- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalChina Automobile Dealers Association: Passenger car terminal sales are expected to be around 2.35 million units in December

The Zhitong Finance App learned that the China Automobile Dealers Association issued an article stating that in December, manufacturers and dealers will continue to increase terminal promotions in order to sprint to the annual goal; at the same time, some demand for car purchases before the Spring Festival has also begun to be gradually released. For first-time car buyers, the preferential NEV purchase tax policy is about to decline, and it still forms a strong driving force for year-end car purchases. However, considering the industry's general expectation that the “two new” policies will continue next year, and the effect of car companies' new energy “purchase tax underwriting” plans to stabilize expectations, part of the replacement demand will shift to January next year. Combining the above factors, it is expected that the terminal consumer market will show a moderate upward trend in December, but it is difficult to form a significant “backward” market. Combined with the sales volume in November and the level of dealer data growth in the first half of December, it is estimated that passenger car terminal sales will be around 2.35 million units for the whole month of December.

Passenger car terminal retail sales are expected to reach 23.55 million in 2025, which is basically the same as 2024.

At the end of the year, replacement subsidy policies were tightened in many places, and the impact of car companies on the “purchase tax back-up” of new energy sources increased. The retail sales volume of passenger car terminals fell short of expectations in November, and there was a slight decline in market sales compared to October.

The start of the passenger car market in December was lackluster. The expiration of the new energy purchase tax exemption policy at the end of the year (halved from 2026) and the end of the two new policies failed to have a significant “last-minute effect.” As the subsidy funds for the two new policies in many places have basically been exhausted, demand for replacement and renewal is weak. Coupled with the late Spring Festival next year and the continuation of the “purchase tax bottom” subsidy program for new energy by some car companies, consumers currently have a strong wait-and-see attitude. As a result, although there may be a brief spike in sales in late December due to a decline in new energy purchase tax subsidies, it is expected that it will be difficult for the car market to show a clear “backward” market over the entire month.

Recently, the Central Economic Work Conference mentioned adhering to domestic demand leadership and building a strong domestic market. Optimize the implementation of “two new” policies (that is, large-scale equipment renewal and consumer goods trade-in). The industry generally expects that the “national subsidy” policy for trade-in automobile products will continue to be implemented next year.

According to data from the Ministry of Commerce, in January-November of this year, consumer goods trade-in drove sales of related products exceeding 2.5 trillion yuan, of which over 11.2 million cars were traded; combined with the Passenger Link branch data, passenger cars have sold a total of 21.483 million units since this year. This means that replacement sales driven by the “national subsidy” policy already accounted for more than one-half of the overall market, and the effect of boosting automobile consumption is remarkable. Taken together, the continuation of “state subsidies” next year will continue to boost automobile consumer demand, but this expectation will affect the market in December this year in reverse, compounding the car companies' new energy “purchase tax back-up” policies. Some consumers, especially those with replacement needs, may slow down the pace of car purchase decisions.

Based on the dealer's feedback on customer attraction, sales volume, and inventory biweekly report data, it can be seen that:

