- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Humana Attractively Priced After Recent 16% Surge And DCF Upside In 2025

Setting the Stage for Humana's Valuation Deep Dive

Humana has been catching the eye of investors who are wondering if the recent momentum is finally signaling value, or if the market is just resetting expectations after a tough few years.

Over the last month the stock has climbed 15.9%, including a 7.2% gain in just the past week, and it is now up 8.7% year to date and 7.0% over the last year, even after a bruising 3 year return of -43.9% and a 5 year return of -26.2%.

Recent headlines have focused on shifting dynamics in the US healthcare and Medicare Advantage markets, including regulatory scrutiny and changing reimbursement structures that have pushed investors to reassess risk and growth in managed care stocks. At the same time, strategic moves across the sector, such as cost management initiatives and portfolio adjustments by large insurers, have added more nuance to how the market is pricing Humana’s long term role in the healthcare ecosystem.

On our valuation framework, Humana scores 3 out of 6 for being undervalued. This means it looks cheap on some metrics but not all. That mixed picture is exactly why we will walk through multiple valuation lenses in this article before finishing with a more holistic way to think about what the stock is really worth.

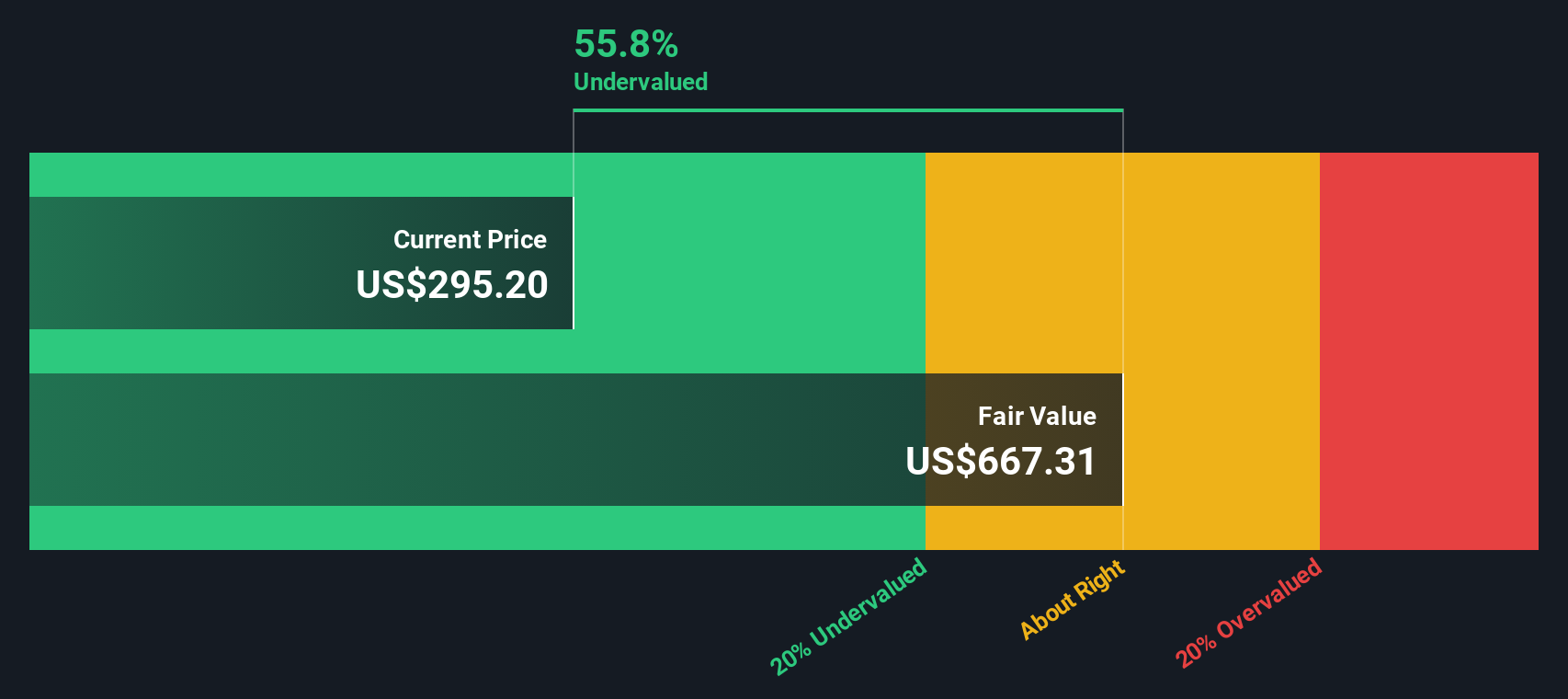

Approach 1: Humana Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today’s dollars.

For Humana, the latest twelve month free cash flow is about $1.24 Billion. Analysts expect free cash flow to rise sharply over the next few years, reaching roughly $3.74 Billion by 2029, with further growth extrapolated out to 2035 under a 2 stage Free Cash Flow to Equity framework. These projections move from analyst forecasts in the near term to more modest, model driven growth further out. They are all converted into today’s value using a required return that reflects risk and inflation.

