- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalOrla Mining (TSX:OLA) Valuation Check After South Carlin Exploration Results and Growth Update

Orla Mining (TSX:OLA) just followed up strong South Carlin exploration news with a separate catalyst: Fairfax exiting a 7.35% stake in a CAD 440 million block trade to an undisclosed buyer.

See our latest analysis for Orla Mining.

Those South Carlin drill results, the inaugural dividend, and now Fairfax’s exit have landed on top of a powerful backdrop, with a year to date share price return of 116.57% and a one year total shareholder return of 134.18%. This suggests momentum is clearly building rather than fading at the current CA$18.43 share price.

If this kind of rerating has you thinking more broadly about the gold space, it could be worth lining Orla up against other fast growing stocks with high insider ownership to see where the next leg of momentum might come from.

With the share price already more than doubling this year, but still trading around a 30% discount to analyst targets, investors now face a pivotal question: Is Orla still mispriced, or is the market already baking in South Carlin’s future growth?

Most Popular Narrative: 22.9% Undervalued

At a last close of CA$18.43 versus a narrative fair value near CA$23.91, Orla is framed as offering sizable upside if growth plays out.

Robust production growth and revenue diversification from integrating Musselwhite, as well as future contributions from South Railroad and expanded Camino Rojo underground, are likely underappreciated catalysts that will increase long term revenue and reduce operational risk.

Curious how this story gets from today’s modest margins to a future of powerful cash generation, steep earnings growth, and a compressed profit multiple? The full narrative unpacks the specific growth path, margin lift, and valuation reset needed to support that higher fair value.

Result: Fair Value of $23.91 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside still hinges on smooth execution, with permitting delays or higher than expected costs at Camino Rojo or South Railroad capable of derailing projections.

Find out about the key risks to this Orla Mining narrative.

Another Lens On Value

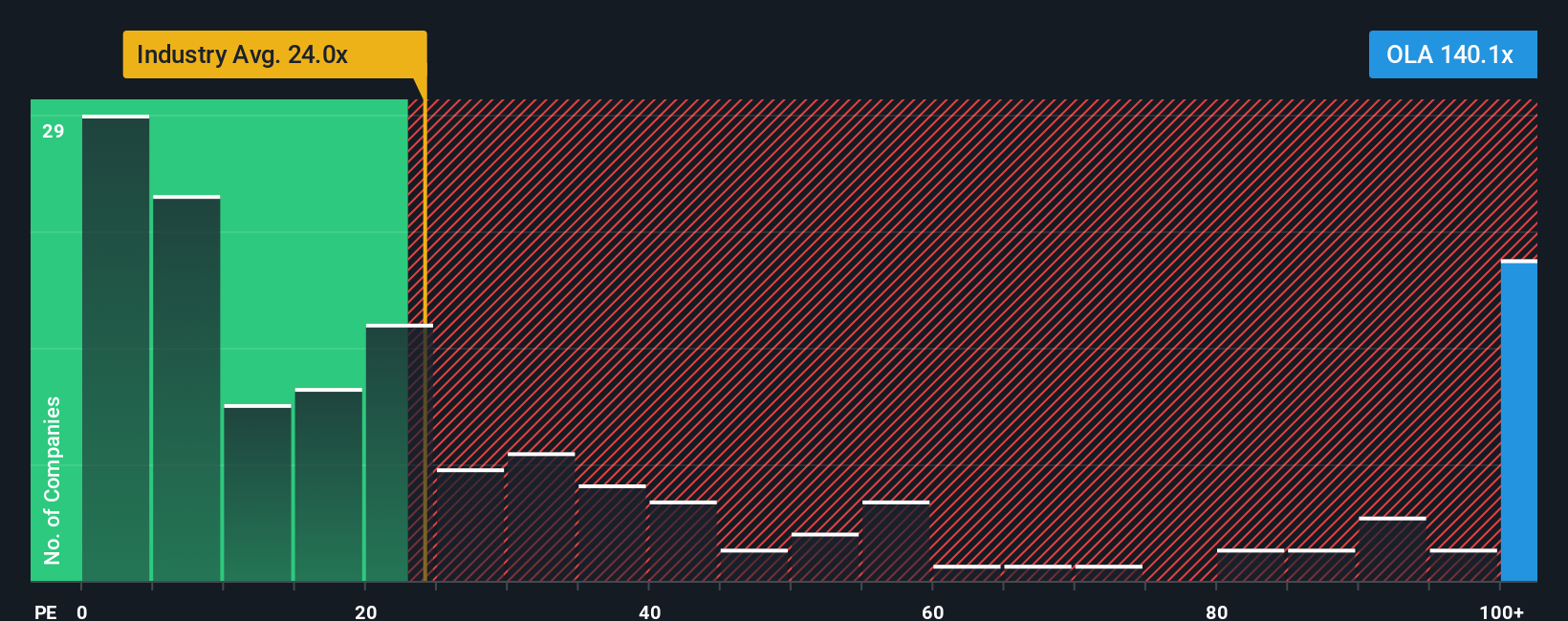

On earnings, the story looks very different. Orla trades on a rich 84.6 times earnings, versus about 21.4 times for the Canadian metals and mining group and a fair ratio near 24.8 times. That kind of gap can unwind quickly if growth expectations slip, so how much optimism feels comfortable to you?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Orla Mining Narrative

If the current framing does not quite align with your own perspective, dive into the numbers and build a tailored view in minutes: Do it your way.

A great starting point for your Orla Mining research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, give yourself an edge by scanning fresh opportunities through powerful screeners on Simply Wall St, so you are not late to the next move.

- Capitalize on mispriced potential by targeting companies trading below their intrinsic value through these 906 undervalued stocks based on cash flows and position yourself ahead of a sentiment shift.

- Ride structural tailwinds in cutting edge innovation by focusing on these 26 AI penny stocks that could benefit as artificial intelligence reshapes entire industries.

- Seek more dependable portfolio income by zeroing in on these 13 dividend stocks with yields > 3% that may offer resilient yields even when markets stay volatile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com