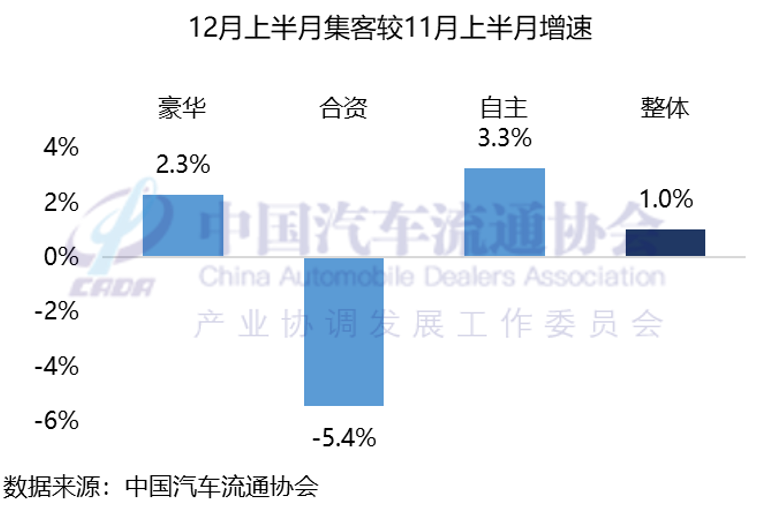

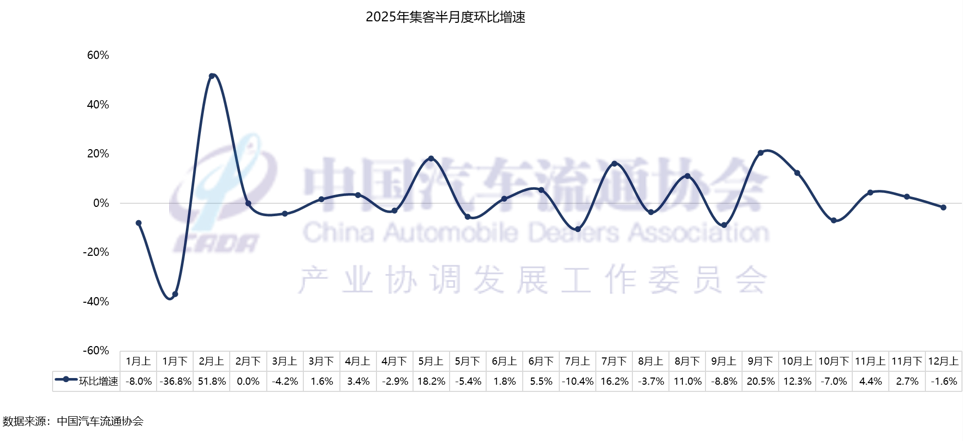

The number of visitors attracted in the first half of December increased slightly by 1.0% compared to the same period in November, and decreased by 1.6% compared to the second half of November. In late November, the Guangzhou International Auto Show began, and some new cars and facelift models were launched, driving an increase in passenger traffic; although passenger traffic declined in the first half of December compared to the second half of November, passenger traffic increased slightly compared to the first half of November, driven by dealers' “Double 12” activities and the decline in new energy purchase tax subsidies at the end of the year.

