Undiscovered Gems in Asia Promising Stocks for December 2025

As global markets adjust to the Federal Reserve's recent interest rate cut and mixed economic signals, small-cap stocks have shown resilience, particularly in the U.S., with the Russell 2000 Index outperforming its larger peers. In this dynamic environment, identifying promising stocks in Asia requires a keen eye for companies that can navigate shifting monetary policies and capitalize on regional growth opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Dear LifeLtd | 53.23% | 18.86% | 15.70% | ★★★★★★ |

| Central Forest Group | NA | 5.20% | 24.71% | ★★★★★★ |

| Kanda HoldingsLtd | 23.54% | 3.84% | 10.38% | ★★★★★★ |

| Nice | 78.50% | 1.97% | 13.44% | ★★★★★☆ |

| Anhui Huaren Health Pharmaceutical | 55.17% | 17.65% | 10.18% | ★★★★★☆ |

| Huasi Holding | 6.89% | 4.80% | 41.72% | ★★★★★☆ |

| Tai Sin Electric | 37.42% | 10.92% | 7.66% | ★★★★☆☆ |

| Jiangxi Jiangnan New Material Technology | 68.65% | 15.68% | 14.93% | ★★★★☆☆ |

| Sichuan Zigong Conveying Machine Group | 54.32% | 21.85% | 16.70% | ★★★★☆☆ |

| Zhejiang Bofay Electric | 39.35% | -1.41% | -47.96% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Sumec (SHSE:600710)

Simply Wall St Value Rating: ★★★★★★

Overview: Sumec Corporation Limited operates in the supply and industrial chain business in China, with a market cap of CN¥14.06 billion.

Operations: The company generates its revenue primarily through its supply and industrial chain operations in China. It has a market capitalization of CN¥14.06 billion.

