- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalKerui Real Estate Research: Housing prices stopped falling month-on-month, cities increased, supply and demand structure indicators continued to be optimized

The Zhitong Finance App learned that on December 15, Kerui Real Estate Research published an article stating that in November, the first-hand housing price index fell 2.8% year on year, an increase of 0.2 percentage points over the previous month. Sales prices of new homes in major cities fell month-on-month. Affected by base period factors, the year-on-year decline in new housing prices in November ended a continuous narrowing trend during the year, showing a slight expansion, but the number of cities that stopped falling month-on-month increased markedly — to 11, 5 more than the previous month.

On the morning of December 15, the National Bureau of Statistics released macroeconomic and real estate data for November 2025 as scheduled. The national economy grew steadily, and the year-on-year growth rate of Social Security Zero declined. In terms of the real estate industry, sales scale, housing prices, investment, and the national housing sentiment index have all continued to be adjusted as the industry is in a critical period of transformation and development, and the impact of the increase in the previous year's base. However, from the perspective of specific cities and projects, there are still structural highlights in terms of new housing prices, project removal rates, etc., and supply and demand pressure on the industry continues to improve.

Social zero and M1 growth rates declined in November, and residents' medium- to long-term loans ushered in a recovery

In November 2025, various departments in various regions promoted the construction of a unified national market in depth, focusing on promoting high-quality development, stable production and supply, generally stable employment conditions, continued improvement in market prices, and steady development of new quality productivity. More specifically:

1. Industrial production is growing steadily, and the equipment manufacturing industry and high-tech manufacturing industry are growing rapidly. In November, the value added of industries above the national scale increased 4.8% year on year and 0.44% month on month. The value added of the equipment manufacturing industry increased by 7.7% year on year, and the value added of the high-tech manufacturing industry increased by 8.4%, which is 2.9 and 3.6 percentage points faster than the value added of industries above all sizes, respectively. 2. The scale of market sales has expanded, and the growth of retail service has accelerated. In November, total retail sales of social consumer goods amounted to 4389.8 billion yuan, up 1.3% year on year, down 1.6 percentage points from the previous month; down 0.42% month on month. 3. Overall investment in fixed assets declined year-on-year, and investment in manufacturing continued to grow. Excluding investment in real estate development, the country's fixed asset investment increased by 0.8% in the first 11 months, and investment in manufacturing increased by 1.9%. 4. The growth rate of imports and exports of goods picked up, and the trade structure continued to be optimized. In November, the total import and export volume of goods was 3898.7 billion yuan, up 4.1% year on year, 4.0 percentage points faster than the previous month. Among them, exports amounted to 2345.6 billion yuan, an increase of 5.7%. 5. The employment situation is generally stable. In November, the unemployment rate in the national urban survey was 5.1%, the same as last month.

Judging from the November financial data, M2 increased 8% year on year, down 0.2 percentage points from the previous month; M1 increased 4.9% year on year, and the growth rate decline widened to 1.3 percentage points. The scissor gap between the two reached 3.1 percentage points, an increase of 1.1 percentage points over the previous month, and has been rising for two consecutive months. This trend is mainly due to two factors: First, the M1 growth rate declined sharply, and second, the size of short-term loans to residents contracted month-on-month, a decrease of 264.7 billion yuan from the end of October. In this context, the Ministry of Commerce, the Central Bank, and the General Administration of Financial Supervision jointly issued a consumer promotion notice on December 14, introducing 11 policies and measures in the fields of commodity consumption, service consumption, and new types of consumption to expand domestic demand. As relevant policies are implemented at an accelerated pace, subsequent financial data is expected to gradually improve.

The size of residents' medium- to long-term loans stopped falling and rebounded. Preliminary statistics showed a month-on-month increase of 62.2 billion yuan in November. Currently, sales in the real estate industry are in a critical period of adjustment. Medium- and long-term loans can stop falling, fully reflecting positive changes in the operation of the industry. Recently, the governor of the central bank published a signed article clarifying that in the future, macroprudential management of real estate finance will be strengthened to promote the steady and healthy development of the real estate market. Meanwhile, the report of the Economic Work Conference released on December 11 also emphasized the need to actively and orderly resolve local government debt risks, urge all regions to take active debt, and resolutely curb new hidden debts; at the same time, optimize debt restructuring and replacement mechanisms to resolve the operating debt risks of local government financing platforms through multiple measures.

