- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHas Pinnacle Financial Partners Price Jump Left Further Upside After Recent Regional Bank Rebound?

- Wondering if Pinnacle Financial Partners at around $100 a share is still a smart buy or if the easy money has already been made? Let us unpack what the current price might be telling you about its real value.

- The stock has crept up about 0.2% over the last week and jumped 18.6% in the past month, even though it is still down 11.8% year to date and 8.9% over the last year. Zooming out further, it is up 40.9% over three years and 62.1% over five, so there is clearly a longer term growth story in play.

- Recent headlines have focused on regional banks re rating as credit concerns ease and deposit trends prove more resilient than feared, which has helped sentiment toward quality names like Pinnacle. At the same time, investors are watching management's balance sheet discipline and capital allocation moves as key signals for whether this recovery has room to run.

- On our valuation checklist Pinnacle scores a solid 4 out of 6 for being undervalued, suggesting the market may not be fully pricing in its fundamentals yet. Next we will walk through the usual valuation tools investors rely on, then finish with a more nuanced way to judge whether PNFP is truly priced for its future, not its past.

Approach 1: Pinnacle Financial Partners Excess Returns Analysis

The Excess Returns model looks at how much profit Pinnacle Financial Partners can generate above the return that investors demand on its equity, and then capitalizes those surplus profits into an intrinsic value per share.

For Pinnacle, the foundation is its Book Value of $86.33 per share and a Stable EPS estimate of $10.67 per share, based on weighted future Return on Equity forecasts from 8 analysts. With an Average Return on Equity of 10.64% and a Cost of Equity of $8.22 per share, the stock is expected to generate Excess Returns of $2.46 per share, meaning its earnings are projected to exceed the required return on capital by a meaningful margin.

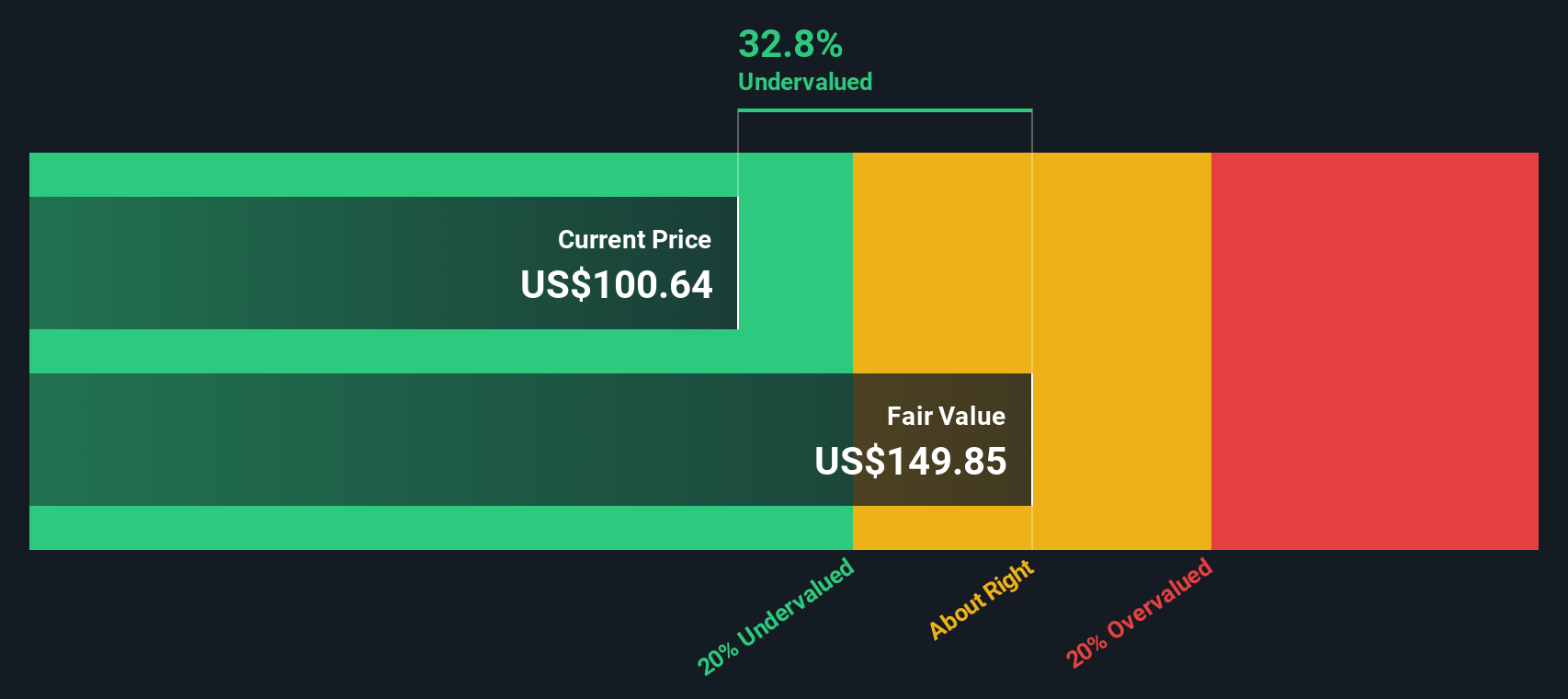

Analysts also expect the Stable Book Value to rise to $100.28 per share over time, supported by estimates from 10 analysts. Feeding these inputs into the Excess Returns framework yields an intrinsic value estimate of about $150 per share, implying the stock is roughly 33.3% undervalued compared with its current price around $100.

