Evaluating Jardine Matheson (SGX:J36) After Insider Buying, Buybacks and the Planned Mandarin Oriental Privatization

Jardine Matheson Holdings (SGX:J36) has drawn fresh attention after insiders stepped up share purchases alongside a US$250 million buyback program, with the planned privatization of Mandarin Oriental in early 2026 sharpening the strategic narrative.

See our latest analysis for Jardine Matheson Holdings.

Those insider moves are landing against a powerful backdrop, with Jardine Matheson’s share price returning 14.04% over 90 days and a standout 63.20% year to date, while the 1 year total shareholder return of 72.76% points to firmly building momentum rather than a short lived bounce.

If this combination of buybacks, insider buying, and long term compounding has you thinking bigger, it might be worth exploring fast growing stocks with high insider ownership as you look for the next wave of opportunity.

With earnings rebounding, insiders buying, and the share price already close to analyst targets, the key question now is whether Jardine Matheson still trades below its true value or if markets are already pricing in future growth.

Most Popular Narrative: 5.6% Undervalued

With Jardine Matheson trading at $68.07 against a narrative fair value of $72.10, the market is seen lagging a measured upgrade in expectations.

The group's strong balance sheet, ongoing deleveraging, and over $12 billion in liquidity create capacity to execute new investments and bolt on M&A, particularly in digitalization, smart mobility, and technology driven businesses. This is expected to enable future top line and EBITDA growth and support a re rating as market confidence builds.

Want to see what backs this optimism? Steadily rising revenues, expanding margins, and a sharply different future earnings base are doing the heavy lifting. Curious?

Result: Fair Value of $72.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent weakness in Greater China property and structural headwinds in Astra’s autos and coal businesses could quickly undermine these upbeat expectations.

Find out about the key risks to this Jardine Matheson Holdings narrative.

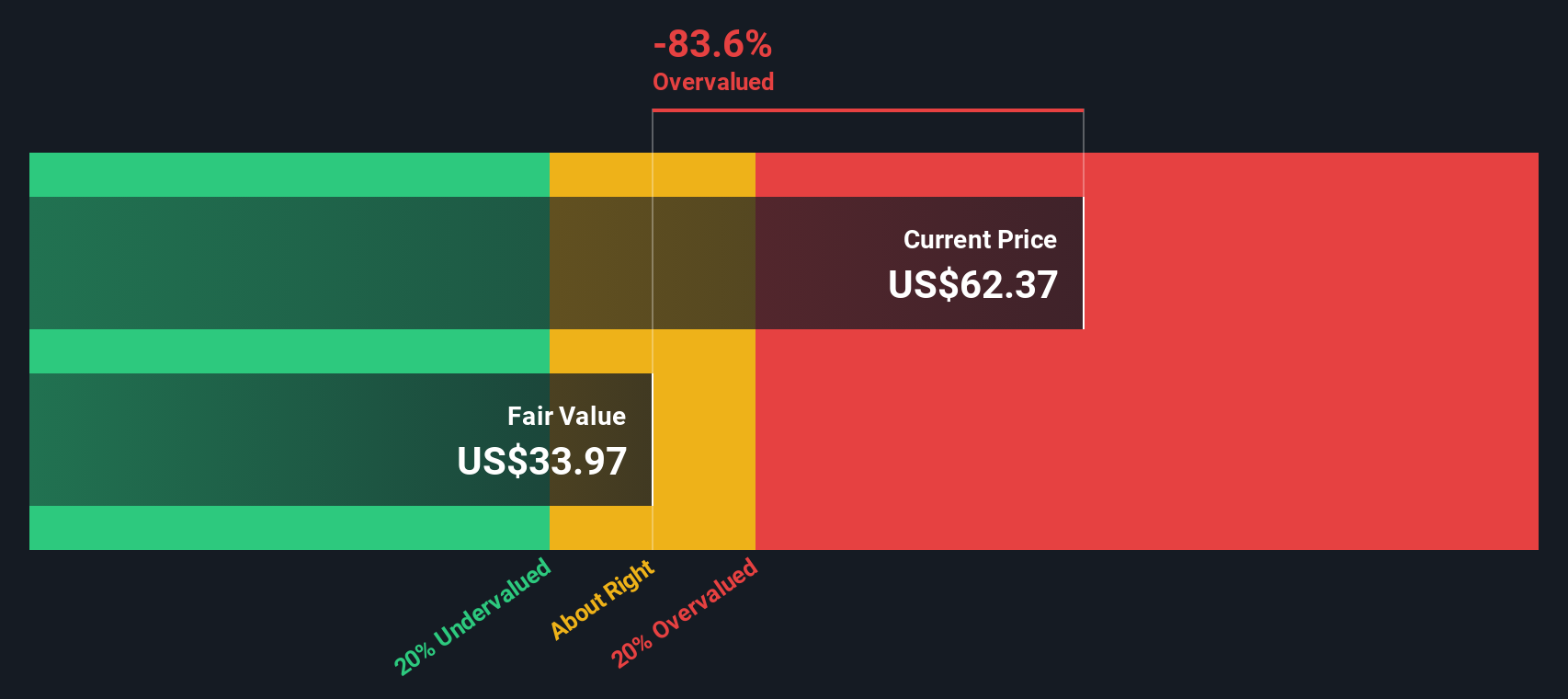

Another Lens on Value

Our SWS DCF model paints a starkly different picture, suggesting fair value near $34.63, which would make Jardine Matheson look meaningfully overvalued at current prices rather than modestly undervalued. This raises the question of whether recent buybacks and narratives are leaning too much on sentiment over cash flow reality.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Jardine Matheson Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 911 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Jardine Matheson Holdings Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in minutes: Do it your way.

A great starting point for your Jardine Matheson Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop at Jardine Matheson when the next potential winners are only a screener away. Smart capital moves before the crowd catches on.

- Capture mispriced potential with these 911 undervalued stocks based on cash flows that spotlight companies whose cash flows suggest the market has not yet caught up.

- Ride powerful secular trends by targeting these 25 AI penny stocks that could reshape entire industries through automation and intelligent software.

- Lock in attractive income streams with these 13 dividend stocks with yields > 3% that focus on businesses paying robust yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com