Looking forward to the future, financial policy will focus more on industry risk management, and the policy focus will also shift from focusing on mitigating corporate risk and further shifting to balancing corporate risk with local debt risk mitigation. This adjustment will unleash multiple positive effects: on the one hand, it will help speed up the removal of local urban investment inventories, ease the inventory pressure caused by the “new city” sector hoarding large amounts of land to be developed, and promote the orderly progress of the urbanization process; on the other hand, it can effectively reduce the financial burden on local governments, guide the pace of land concessions back to rationality, and avoid excessive local land promotion to ease short-term financial pressure, thus ensuring the steady development of high-quality sectors.

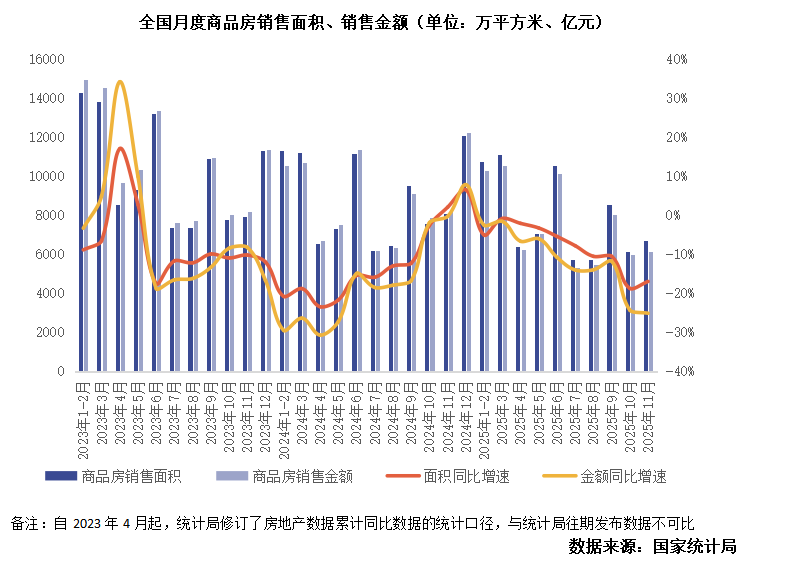

The year-on-year decline in the transaction area of new homes in a single month narrowed, and the removal rate index increased slightly

Affected by the sharp rise in the base figure last year, the cumulative year-on-year decline in new housing transactions continued to expand in November. The sales area of newly built commercial housing in the first 11 months was 787 million square meters, down 7.8% from the previous year, and the decline increased by 1 percentage point; in the first 11 months, the sales amount of commercial housing was 7.51 trillion yuan, down 11.1% year on year, and the decline increased by 1.5 percentage points. However, judging from the monthly data, the year-on-year decline remained stable, and the decline in sales area was 1.8 percentage points narrower than the previous month to 17%. In terms of funds available to housing enterprises, personal mortgage loans increased by 95.2 billion yuan in November, which was basically the same as the previous month. Inventory indicators continued to improve. In November, the area of commercial housing for sale fell by 3 million square meters, falling for 9 consecutive months.

In terms of specific cities, Kerui's core city data shows that in November, the volume of new housing transactions fell 16% month-on-month, and the year-on-year decline increased to 49%. This was mainly due to an increase in the previous year's base period values. On the other hand, it was also due to the continued low supply scale, which limited the scale of transactions at the end of the year. However, there was a slight increase in the removal rate index. In November, the removal rate of typical cities increased by 3 percentage points over the same period last month to 34%. Compound advantage projects such as high-end luxury, strong product strength, complete supporting facilities, and price advantages continue to be popular. Examples include Shanghai Jinling Huating, Zhengzhou Yuexiu Jinshui Guancui, and Guangzhou Poly Yuexiwan, all with an opening rate of over 90%.

The December Economic Work Conference made it clear that in the coming year, the city will focus on controlling growth, removing inventory, and improving supply, and encouraging the acquisition of existing commercial housing for affordable housing, etc. Deepen the reform of the housing provident fund system and promote the construction of “good houses” in an orderly manner. Domestic demand dominates the sector, and the expression of urban renewal was upgraded from “vigorous implementation” in 2024 to “high-quality promotion”, marking its leap from an old renovation project to a dual engine for stabilizing the property market and building a new model. It also proposed for the first time a pilot market-based reform to expand factors to provide lower-level institutional support for stabilizing the property market and urban renewal.

In the short term, it is expected that in order to speed up the improvement of inventory pressure indicators, the scale of new housing supply will remain low. Coupled with the development of affordable housing, it is expected that the volume and price index of new housing will continue to bottom out for a period of time. However, thanks to the reform of the Provident Fund system and the continued development of “good house” construction, along with the reasonable release of demand for improved housing, there will still be opportunities for high-quality development in the market.

