- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Hesai Group (NasdaqGS:HSAI) Valuation After Morgan Stanley Recognition and Lidar Milestone Momentum

Hesai Group (NasdaqGS:HSAI) just earned a spotlight as the only lidar player on Morgan Stanley's Humanoid Tech 25 list, after crossing 2 million automotive lidar shipments and leading ADAS main lidar share for nine straight months.

See our latest analysis for Hesai Group.

Those milestones seem to be resonating with investors, with the share price now at $20.88 and a year to date share price return of 29.45%. The 1 year total shareholder return of 104.71% suggests momentum is building again, despite a weaker 90 day share price return of 29.93%.

If this kind of lidar driven story has your attention, it could be worth scanning other high growth tech names through high growth tech and AI stocks for fresh ideas.

With Hesai still trading at a sizable discount to analyst targets despite rapid revenue and profit growth, investors face a key question: Is the market underestimating its lidar edge or already pricing in its next leg of expansion?

Most Popular Narrative: 30% Undervalued

With Hesai's fair value estimate sitting well above the recent $20.88 close, the most popular narrative argues that current prices miss the long term earnings runway.

The projection of 2025 LiDAR shipments reaching 1.2 million to 1.5 million units, with nearly 200,000 high margin robotic LiDAR units, is expected to significantly boost revenue. Anticipated net revenues of RMB 3 billion to RMB 3.5 billion for 2025, driven by strong demand and mass market adoption, indicate potential growth in revenue.

To see how those shipment volumes translate into a richer earnings profile and why a premium future multiple may still make sense, explore the full narrative.

Result: Fair Value of $29.83 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained overseas expansion delays, as well as margin pressure from aggressive pricing and rising input costs, could quickly challenge the long term lidar growth narrative.

Find out about the key risks to this Hesai Group narrative.

Another View: Rich On Earnings

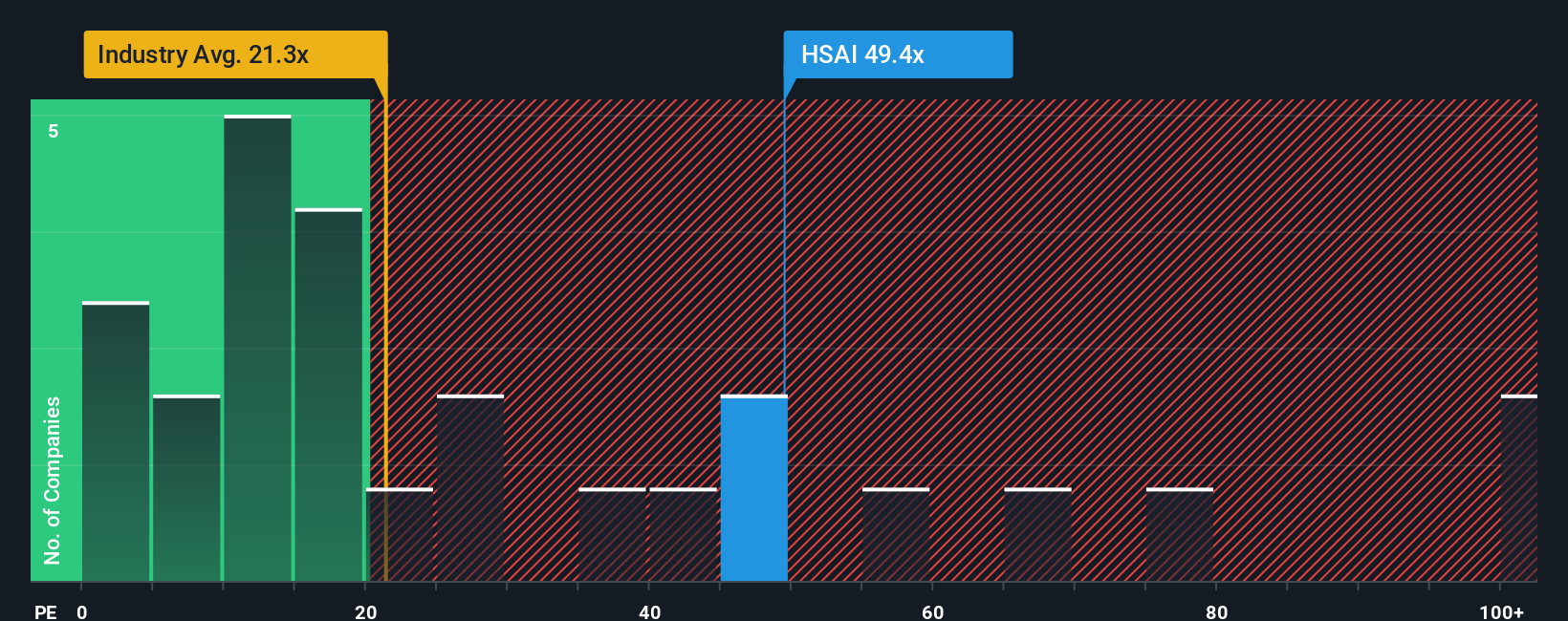

While our fair value estimate points to upside, the earnings picture looks stretched. Hesai trades on a 53.5x price to earnings ratio, well above both the Auto Components industry at 18.9x and its own 44.8x fair ratio, raising the risk of a painful de rating if growth wobbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Hesai Group Narrative

If you see the story differently, or want to dig into the numbers yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Hesai Group research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by using the Simply Wall Street Screener to uncover stocks that fit your strategy and time horizon.

- Capture potential mispricings by targeting companies that look fundamentally cheap through these 908 undervalued stocks based on cash flows and position yourself ahead of a possible re rating.

- Ride structural innovation by focusing on businesses building real world applications across automation and intelligent software with these 26 AI penny stocks.

- Strengthen your income stream by filtering for reliable payers offering attractive yields and consistent distributions via these 13 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com