- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs It Too Late To Consider Liquidia After Its 182.6% 2025 Surge?

- If you are wondering whether Liquidia is still a smart buy after its huge run, you are not alone. This is exactly the kind of stock where valuation really matters.

- The share price has pulled back about 2.3% over the last week, but it is still up 21.9% over 30 days and 182.6% year to date, with a 210.0% gain over the past year and 992.3% over five years.

- Those moves have been driven by growing optimism around Liquidia's pipeline and regulatory progress, with investors reacting positively to developments that reduce perceived risk around its lead therapies. At the same time, shifts in sentiment across the biotech space have amplified every piece of company specific news, making the stock more volatile than the broader market.

- Despite all that excitement, Liquidia scores just 2 out of 6 on our valuation checks. Next, we will break down what different valuation methods say about the stock, and then finish with a more complete way to judge whether the current price really makes sense.

Liquidia scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Liquidia Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and discounting them back to today, so investors can compare that value to the current share price.

For Liquidia, the 2 Stage Free Cash Flow to Equity model starts from last twelve months Free Cash Flow of roughly $116 million in the red, reflecting its investment heavy, pre profit profile. Analyst forecasts and Simply Wall St extrapolations then ramp Free Cash Flow up to about $942 million by 2035, with particularly rapid growth expected through the late 2020s as key therapies potentially gain traction.

When all those projected cash flows are discounted back to today, the model produces an estimated intrinsic value of about $196.66 per share. Compared with the current share price, this implies the stock is roughly 82.6% undervalued. This suggests the market is still pricing in a lot more risk than the cash flow outlook alone would indicate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Liquidia is undervalued by 82.6%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Liquidia Price vs Sales

For companies that are still unprofitable or reinvesting heavily, the price to sales ratio is often a straightforward way to gauge valuation because it focuses on how much investors are paying for each dollar of current revenue, rather than uncertain future earnings. In general, faster growth and lower perceived risk can justify a higher normal multiple, while slower growth or higher risk usually means a lower one is appropriate.

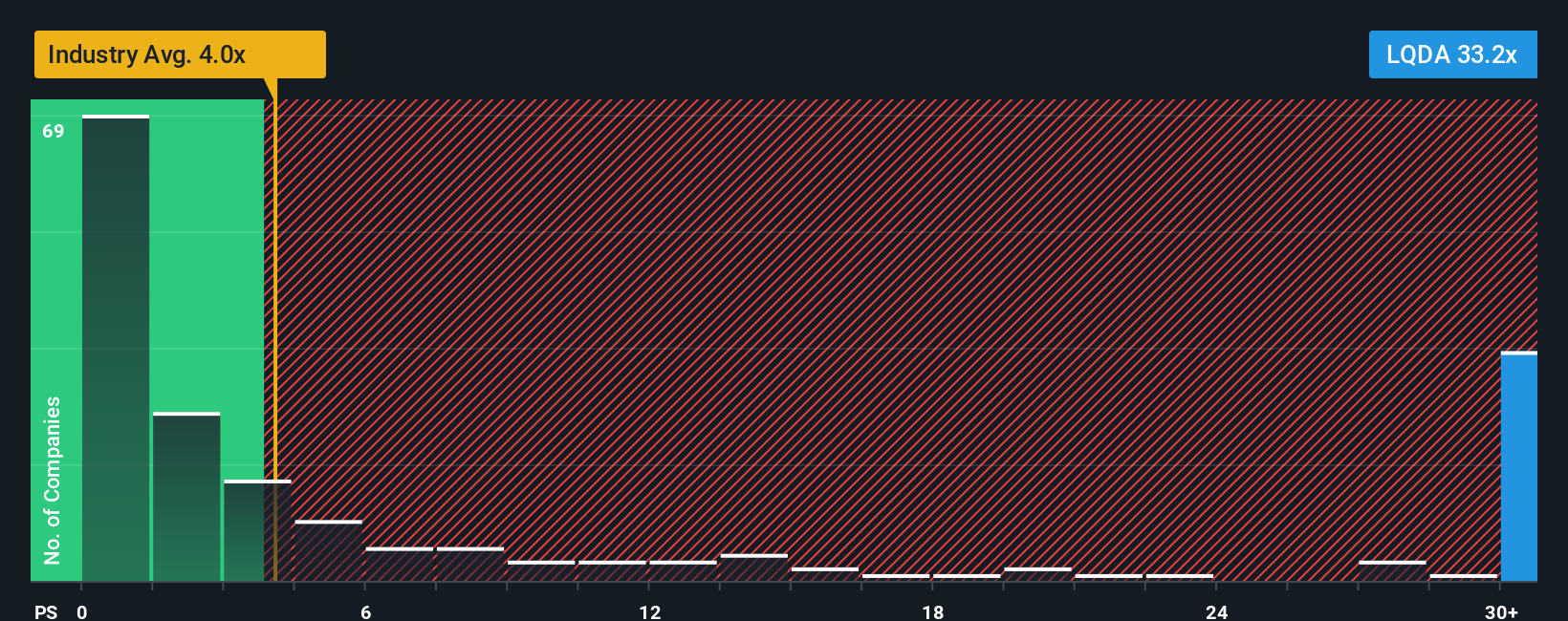

Liquidia currently trades at about 43.0x sales, far above the broader Pharmaceuticals industry average of roughly 4.2x and well ahead of its peer group, which sits near 9.3x. On the surface, that kind of premium suggests a lot of future success is already priced in. To refine this view, Simply Wall St uses a proprietary Fair Ratio, which estimates what a justified price to sales multiple should be after factoring in earnings growth potential, industry dynamics, profit margins, company size and risk profile.

For Liquidia, the Fair Ratio comes out at around 16.1x sales, a level that is tailored to the company, unlike simple peer or industry comparisons. With the current multiple of 43.0x sitting far above that Fair Ratio, the stock appears meaningfully overvalued on this metric.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Liquidia Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of a company’s future with the numbers behind it. A Narrative is your story about Liquidia, captured as assumptions for fair value, future revenue growth, margins and risk, so you can see how the story translates into a concrete forecast and a single fair value estimate. On Simply Wall St, millions of investors build and explore Narratives on the Community page, using them as an easy tool to decide whether to buy or sell by comparing their Fair Value to the current share price. Because Narratives update automatically as new information, like news or earnings results, flows in, your story and valuation stay current without any number crunching. For Liquidia, one investor’s Narrative might price in rapid adoption of its lead therapy and strong margins, while another assumes slower uptake and continued cash burn, leading to very different fair values and, in turn, very different decisions about whether the stock is attractive at today’s price.

Do you think there's more to the story for Liquidia? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com