In the long run, on the demand side, 35% of the housing stock in China's towns has been built for more than 20 years. Aging and household miniaturization have spawned demand for continuous renewal. Urban renewal forms a sustainable balance between supply and demand through “improving stock quality”; on the supply side, market-based reforms of land, capital, etc. can accurately match demand, reducing the industry's dependence on land value added.

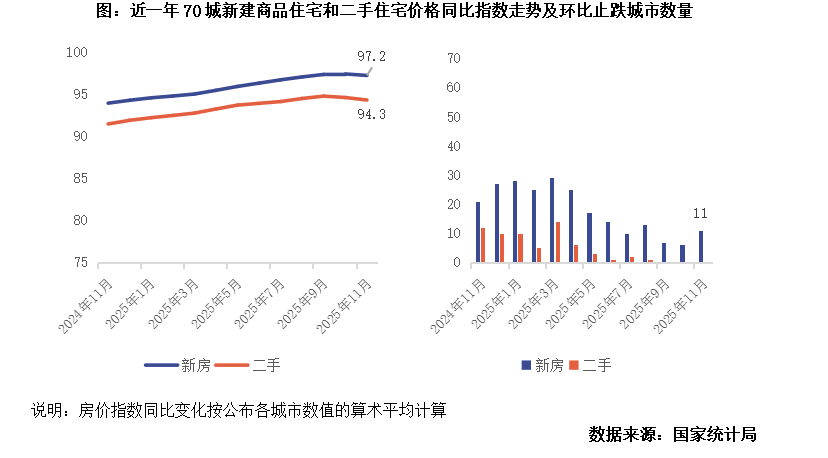

Housing prices fell overall in November, and the number of cities that stopped falling increased from month to month

In November 2025, commercial residential sales prices in 70 large and medium-sized cities generally declined month-on-month, and the year-on-year decline increased.

In November, the first-hand housing price index fell 2.8% year on year, an increase of 0.2 percentage points over the previous month. The sales price of newly built commercial residential homes in first-tier cities fell 1.2% year on year, an increase of 0.4 percentage points over the previous month. Among them, Shanghai rose 5.1%, while Beijing, Guangzhou and Shenzhen declined by 2.1%, 4.3%, and 3.7%, respectively. Sales prices of newly built commercial residential homes in second-tier and third-tier cities decreased by 2.2% and 3.5%, respectively, and the declines increased by 0.2 and 0.1 percentage points, respectively.

Sales prices of new homes in major cities fell month-on-month. The sales price of newly built commercial residential homes in first-tier cities fell 0.4% month-on-month, an increase of 0.1 percentage points over the previous month. Among them, Shanghai rose 0.1%, while Beijing, Guangzhou and Shenzhen declined by 0.5%, 0.5%, and 0.9%, respectively. Sales prices of newly built commercial residential homes in second- and third-tier cities fell by 0.3% and 0.4%, respectively, and both narrowed by 0.1 percentage points.

Affected by base period factors, the year-on-year decline in new housing prices in November ended a continuous narrowing trend during the year, showing a slight expansion, but the number of cities that stopped falling month-on-month increased markedly — to 11, 5 more than the previous month. In addition to Shanghai, Shenyang, and Hefei, new home prices in cities such as Dalian, Nanjing, Chongqing, Guiyang, and Yangzhou also stabilized month-on-month this month. As previously anticipated, new housing prices in more cities are showing signs of stabilizing against the backdrop of a continuous increase in the supply of high-quality housing and the gradual effects of supply-side controls in various regions.

At the same time, thanks to the current positive financial policy orientation, combined with the continuous adjustment of second-hand housing prices, rental housing that can cover the cost of purchase capital is gradually emerging in various regions. However, it should be noted that second-hand housing prices still have room for adjustment after poor location and poor quality, and the pace of price index adjustment may lag behind the industry's actual bottoming out cycle.

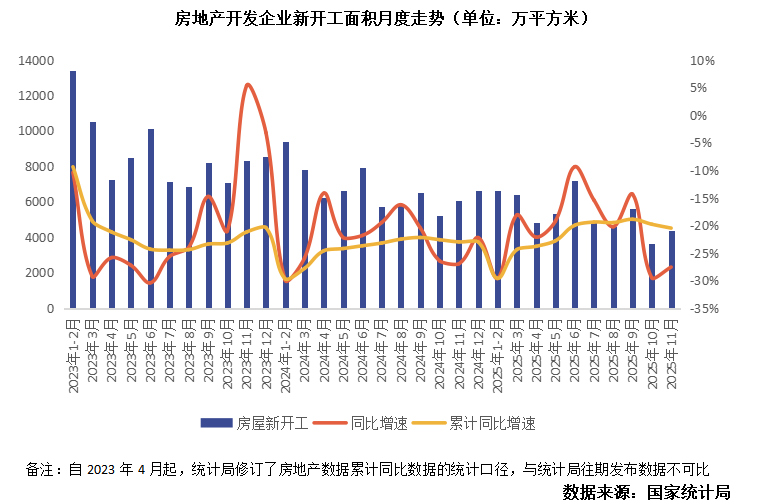

The cumulative scale of new construction is less than 70% of the sales scale of new homes, helping to reduce inventory pressure on the industry

