Is Kontoor Brands Now a Value Opportunity After 2025 Pullback and DCF Reassessment

- If you have been wondering whether Kontoor Brands is quietly turning into a value opportunity, you are not alone. This stock is starting to look interesting for valuation focused investors.

- Despite being down 6.2% over the last week, 8.1% over the past month, and 24.8% year to date, the stock is still up 80.7% over 3 years and 83.6% over 5 years, which indicates that long term holders have done well even after the recent pullback.

- Recently, sentiment around apparel and denim names has been shifting as investors sift through changing consumer demand and inventory trends across retailers. Sector wide moves and renewed focus on brands with durable cash flows have put companies like Kontoor back on the radar for investors looking for resilient dividend paying names.

- On our framework, Kontoor scores a strong 5/6 valuation check, suggesting it screens as undervalued on most of the key metrics tracked. Next, this can be broken down across different valuation methods, before circling back to a more holistic way of thinking about what the stock is really worth.

Find out why Kontoor Brands's -23.6% return over the last year is lagging behind its peers.

Approach 1: Kontoor Brands Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today, using a required rate of return.

For Kontoor Brands, the model starts with last twelve month Free Cash Flow of about $219.7 million, then uses analyst forecasts and gradual growth assumptions to project how this could develop. By 2027, free cash flow is expected to reach roughly $389.8 million, and Simply Wall St extrapolates this further to around $487.6 million by 2035, reflecting modest, steady growth in dollar terms.

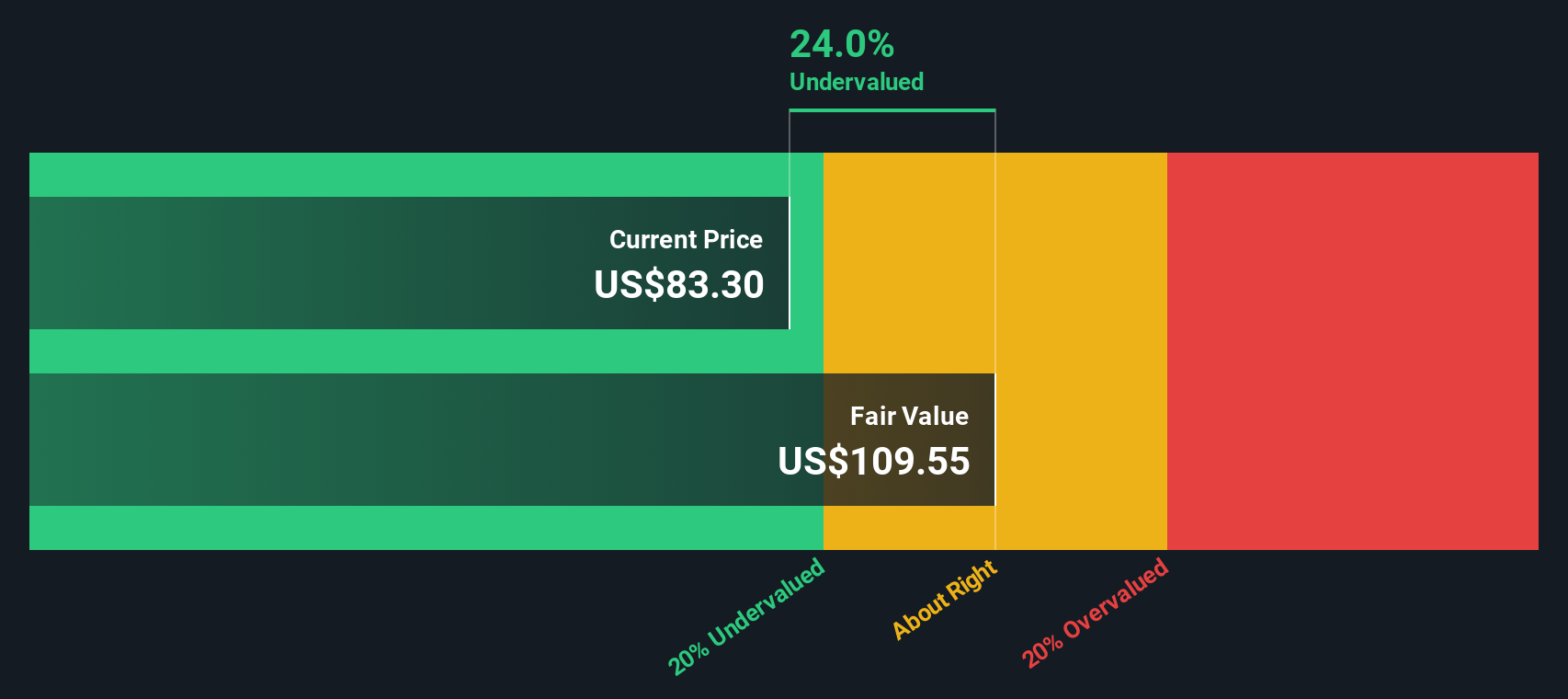

When all of these future cash flows are discounted back and summed, the DCF model estimates an intrinsic value of about $101.05 per share. Compared with the current market price, this implies the shares trade at roughly a 36.7% discount. This suggests investors are not fully pricing in Kontoor’s future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kontoor Brands is undervalued by 36.7%. Track this in your watchlist or portfolio, or discover 911 more undervalued stocks based on cash flows.

