures in Brazil, along with heightened regulatory or litigation risks, could quickly undermine the current growth and valuation narrative.

Find out about the key risks to this Banco Santander narrative.

Another Angle on Value

Our numbers tell a different story. Based on our SWS DCF model, Santander’s shares look around 17% undervalued at €9.97 versus an estimated fair value of about €11.98. If cash flows point to upside while the narrative flags mild overvaluation, which signal do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Banco Santander Narrative

If you would rather dig into the numbers yourself and shape your own view, you can build a personalized narrative in minutes: Do it your way.

A great starting point for your Banco Santander research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Ready for your next investing move?

Do not stop at one strong bank. Use the Simply Wall Street Screener to pinpoint focused opportunities that match your goals before other investors react.

- Capture potential multi-bagger opportunities early by zeroing in on these 3634 penny stocks with strong financials with improving fundamentals and room to grow.

- Position your portfolio for the next wave of innovation by targeting these 24 AI penny stocks shaping automation, data intelligence and digital transformation.

- Lock in potential value before the crowd notices with these 914 undervalued stocks based on cash flows that trade below their estimated cash flow worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com