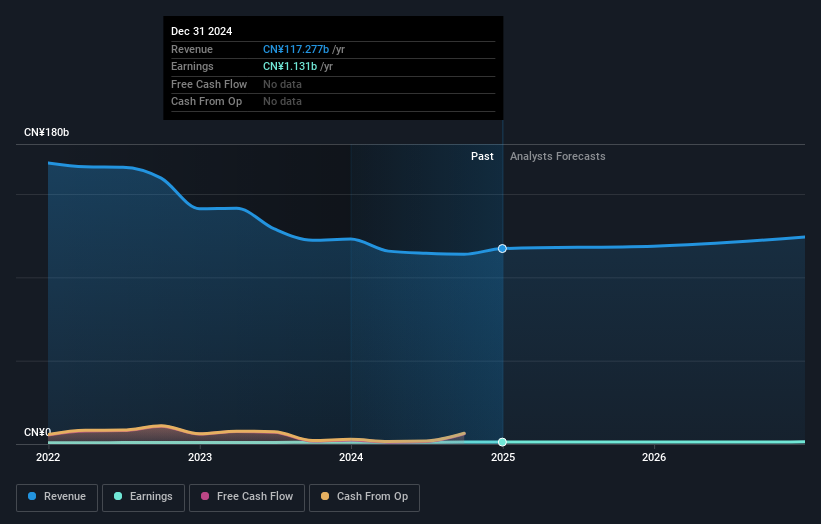

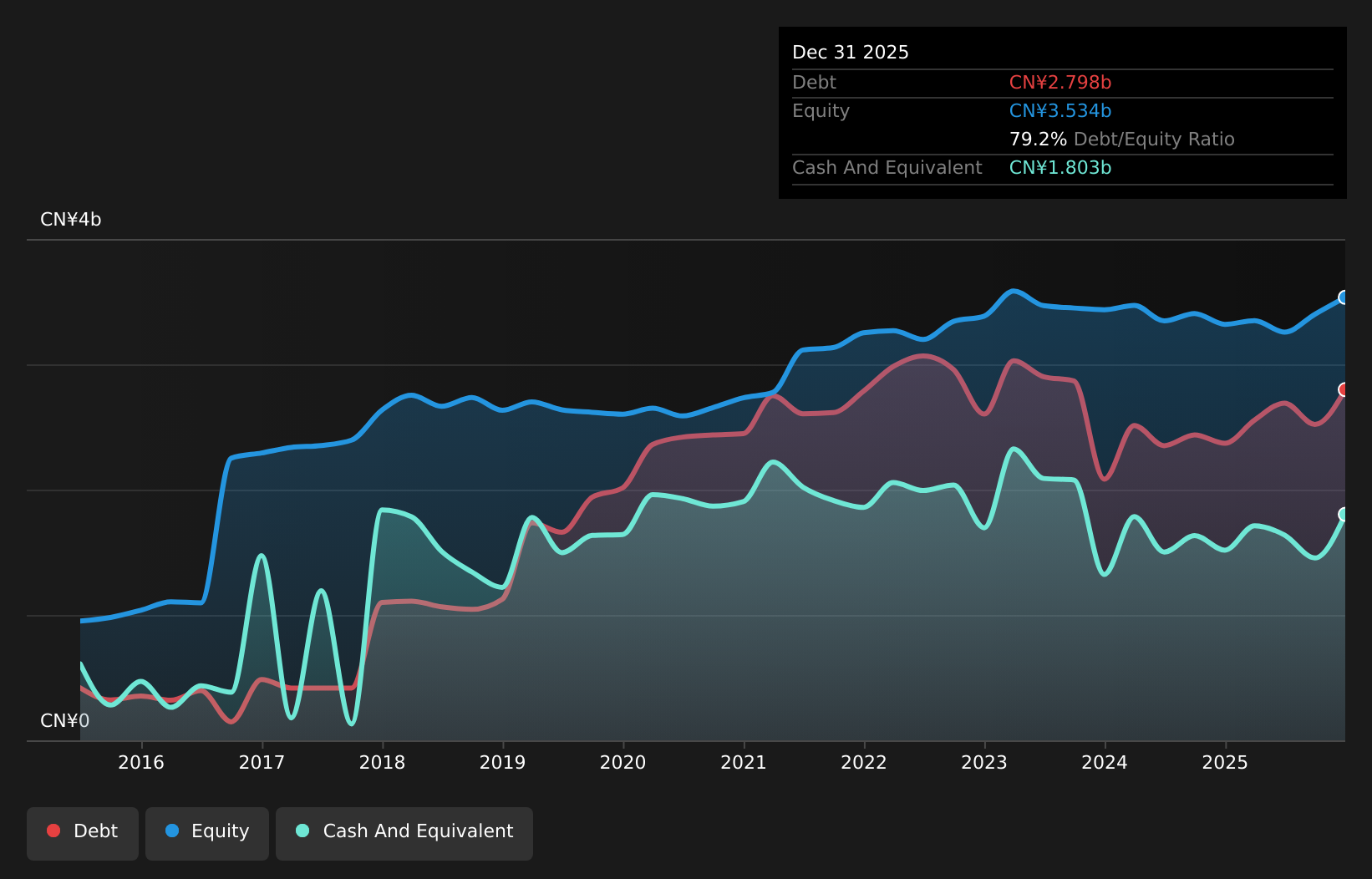

Sumec's earnings growth of 9.8% over the past year outpaced the Trade Distributors industry, which saw a -12.9% change, highlighting its robust performance in a challenging sector. The company reported net income of CNY 1,103.69 million for the first nine months of 2025, up from CNY 1,003.08 million last year. Trading at a significant discount—67.1% below estimated fair value—Sumec seems undervalued compared to peers and industry standards. Notably, its debt-to-equity ratio has improved dramatically from 81.3% to just 22.6% over five years, suggesting effective financial management and potential for future growth.

- Delve into the full analysis health report here for a deeper understanding of Sumec.

Gain insights into Sumec's historical performance by reviewing our past performance report.

Tianshui Zhongxing Bio-technologyLtd (SZSE:002772)

Simply Wall St Value Rating: ★★★★★☆

Overview: Tianshui Zhongxing Bio-technology Co., Ltd. is involved in the research, development, production, and sale of edible fungi both in China and internationally, with a market capitalization of approximately CN¥5.36 billion.

Operations: The company generates its revenue primarily from the agricultural planting industry, with reported revenues of approximately CN¥1.99 billion.

Tianshui Zhongxing Bio-technology, a promising player in the biotech sector, has seen its earnings soar by 235% over the past year, outpacing the broader food industry growth of 4.8%. The company's net income for the first nine months of 2025 reached CNY 204 million, significantly up from CNY 89 million a year prior. With a price-to-earnings ratio of 22x, it remains attractively valued compared to China's market average of 42.9x. Its debt management is commendable with a reduced debt to equity ratio from 91.8% to 74.1% over five years and an interest coverage of nearly sixteen times EBIT.

Hisamitsu Pharmaceutical (TSE:4530)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hisamitsu Pharmaceutical Co., Inc. focuses on the manufacturing and sale of pharmaceuticals in Japan, with a market cap of ¥304.63 billion.

Operations: The company generates revenue primarily from the sale of pharmaceuticals in Japan. Its financial performance is influenced by factors such as production costs and market demand for its products. The market cap stands at ¥304.63 billion, reflecting its position within the industry.

With a notable presence in the pharmaceutical sector, Hisamitsu Pharmaceutical has shown robust earnings growth of 34% over the past year, outpacing the industry average of 9.6%. Trading at a significant discount, it stands 53.5% below its estimated fair value. The company is financially sound with more cash than total debt and positive free cash flow. Recent strategic moves include completing a share buyback program worth ¥12.27 billion, enhancing shareholder value. Furthermore, they have increased dividends to ¥45 per share from ¥43 previously, reflecting confidence in their financial health and future prospects.

- Click here to discover the nuances of Hisamitsu Pharmaceutical with our detailed analytical health report.

Gain insights into Hisamitsu Pharmaceutical's past trends and performance with our Past report.

Where To Now?

- Delve into our full catalog of 2502 Asian Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com