From January to November, the housing construction area of real estate development enterprises was 6.56 billion square meters, a year-on-year decrease of 9.6%. Among them, the residential construction area was 4.58 billion square meters, a decrease of 10.0%.

In the first 11 months, the new housing construction area was 530 million square meters, a decrease of 20.5%. Among them, the new residential construction area was 390 million square meters, a decrease of 19.9%. In November, the new construction area was 43.96 million square meters, a year-on-year decrease of 27.6%, and a year-on-year decline of 1.9 percentage points.

The area of new housing construction in the first 11 months was only 68% of new home sales during the same period. The scale of new construction and new housing sales contracted simultaneously during the year, and continued to fall below new housing sales. While relieving the pressure on new housing inventories, it also guaranteed the market competitiveness of new supply projects, and encouraged the industry to continue to stop falling and stabilize.

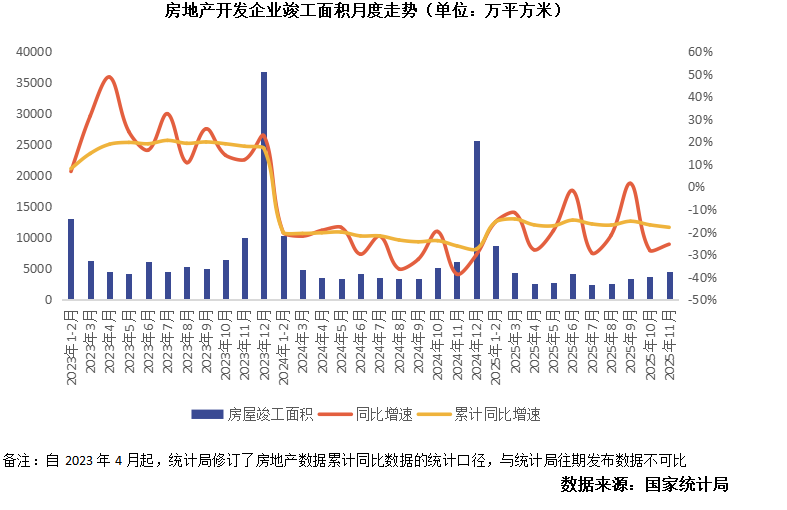

In the first 11 months of 2025, the country's completed housing area reached 390 million square meters, a year-on-year decrease of 18%, and an increase of 1.1 percentage points over the previous October; the area completed in November was 45.93 million square meters in a single month, down 25.5% from the previous year. Judging from the monthly trend, although the area completed in November was still in a year-on-year decline, the completed volume of the industry has shown a cyclical upward trend, reflecting that various regions are continuing to make efforts to promote housing security and delivery work. Although the completed area is not directly comparable to the new construction data due to differences in statistical caliber, a positive signal can be clearly seen from the year-on-year growth rate: the cumulative year-on-year decline in completed area during the year was controlled within 20%, which is significantly less than the year-on-year decline of more than 30% of the new construction area three years ago. This fully shows that the current project insurance and housing delivery work is achieving results. This progress was also confirmed at the policy level — at the China Economic Annual Conference held in December, the Deputy Director of the Central Finance Office made it clear that risk mitigation results in key areas have been remarkable since this year, the replacement of hidden debts by local governments has progressed in an orderly manner, and the task of securing housing delivery has been fully completed.

The investment-sales gap continues to narrow, and the industry accelerates towards a new model of development

