Leggett & Platt (LEG): Assessing Valuation After a 29% One-Month Share Price Rebound

Why Leggett & Platt Is Back On Investors Radar

Leggett & Platt (LEG) has quietly jumped roughly 29% over the past month after a long slump, drawing fresh attention to whether this cyclical manufacturer is simply bouncing or starting a more durable recovery.

See our latest analysis for Leggett & Platt.

That 29.2% 1 month share price return has come after a long stretch of weak total shareholder returns, with the recent bounce suggesting sentiment might be turning as investors reassess LEG around $11.32.

If LEG’s rebound has you rethinking where value might emerge next, this could be a good moment to explore fast growing stocks with high insider ownership for other under the radar opportunities.

After years of lagging returns and only modest growth in the top and bottom line, LEG’s sharp rebound and slight premium to intrinsic value raises the key question: is there still a buying opportunity here, or is the market already pricing in a turnaround?

Most Popular Narrative Narrative: 2.9% Overvalued

With Leggett & Platt closing at $11.32 against a most popular fair value of $11.00, the prevailing narrative sees only a slight premium in the price and focuses heavily on how future earnings quality and industry repair might reshape that gap.

Recent and proposed enforcement of tariffs on imported mattresses and components, combined with aggressive targeting of transshipment and non-compliant imports, is expected to create a more level playing field for domestic producers. This should drive higher demand for Leggett & Platt's U.S.-made bedding components and steel rod/wire, contributing to stronger revenue and gross margin expansion as price pressures from foreign dumping recede.

Want to see how modestly shrinking sales can still underpin a tight fair value band, rising margins, and a future earnings multiple below today’s industry benchmark? The narrative’s detailed roadmap connects these moving parts in a way the headline price alone does not reveal.

Result: Fair Value of $11 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer than expected residential bedding demand or prolonged competitive discounting could quickly erode the assumed margin recovery underpinning this fair value view.

Find out about the key risks to this Leggett & Platt narrative.

Another Angle On Value

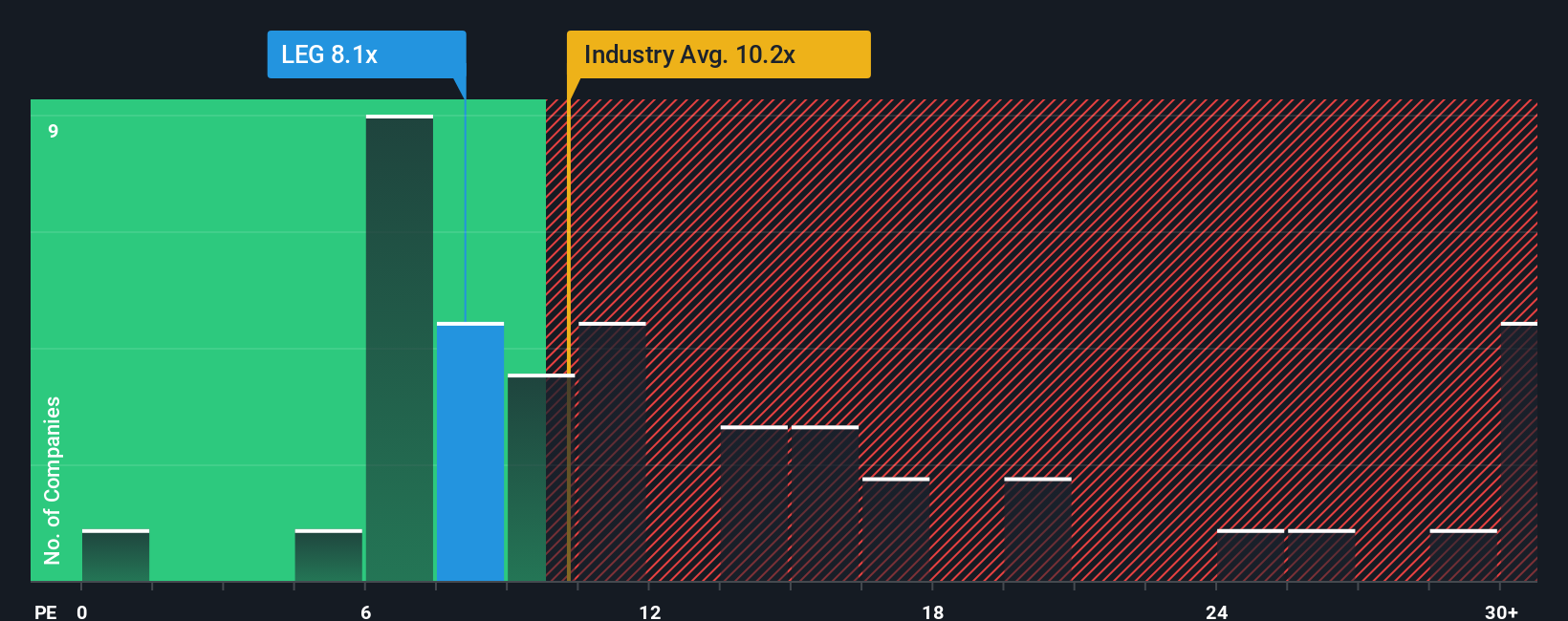

While the narrative work pegs Leggett & Platt as around 2.9% overvalued versus an $11 fair value, its 6.8x earnings multiple looks cheap against a 10.7x industry average, 14.1x peers, and a 12.3x fair ratio. This raises a tougher question: is this really pricing in all the risk?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Leggett & Platt Narrative

If the current storyline does not quite fit your view, dive into the numbers yourself and shape a fresh perspective in minutes, Do it your way.

A great starting point for your Leggett & Platt research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Ready For Your Next Investing Move?

Before you move on, lock in fresh ideas with our powerful screeners, so you are not relying on a single turnaround story to shape your returns.

- Capture potential bargains with strong cash generation by running through these 912 undervalued stocks based on cash flows and focusing on companies where the market has not yet caught up to the fundamentals.

- Ride structural growth in technology by scanning these 26 AI penny stocks for businesses building real revenue momentum from artificial intelligence, not just buzzword-heavy headlines.

- Strengthen your income stream by reviewing these 13 dividend stocks with yields > 3% and targeting businesses that balance attractive yields with sustainable payout ratios and resilient cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com