Approach 2: Kontoor Brands Price vs Earnings

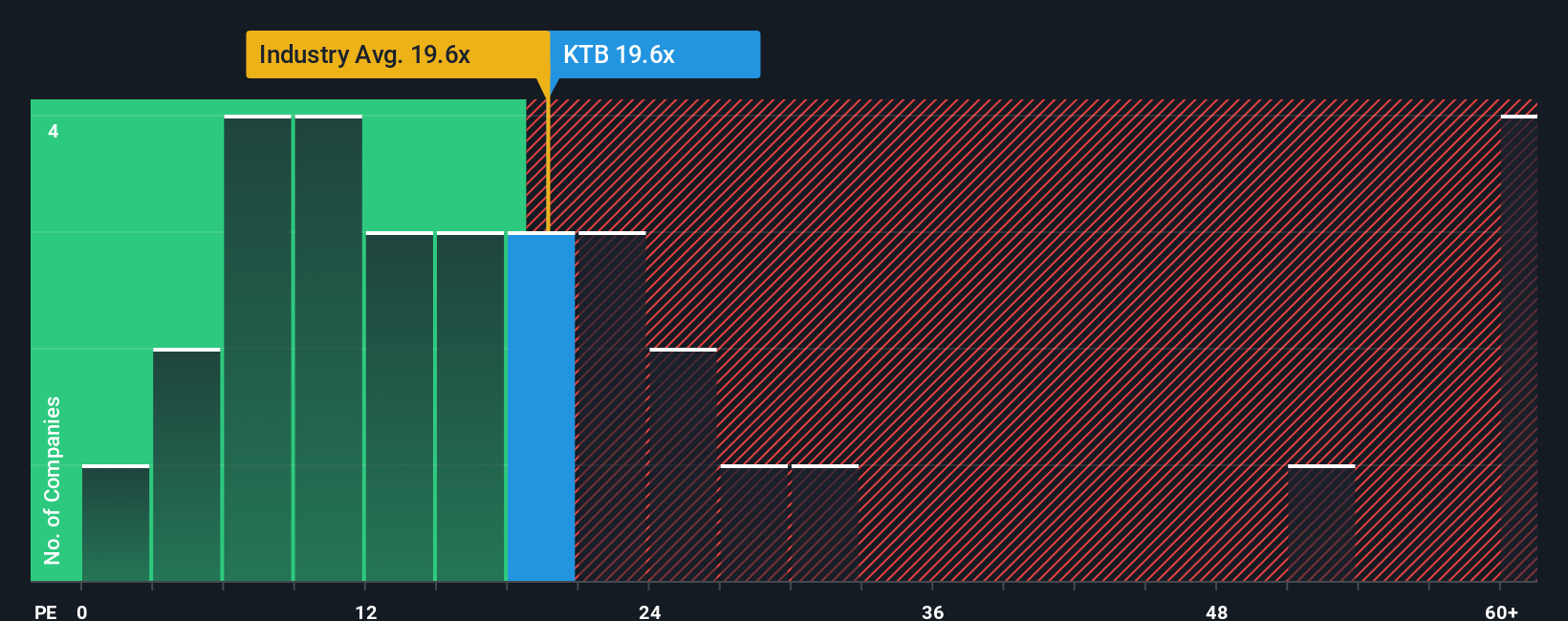

For profitable, established businesses like Kontoor Brands, the Price to Earnings (PE) ratio is a useful way to gauge whether investors are paying a reasonable price for each dollar of current earnings. In broad terms, companies with stronger growth prospects and lower risk typically deserve a higher PE ratio, while slower growing or riskier businesses should trade on a lower multiple.

Kontoor currently trades on a PE of around 16.3x, which is below both the Luxury industry average of about 22.6x and the broader peer group, which sits near 39.0x. To go a step further than these blunt comparisons, Simply Wall St calculates a proprietary Fair Ratio for each stock. This Fair Ratio, around 20.1x for Kontoor, reflects what investors might reasonably pay given its earnings growth profile, profitability, size, industry and risk characteristics, rather than just how it stacks up against peers.

Because this Fair Ratio is meaningfully above Kontoor’s current 16.3x multiple, this PE-based view suggests the shares are still trading at a discount to what they might be worth.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kontoor Brands Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, an easy tool on Simply Wall St’s Community page that lets you attach a clear story and set of assumptions to a company’s future revenue, earnings and margins. This way its story, financial forecast and fair value are all joined together and update dynamically as new earnings or news arrives. This can help you decide whether to buy or sell by comparing your Narrative Fair Value to today’s price. For example, a bullish Kontoor Brands investor might build a Narrative around Helly Hansen integration, double digit revenue growth and margin expansion that supports a fair value closer to $99 per share. A more cautious investor might emphasize legacy brand risk, cost pressures and slower digital progress, leading to a fair value nearer $49 per share. Both perspectives can sit side by side on the platform, giving you a simple, structured way to choose, tweak, and act on the story you believe.

Do you think there's more to the story for Kontoor Brands? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com