Has the CVS Stock Surge in 2025 Already Priced In Its Cash Flow Potential?

- If you are wondering whether CVS Health is still a bargain after its recent run, or if you have already missed the sweet spot, this breakdown will help you consider whether the current price makes sense.

- The stock has climbed about 77.0% year to date and 85.4% over the last year, even though 3 year returns are still slightly negative. This suggests the market has rapidly rewritten its expectations for CVS after a long stretch of underperformance.

- Recently, investors have been evaluating CVS Health's progress on its healthcare services strategy and the integration of past acquisitions. This is reshaping how the market views its long term earnings power. At the same time, ongoing debates around drug pricing reforms and reimbursement pressures continue to influence sentiment, adding both opportunity and uncertainty for the stock.

- In that context, CVS Health currently earns a valuation score of 6/6 on our checks, indicating it screens as undervalued across the board. Next, we will walk through how different valuation approaches arrive at that view, followed by a more intuitive way to think about what the stock might be worth.

Approach 1: CVS Health Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to the present.

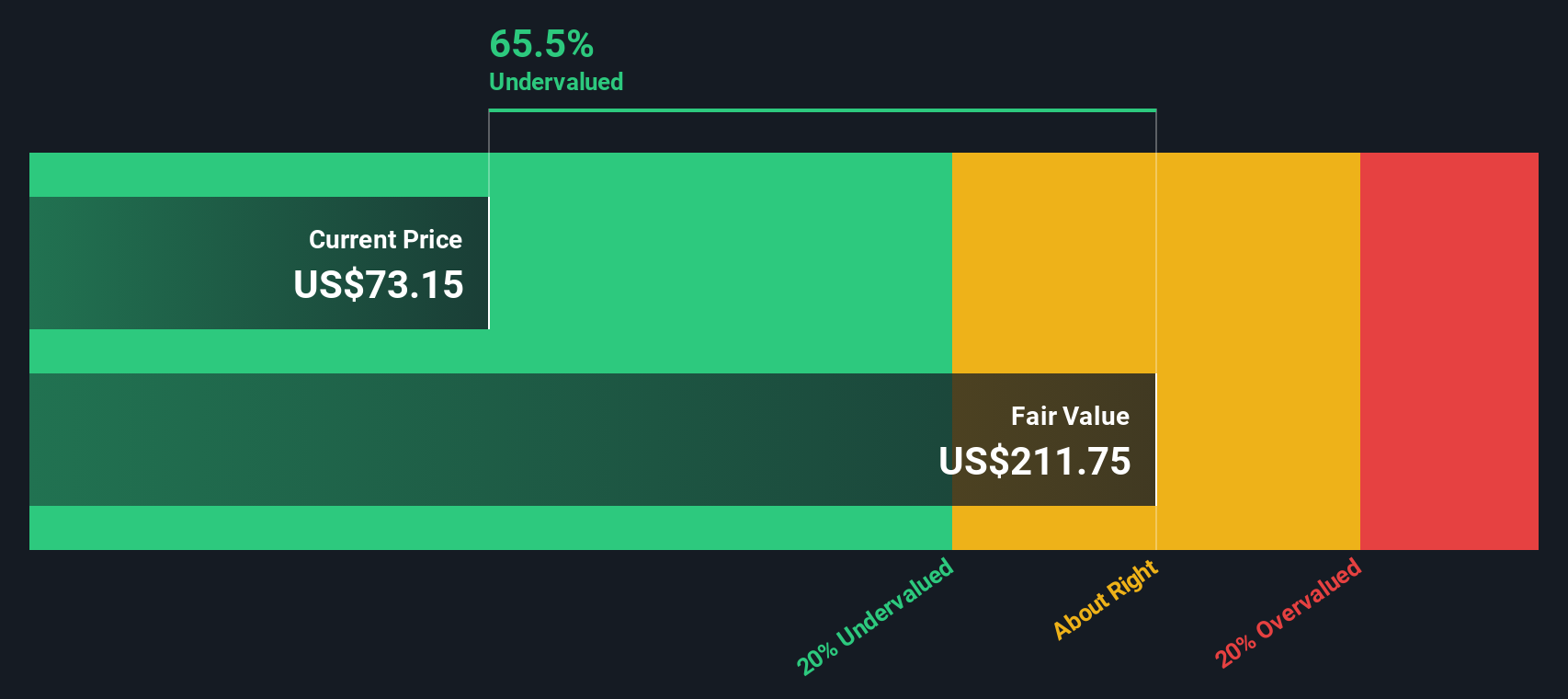

For CVS Health, the model starts with last twelve months Free Cash Flow of about $6.1 Billion and uses analyst forecasts plus Simply Wall St extrapolations to project growth. By 2029, annual Free Cash Flow is expected to reach roughly $11.1 Billion, with projections extending out over the following years as cash flows continue to rise, though at a moderating pace.

Those future cash flows are discounted to today using a 2 Stage Free Cash Flow to Equity approach, producing an estimated intrinsic value of about $225.24 per share. Compared with the current share price, this implies the stock trades at roughly a 65.2% discount to its DCF value. This suggests the market is pricing CVS Health well below its modeled cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CVS Health is undervalued by 65.2%. Track this in your watchlist or portfolio, or discover 915 more undervalued stocks based on cash flows.

