- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalRevenues Not Telling The Story For Oncoclínicas do Brasil Serviços Médicos S.A. (BVMF:ONCO3) After Shares Rise 38%

Oncoclínicas do Brasil Serviços Médicos S.A. (BVMF:ONCO3) shareholders are no doubt pleased to see that the share price has bounced 38% in the last month, although it is still struggling to make up recently lost ground. Notwithstanding the latest gain, the annual share price return of 9.3% isn't as impressive.

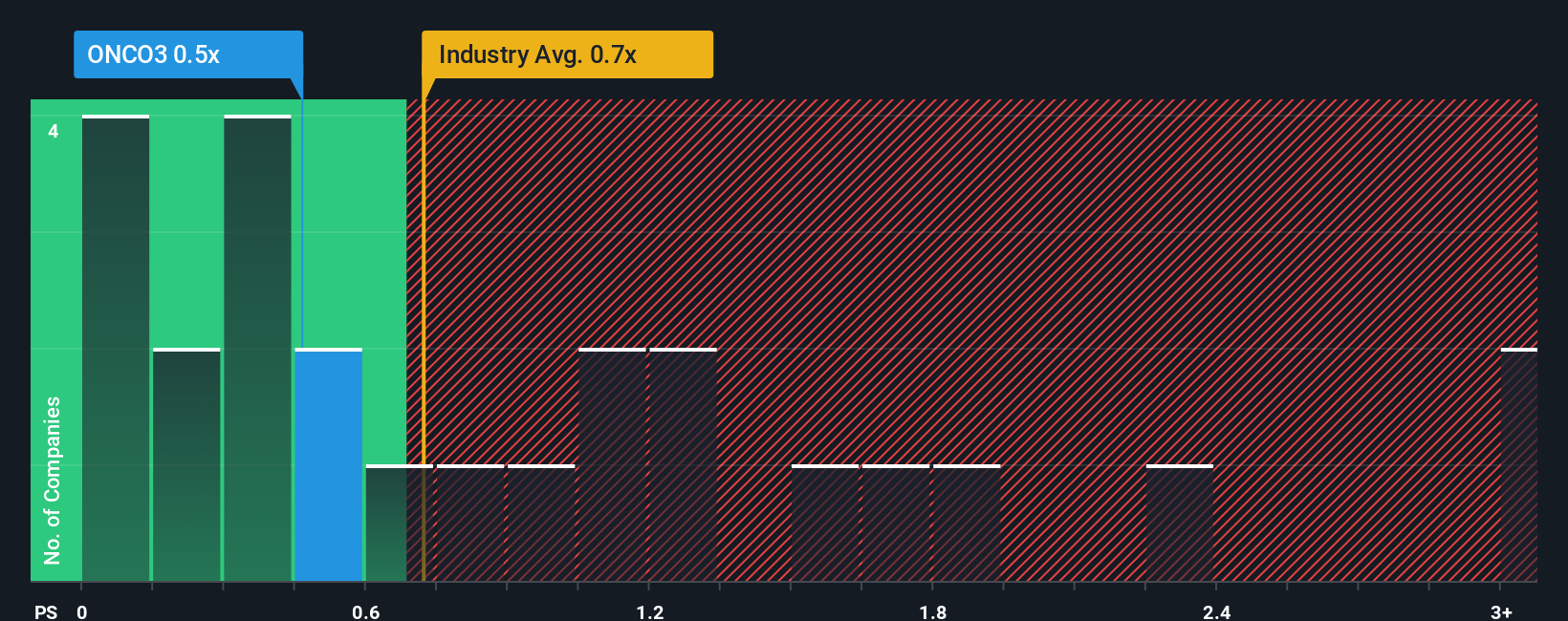

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Oncoclínicas do Brasil Serviços Médicos' P/S ratio of 0.5x, since the median price-to-sales (or "P/S") ratio for the Healthcare industry in Brazil is about the same. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Check out our latest analysis for Oncoclínicas do Brasil Serviços Médicos

How Oncoclínicas do Brasil Serviços Médicos Has Been Performing

While the industry has experienced revenue growth lately, Oncoclínicas do Brasil Serviços Médicos' revenue has gone into reverse gear, which is not great. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Oncoclínicas do Brasil Serviços Médicos.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Oncoclínicas do Brasil Serviços Médicos' is when the company's growth is tracking the industry closely.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.6%. Even so, admirably revenue has lifted 63% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 5.7% per annum as estimated by the six analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 11% each year, which is noticeably more attractive.

In light of this, it's curious that Oncoclínicas do Brasil Serviços Médicos' P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Bottom Line On Oncoclínicas do Brasil Serviços Médicos' P/S

Oncoclínicas do Brasil Serviços Médicos' stock has a lot of momentum behind it lately, which has brought its P/S level with the rest of the industry. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that Oncoclínicas do Brasil Serviços Médicos' revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

Having said that, be aware Oncoclínicas do Brasil Serviços Médicos is showing 2 warning signs in our investment analysis, you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.