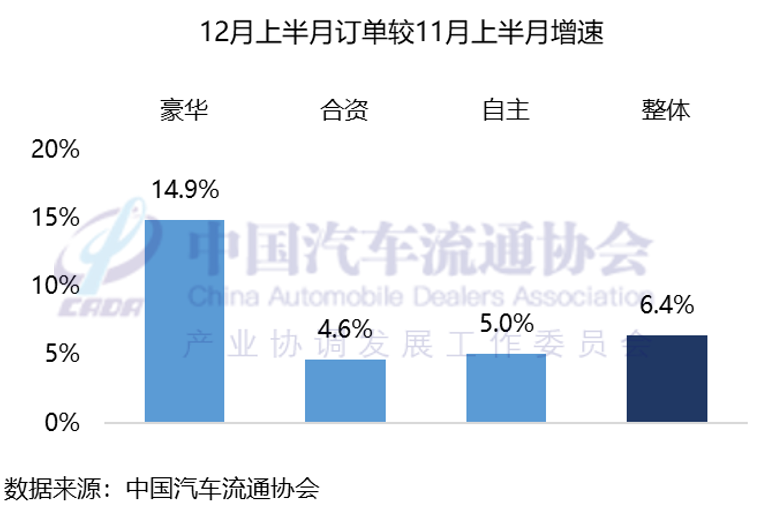

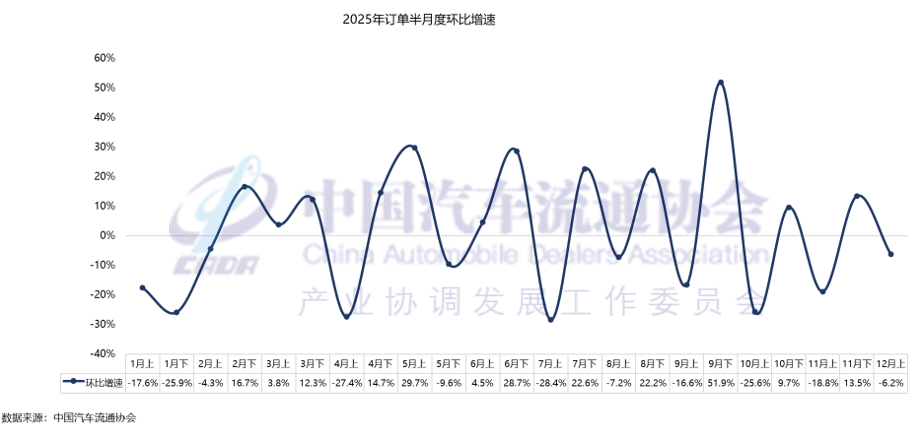

Orders in the first half of December increased by 6.4% compared to the same period in November and decreased by 6.2% compared to the second half of November. Compared to the first half of November, the first half of December was closer to the end of the year. The pace of dealer sales accelerated significantly, and promotions were further strengthened. Various facelifted models were launched before and after the Guangzhou Auto Show, which also led to an increase in order growth in the second half of November and the first half of December. Recently, many local governments introduced various forms of car purchase subsidy policies: Hubei issued an additional batch of car replacement and renewal subsidy vouchers; Zhengzhou co-ordinated additional consumer goods trade-in capital of 157 million yuan to continue the 2025 Zhengzhou car scrapping renewal campaign; Shenyang, Dalian, Qingdao and other places have introduced winter/year-end car purchase consumption subsidies. Combined with the policy effects of declining new energy purchase tax subsidies, and the majority of car companies' new energy “purchase tax underwriting” plans to complete car orders by the end of December, this will encourage some consumers, especially first-time buyers, to speed up their purchasing decisions. It is expected that orders will continue to rise in the second half of December.