Result: UNDERVALUED

Our Excess Returns analysis suggests Pinnacle Financial Partners is undervalued by 33.3%. Track this in your watchlist or portfolio, or discover 912 more undervalued stocks based on cash flows.

Approach 2: Pinnacle Financial Partners Price vs Earnings

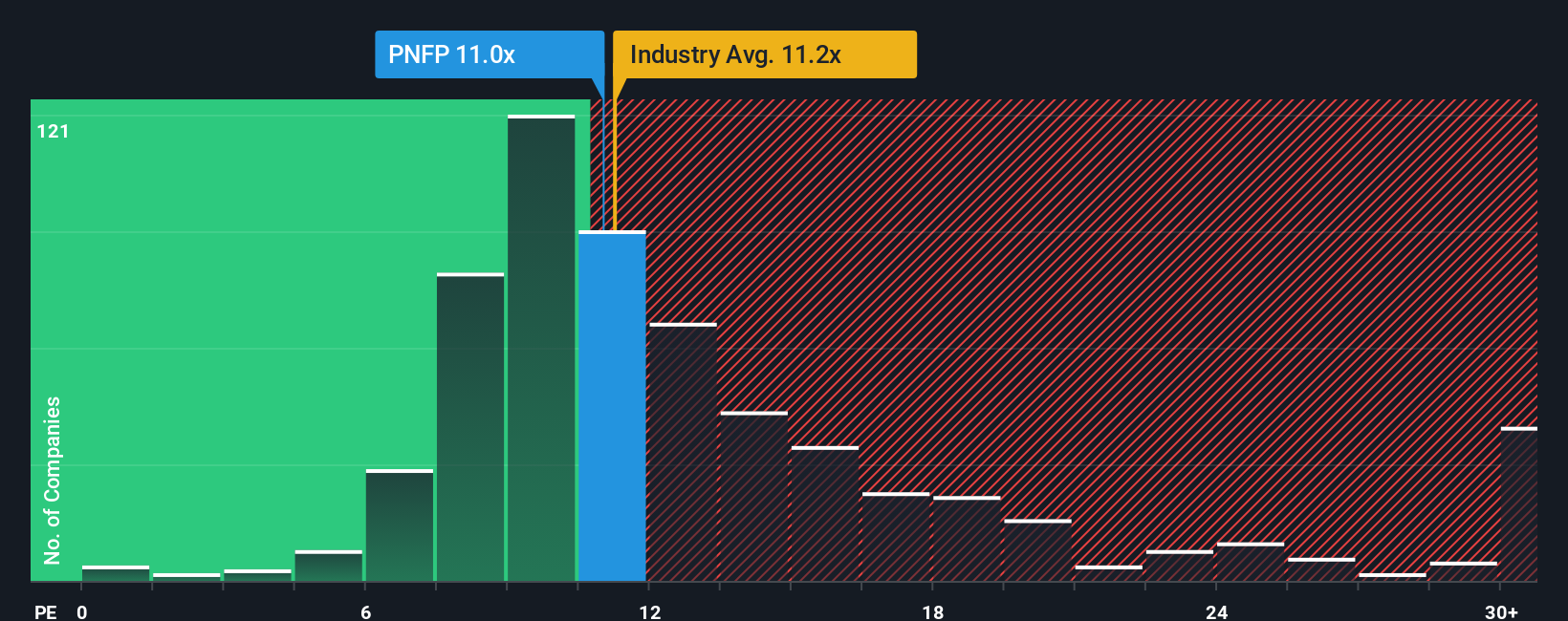

For consistently profitable companies like Pinnacle Financial Partners, the price to earnings ratio is a useful yardstick because it links what investors pay for the stock to the profits the business is actually generating today. In general, faster growing and lower risk banks tend to justify a higher PE, while slower growth or higher risk names deserve a discount multiple.

Pinnacle currently trades on a PE of about 12.7x. That is slightly above the broader Banks industry average of roughly 12.0x, but below the 14.1x average of its listed peers. Simply Wall St also calculates a proprietary Fair Ratio of 25.0x for Pinnacle, which estimates what a reasonable PE should be once factors like earnings growth, profitability, risk profile, industry dynamics and market cap are all taken into account.

This Fair Ratio is more tailored than a simple comparison with peers or the sector, because it adjusts for the fact that not all banks have the same growth runway or risk exposure. With Pinnacle trading at 12.7x versus a Fair Ratio of 25.0x, the stock screens as materially undervalued on a PE basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1462 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Pinnacle Financial Partners Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page where you connect your view of a company’s story to a set of numbers like future revenue, earnings, margins and a fair value. You can then compare that fair value to today’s price to decide whether to buy, hold or sell, with the whole picture updating automatically as new news or earnings arrive. For example, one Pinnacle Financial Partners Narrative might lean bullish and assume the merger delivers strong growth and synergies that justify a fair value closer to the top end of current targets, around $130 per share. A more cautious Narrative could focus on execution and credit risks, anchoring fair value nearer $95. Yet both investors are using the same tool to turn their story into a forecast and a price tag so they can act with more clarity and confidence.

Do you think there's more to the story for Pinnacle Financial Partners? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com