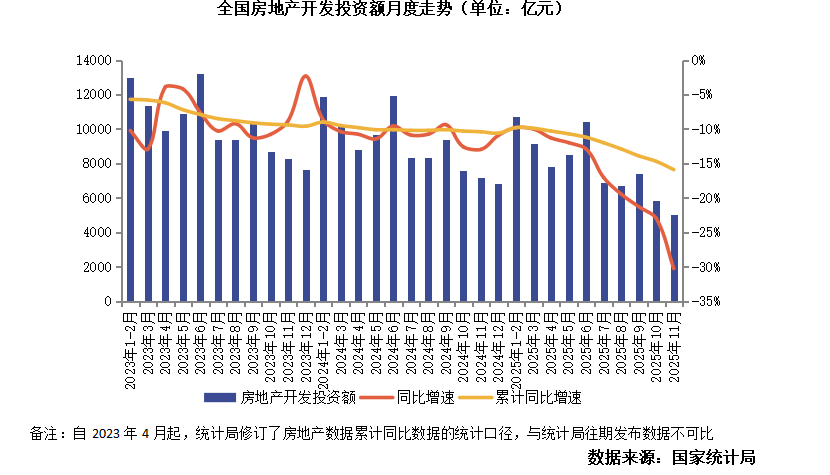

From January to November, the country invested 7859.1 billion yuan in real estate development, a year-on-year decrease of 15.9%. The decline was 4.8 percentage points higher than the sales of new homes during the same period. Looking at November alone, development investment was 502.8 billion yuan, down 30% from the previous year, and the decline was 7.3 percentage points higher than in October.

Further analysis of the degree of matching between investment and sales shows that the amount invested in real estate development in the first 11 months was 4.6% higher than the sales amount of new homes during the same period. This gap narrowed 2.1 percentage points from the previous month. The scale of development investment continues to move closer to the transaction amount of new homes, which intuitively reflects that the industry is gradually leaving the path of highly leveraged expansion and returning to a sales-oriented rational state of development.

This trend is also confirmed in the land market: in the previous 11 months, the total land auction area of 690 million square meters was only 88% of the sales area of new homes during the same period; compounded by the continuous decline in land prices in recent years, the cost pressure on new land concessions has been significantly reduced, and subsequent sales prospects have continued to improve. The dynamic adaptation of investment, sales and the land market is a powerful reflection of the industry's smooth transition to a new model of development.

In summary, Kerui Real Estate Research made the following judgments:

Combined with the current state of the market, the industry is at a critical stage of digesting backlog inventory, reshaping price confidence, and transforming demand drivers. The demand side has moved from being driven by urbanization growth and improvements in housing conditions to being driven by housing renewal and quality upgrades. This has led to gradual adjustments in scale indicators such as industry transactions and investment.

In December, the Central Economic Work Conference clarified eight key tasks for 2026. Real estate-related deployments focus on Article 8 “Adhere to the bottom line and actively and steadily mitigate risks in key areas”. The core requirements include focusing on stabilizing the real estate market, speeding up the construction of a new real estate development model and local government debt insurance; the livelihood sector focuses on topics such as employment, education, medical care, marriage and childbearing, and disaster prevention. Notably, unlike real estate, “urban renewal” is listed separately from real estate. It is included in the first “domestic demand-led” category, and the relevant statement was upgraded to “promote urban renewal with high quality”.

In order to consolidate the stable trend in the market, local authorities continue to step up efforts to control growth, remove inventory, and improve supply. At present, more than 25 provincial administrative districts across the country have issued the “15th Five-Year Plan” development plan proposals. In the real estate sector, the most frequently mentioned expressions are “developing guaranteed housing” and “good housing.” Both are new supply directions with strong certainty under the current market. In terms of inventory revitalization, the planning proposals focus on deepening the market-based allocation reform of factors. The aim is to promote the efficient allocation of various factor resources and the concentration of advanced productivity, thereby expanding domestic demand and helping economic development. Furthermore, urban renewal is also separate from real estate, emphasizing deep ties with industry and population development.

It can be seen from this that in the future, the real estate market will mitigate stock risks while increasing demand will become more certain. Judging from the demand structure, as the industry leaves the dividend period of large-scale urbanization expansion, housing renewal will become a core component of demand. According to population census data, about 35% of the existing housing stock in China's cities took more than 20 years to build; however, large amounts of inefficient land also objectively constrain urban development. By transforming various types of inefficient land, it is possible not only to meet residents' housing renewal needs and promote the upgrading of urban industries, but also to release more high-quality residential land for the real estate market and help the development of “good houses”. There is still plenty of room for high-quality urban renewal.

Looking at short-term industry indicators, the scale of new housing transactions is expected to continue to be low at the end of 2025 due to the rise in base period values and the development expectations of the industry to accelerate the implementation of balance between supply and demand; in order to promote industrialized insurance, investment and new construction data will also continue to decline, and overall housing prices still need to seek further support from the bottom. However, long-term and short-term inventory pressure in various regions will continue to ease, as reflected in the continuous optimization of indicators such as investment and sales ratio, first-tier market size ratio, new construction sales ratio, and area to be sold; at the same time, as the share of marketable products in the market increases further, the opening and elimination rate of new housing projects is expected to continue to improve.