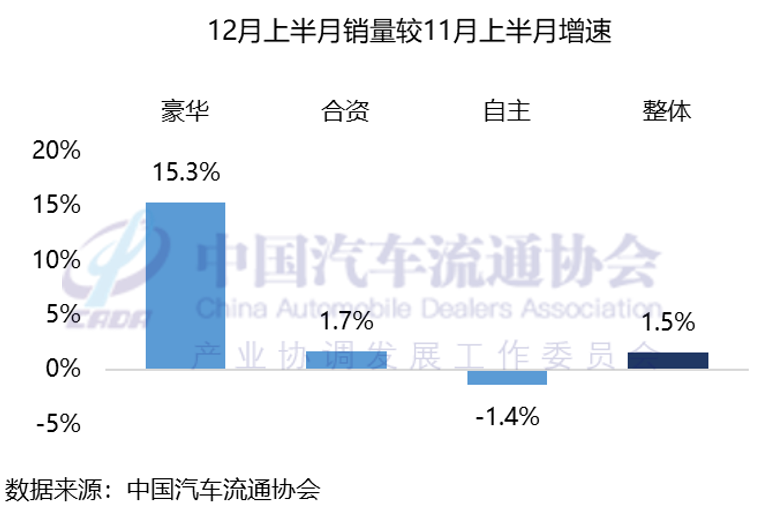

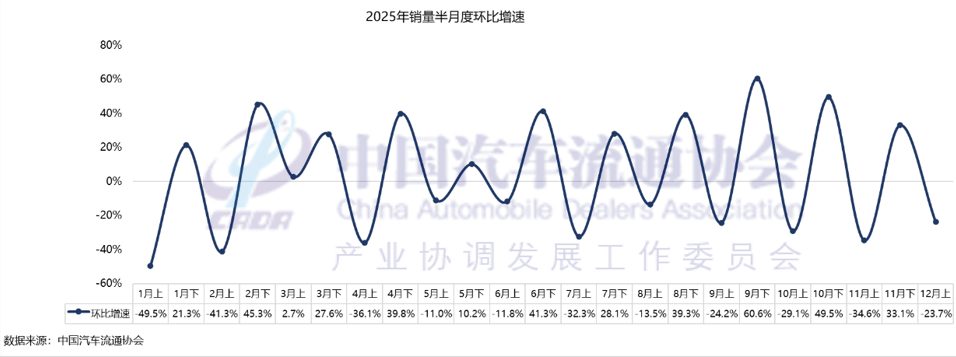

Sales in the first half of December increased by 1.5% compared to the same period in November, and decreased by 23.7% from the second half of November. Sales declined significantly in the first week of December, and market sales began to pick up in the second week, driven by dealers' “Double 12” promotions and year-end car purchase subsidies introduced one after another in various regions. As the end of the year approaches, demand for car purchases before the Spring Festival will gradually be released, and the expiration of the new energy purchase tax exemption policy will also encourage some consumers, especially first-time buyers, to complete car purchases before the end of the year. Overall sales are expected to continue growing in the second half of December.

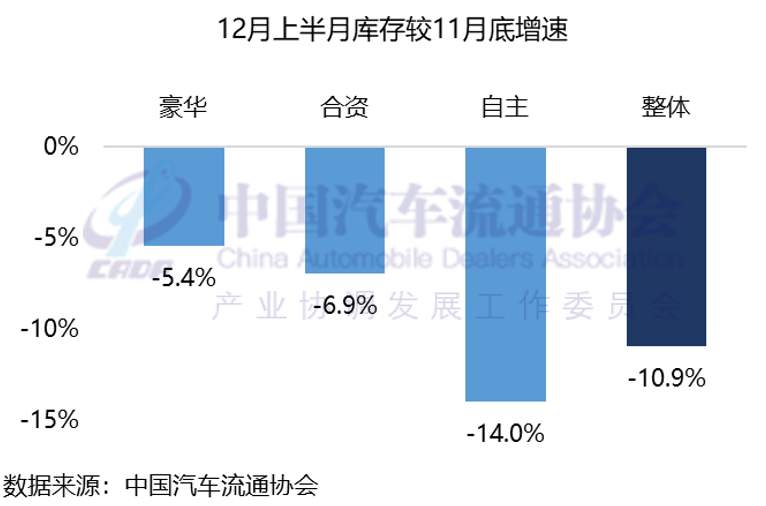

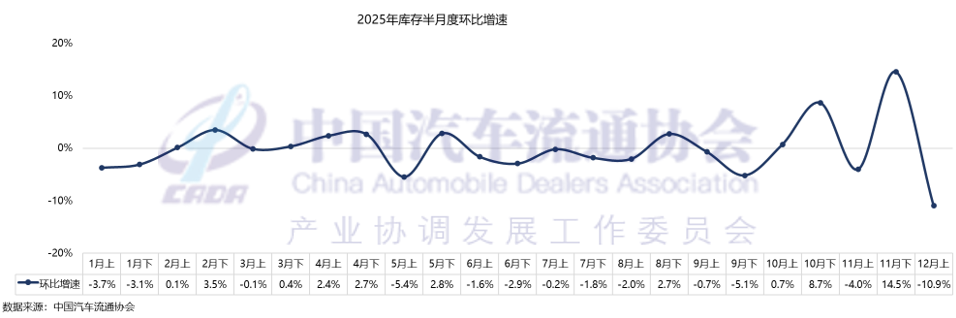

Inventory for the first half of December fell 10.9% from the end of November. At the end of November, due to the impact of end-of-year impulse replenishment and the decline in local replacement subsidy policies, dealer inventory levels rose rapidly and pressure increased; in December, dealers accelerated their sales pace, and mid-month inventory levels declined from the end of November.