- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDoes Zevra Therapeutics Near $8 Reflect Its 92% DCF Upside Potential in 2025?

- Wondering if Zevra Therapeutics at around $8 a share is a hidden bargain or just another biotech rollercoaster? You are not alone. Let us break down what the current price might really be telling us.

- The stock is roughly flat over the last year, down 1.8%, but that sits on top of a wild 84.7% gain over three years and a 55.5% drop over five years. This pattern hints at shifting market confidence rather than a simple growth story.

- Recent attention has centered on Zevra's progress with its rare disease portfolio and regulatory milestones. This has helped frame the stock as a potential catalyst-driven rather than purely speculative biotech name. At the same time, investor focus on capital allocation, pipeline prioritization, and partnership opportunities has sharpened views on what the current share price might already be pricing in.

- Despite the volatility, our model gives Zevra a valuation score of 6/6. This suggests it screens as undervalued across every one of our checks. Next, we will unpack how different valuation approaches arrive at that view, before finishing with a more powerful way to think about what the stock might really be worth.

Find out why Zevra Therapeutics's -1.8% return over the last year is lagging behind its peers.

Approach 1: Zevra Therapeutics Discounted Cash Flow (DCF) Analysis

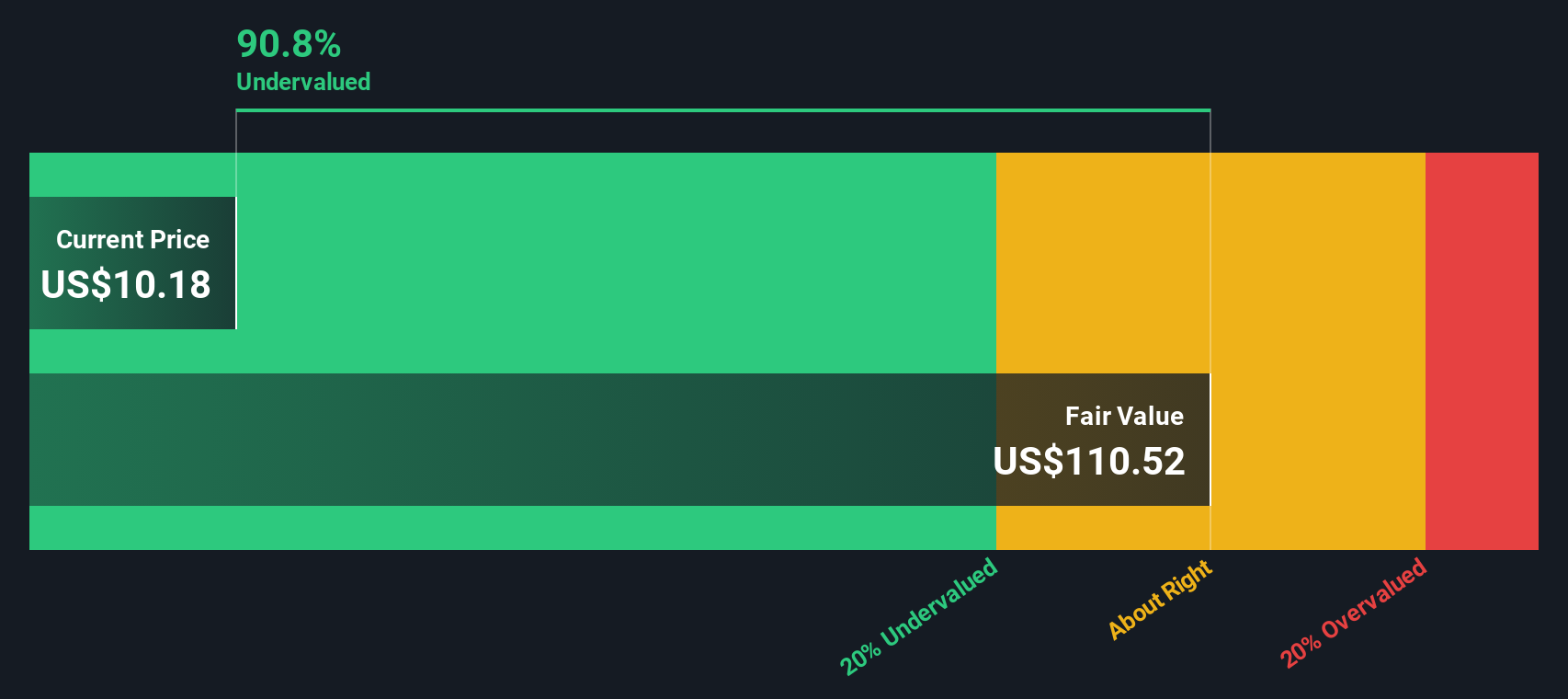

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it could generate in the future and then discounting those cash flows back to today in $ terms. For Zevra Therapeutics, the 2 stage Free Cash Flow to Equity approach starts from a last twelve months free cash outflow of about $24.2 million, reflecting that the company is still investing heavily rather than producing steady surplus cash.

Analysts expect that to flip over the next few years, with projected free cash flow reaching roughly $179.8 million by 2029. Beyond the explicit analyst horizon, Simply Wall St extrapolates further growth, with ten year projections climbing toward the low to mid $300 million range, but applying an increasingly conservative growth rate as the business matures.