Approach 2: CVS Health Price vs Sales

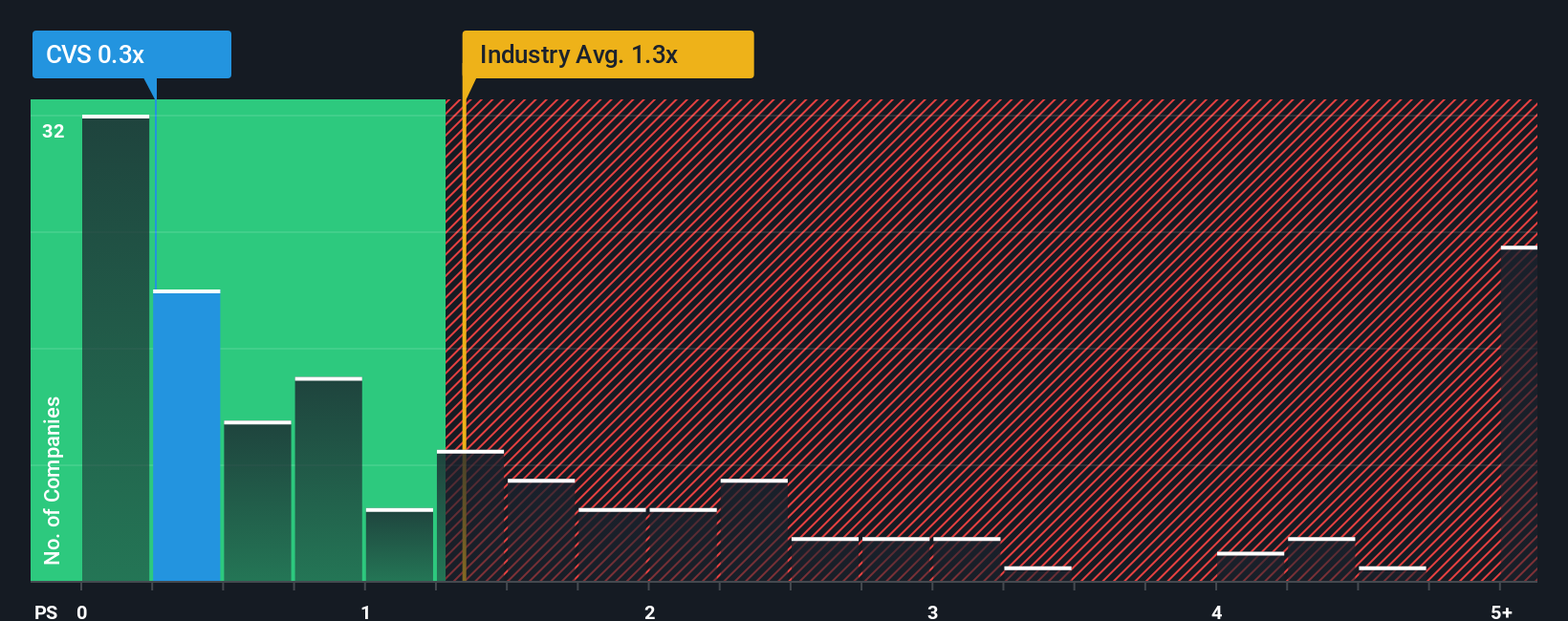

For large, established healthcare companies like CVS Health, the price to sales, or P/S, multiple is a useful way to compare what investors are paying for each dollar of revenue, especially when margins and earnings can be affected by one time items or accounting noise.

In general, higher growth and lower perceived risk justify a higher “normal” P/S multiple, while slower growth or elevated risk typically warrant a lower one. CVS Health currently trades on a P/S multiple of about 0.25x, which is far below the Healthcare industry average of roughly 1.34x and also well under the peer group average of around 4.48x.

Simply Wall St’s Fair Ratio framework estimates what P/S multiple would be reasonable for CVS Health, given its growth outlook, profit margins, industry positioning, market cap and risk profile. This produces a Fair Ratio of about 1.25x, which is more tailored than a simple comparison to peers or the broad industry because it adjusts for company specific fundamentals rather than assuming they are all alike. With the shares trading at roughly 0.25x against a Fair Ratio near 1.25x, the stock screens as materially undervalued on a sales based lens.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1460 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CVS Health Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of CVS Health’s story with a clear set of forecasts for its future revenue, earnings and margins, and then translate that into a Fair Value you can compare to today’s share price to help inform your decision.

On Simply Wall St’s Community page, Narratives are easy to use and continuously updated as news and earnings arrive, so the story, the numbers and the Fair Value all move together in real time.

For example, one investor might build a bullish CVS Health Narrative around Medicare Advantage margin recovery, value based care and digital integration that supports a Fair Value near $99 per share. Another might take a more cautious view focused on reimbursement pressure and regulatory risk that leads to a Fair Value closer to $70. Narratives help you see exactly how those different assumptions drive different valuations so you can decide which story you find more appropriate for your own view.

Do you think there's more to the story for CVS Health? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com