- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs EnerSys Stock Still Attractive After a 60% Surge in 2025?

- Wondering if EnerSys is still a smart buy after its big run, or if you would just be chasing momentum at this point? Let us walk through what the numbers actually say about its value.

- EnerSys has climbed to around $147.65, delivering 0.4% over the last week, 7.4% over the last month, and a hefty 60.3% year to date, with a 60.7% gain over the past year and 109.8% over three years, which hints that the market is steadily re-rating the stock.

- That surge has come as investors lean into energy storage and power solutions names, with EnerSys regularly popping up in discussions around grid resilience, industrial electrification, and backup power infrastructure. The market seems to be pricing in a bigger role for the company in mission critical battery systems as demand for reliable energy infrastructure keeps building.

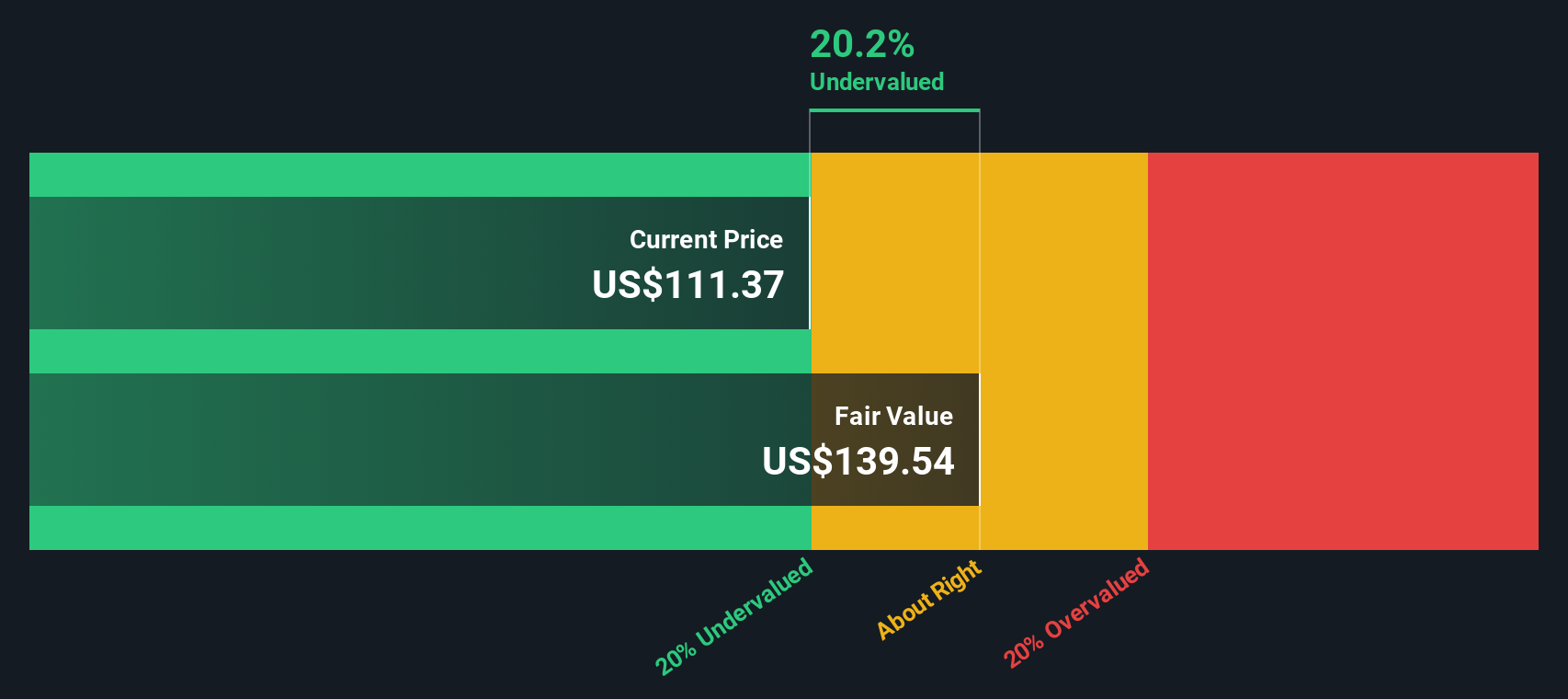

- Despite that strong performance, EnerSys only scores a 3/6 valuation check score, suggesting it screens as undervalued on some measures but not others. That is where things get interesting. Next we will unpack those different valuation approaches in detail, then circle back at the end to a more holistic way of thinking about what EnerSys might really be worth.

Approach 1: EnerSys Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to today in dollar terms.

EnerSys currently generates about $329.7 million in free cash flow. The 2 Stage Free Cash Flow to Equity model projects this will gradually trend down to roughly $140.8 million by 2035, based on a mix of analyst estimates for the next few years and longer term extrapolations by Simply Wall St. Each future yearly cash flow is discounted back to its present value, then added together to arrive at an intrinsic value per share.

Under this framework, the DCF model arrives at an estimated fair value of about $58.45 per share. This implies the stock is roughly 152.6% overvalued compared with the current market price around $147.65. On this cash flow view alone, EnerSys looks richly priced rather than cheap.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests EnerSys may be overvalued by 152.6%. Discover 906 undervalued stocks or create your own screener to find better value opportunities.