Bringing all of those projected cash flows back to today yields an estimated intrinsic value of about $104.13 per share. Compared with a recent market price around $8, the DCF implies the stock is roughly 92.0% undervalued, indicating that investors are heavily discounting Zevra's potential cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Zevra Therapeutics is undervalued by 92.0%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

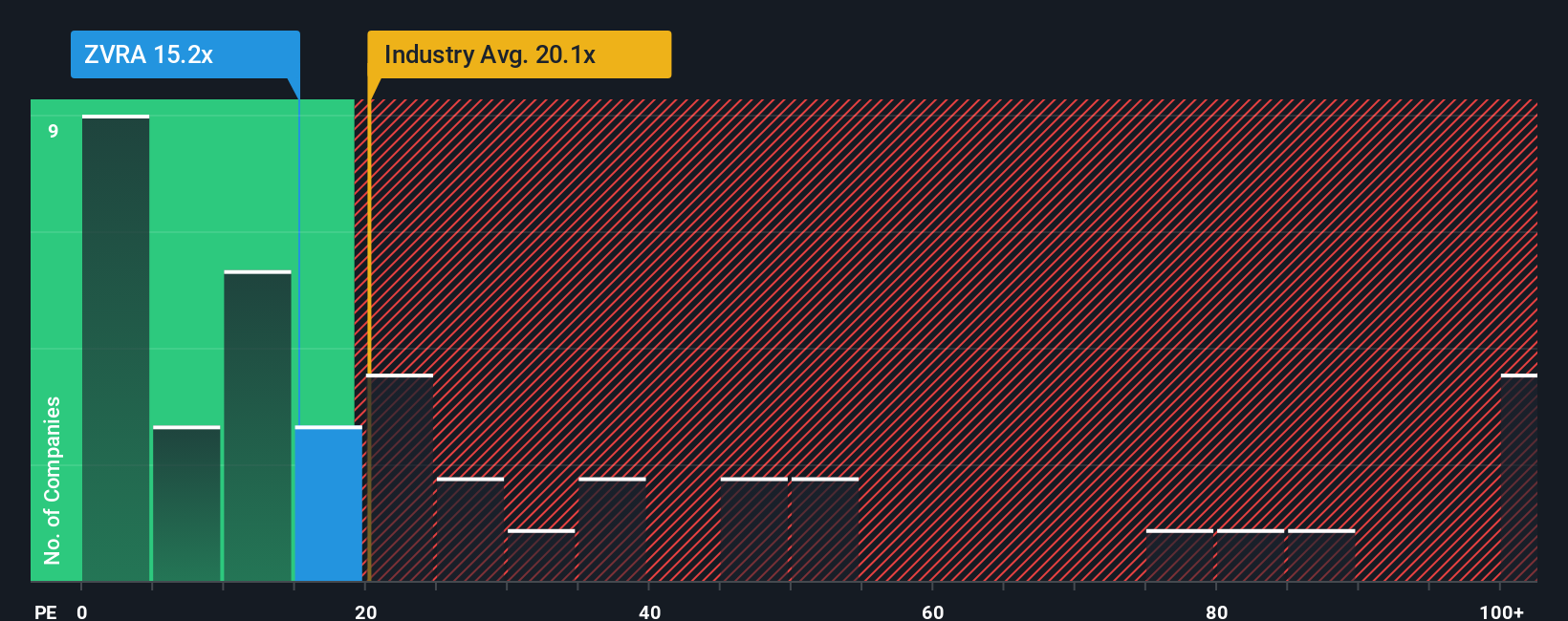

Approach 2: Zevra Therapeutics Price vs Earnings

For companies that are generating profits, the price to earnings, or PE, ratio is a straightforward way to gauge how much investors are willing to pay for each dollar of earnings. In broad terms, faster growth and lower perceived risk justify a higher PE, while slower growth or higher uncertainty point to a lower, more cautious multiple.

Zevra currently trades on a PE of about 15.6x, which is below both the Pharmaceuticals industry average of roughly 20.0x and the broader peer group around 31.3x. On the surface, that discount suggests the market is either skeptical about the durability of Zevra’s earnings or is simply less excited about its story than about other drug developers.

Simply Wall St’s Fair Ratio metric offers a more tailored lens. It estimates what a “normal” PE should be for Zevra, given its earnings growth outlook, profitability profile, risk factors, industry, and market cap. For Zevra, the Fair Ratio comes out at about 20.8x, meaning the shares trade at a meaningful discount to where they might sit if investors fully priced in those fundamentals. That gap indicates the stock appears undervalued on a PE basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Zevra Therapeutics Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, an easy tool on Simply Wall St's Community page that lets you connect your view of a company’s story to a concrete forecast and a Fair Value that you can compare to today’s price.

A Narrative is simply your story behind the numbers, where you outline how you expect Zevra’s revenue, earnings, and margins to evolve, and the platform automatically turns that into a financial forecast and implied Fair Value, then keeps it up to date as new news or earnings come in.

This makes Narratives a dynamic guide for investment decisions, because you can instantly see whether your Fair Value still supports owning the stock at its current price, and quickly adjust your assumptions when something material changes.

For Zevra Therapeutics, for example, an investor with a more optimistic view might build a Narrative around analysts’ higher-end assumptions and a Fair Value closer to about $29 per share, while a more cautious investor might lean on the lower-end assumptions and arrive nearer to $18, using the same tool to express very different perspectives.

Do you think there's more to the story for Zevra Therapeutics? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com