On this basis, the model arrives at an intrinsic value of about $662.49 per share. Compared with the current share price, this implies Humana is about 58.5% undervalued, suggesting the market is heavily discounting its long term cash generation potential.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Humana is undervalued by 58.5%. Track this in your watchlist or portfolio, or discover 913 more undervalued stocks based on cash flows.

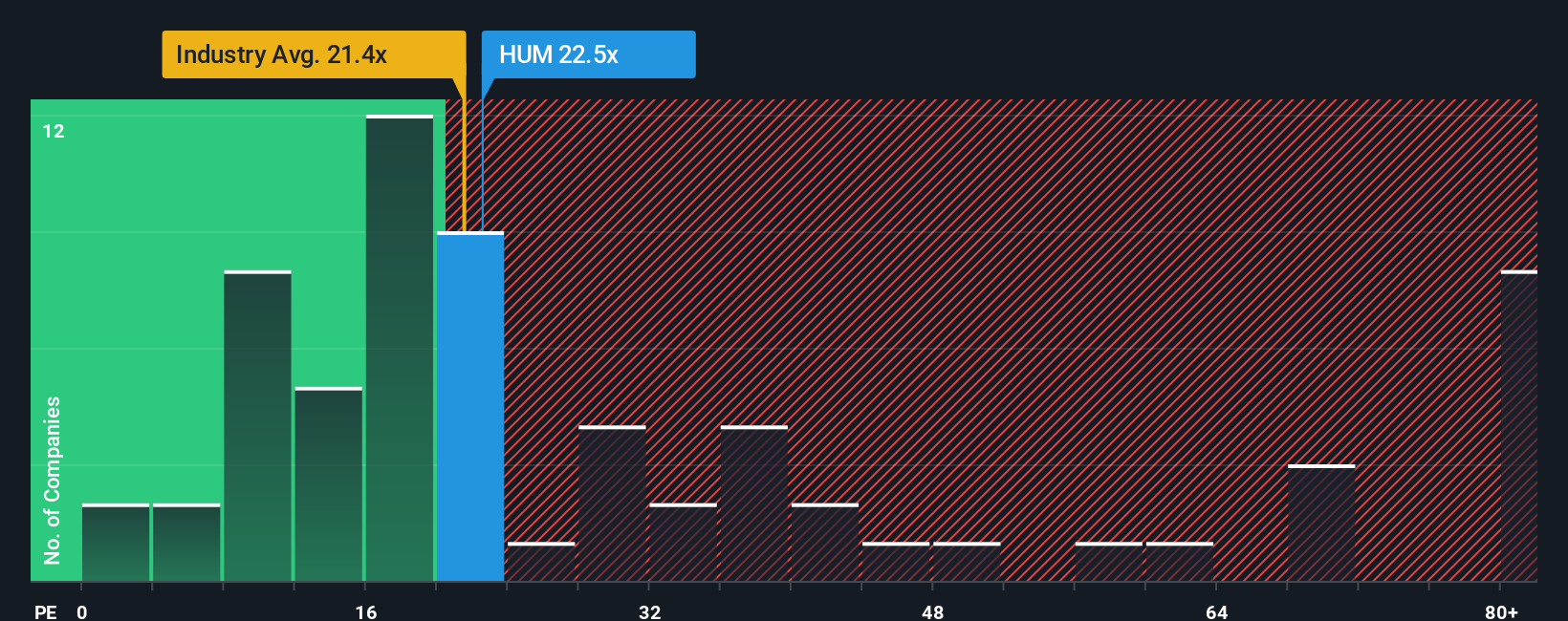

Approach 2: Humana Price vs Earnings

For a profitable company like Humana, the price to earnings ratio is a useful yardstick because it ties the share price directly to the profits that ultimately support returns for shareholders. A higher or lower PE can be reasonable depending on how quickly earnings are expected to grow and how much risk investors see in those future profits, so what counts as a fair PE is shaped by both growth and uncertainty.

Humana currently trades on a PE of about 25.6x, which is above both the US Healthcare industry average of roughly 23.9x and the peer group average of around 21.1x. Simply Wall St goes a step further with its Fair Ratio, which estimates what Humana’s PE should be, given its earnings growth outlook, profitability, industry positioning, market cap and risk profile. This makes it more tailored than a simple comparison with peers or sector averages, which can miss important differences in quality and risk.

Humana’s Fair Ratio is 40.9x, materially higher than its current 25.6x multiple, indicating that the stock looks undervalued on this earnings based lens.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1455 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Humana Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you tell the story behind your numbers by linking your view of Humana’s future revenue, earnings and margins to a financial forecast, a fair value, and a clear buy or sell signal based on how that fair value compares with today’s price. All of this then updates dynamically as new news or earnings arrive. For example, one investor might build a bullish Humana Narrative that leans into AI driven efficiency, CenterWell expansion and margin recovery to support a fair value closer to the most optimistic analyst target of about $353. A more cautious investor could emphasize regulatory risk, Medicare Advantage cyclicality and slower Medicaid recovery to justify a fair value nearer the most conservative target of around $250, with both perspectives coexisting on the platform and helping each investor act with more conviction and discipline.

Do you think there's more to the story for Humana? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com