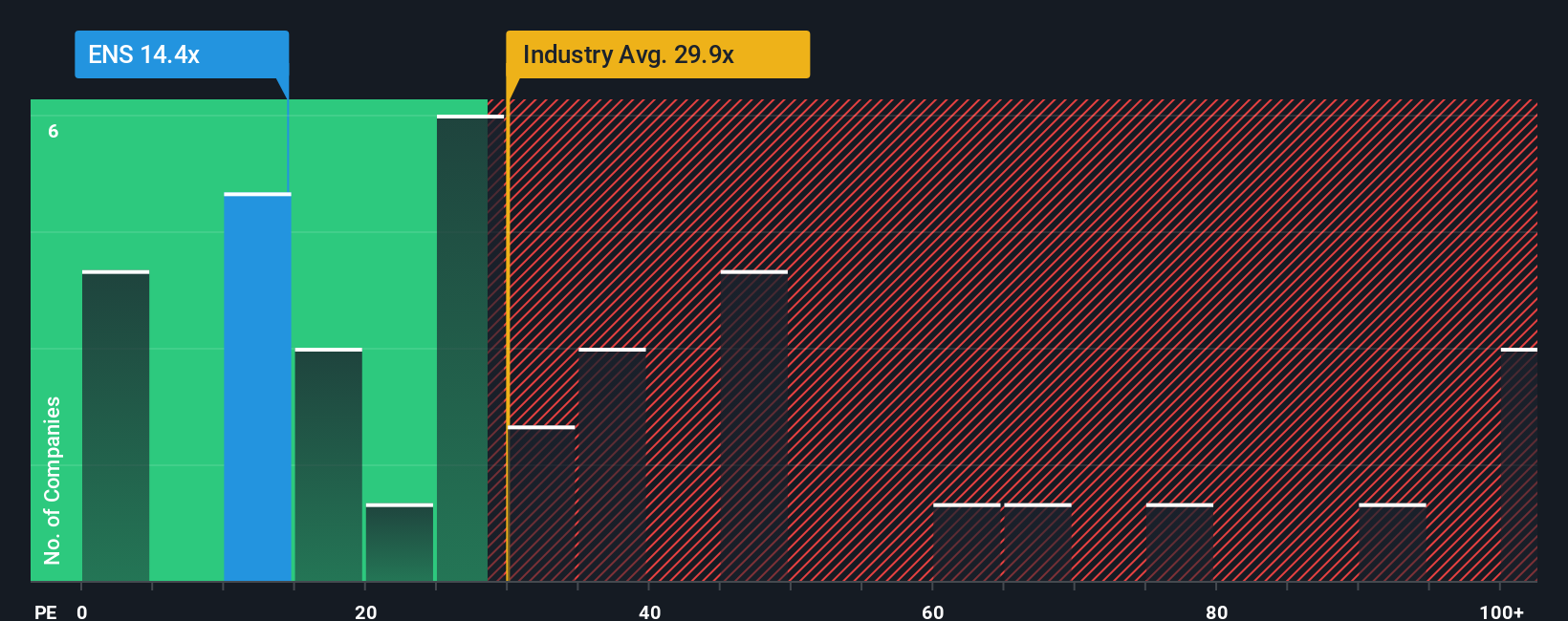

Approach 2: EnerSys Price vs Earnings

For consistently profitable companies like EnerSys, the price to earnings, or PE, ratio is a useful way to gauge value because it links what investors pay directly to the profits the business is generating today. In general, faster growth and lower perceived risk justify a higher PE, while slower, more volatile, or cyclical earnings usually command a lower one.

EnerSys currently trades on a PE of around 16.16x. That is well below the broader Electrical industry average of about 31.85x and also sits at a steep discount to its peer group, which averages roughly 36.88x. On those basic comparisons alone, EnerSys looks inexpensive relative to other listed battery and power equipment names.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what a more tailored PE should be, given EnerSys’s specific earnings growth outlook, profitability, industry, market cap and risk profile. For EnerSys, that Fair Ratio is 24.60x, which is meaningfully higher than the current 16.16x. That gap suggests the market is not fully recognising the company’s fundamentals, pointing to undervaluation on an earnings multiple basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your EnerSys Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. This is a simple framework on Simply Wall St’s Community page that lets you attach your own story about a company to the numbers by linking how you think its business will evolve through a structured forecast for revenue, earnings and margins. This ultimately leads to a fair value estimate that you can compare directly to today’s share price to decide whether EnerSys looks like a buy, hold or sell. The platform continuously updates those Narratives as new earnings, news or guidance arrive and allows very different perspectives to coexist. For example, one investor might plug in robust data center and electrification driven growth and arrive at a fair value well above the current analyst target of about $144 per share. A more cautious investor who is worried about trade policy, acquisition risks and slower organic growth might assume lower margins and a smaller multiple, ending up with a fair value far below today’s price. Yet both investors can see clearly how their beliefs translate into numbers and what would need to change for their view to shift.

Do you think there's more to the story for EnerSys? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com