- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalThere's Reason For Concern Over Diagnósticos da América S.A.'s (BVMF:DASA3) Massive 68% Price Jump

Despite an already strong run, Diagnósticos da América S.A. (BVMF:DASA3) shares have been powering on, with a gain of 68% in the last thirty days. The last 30 days bring the annual gain to a very sharp 73%.

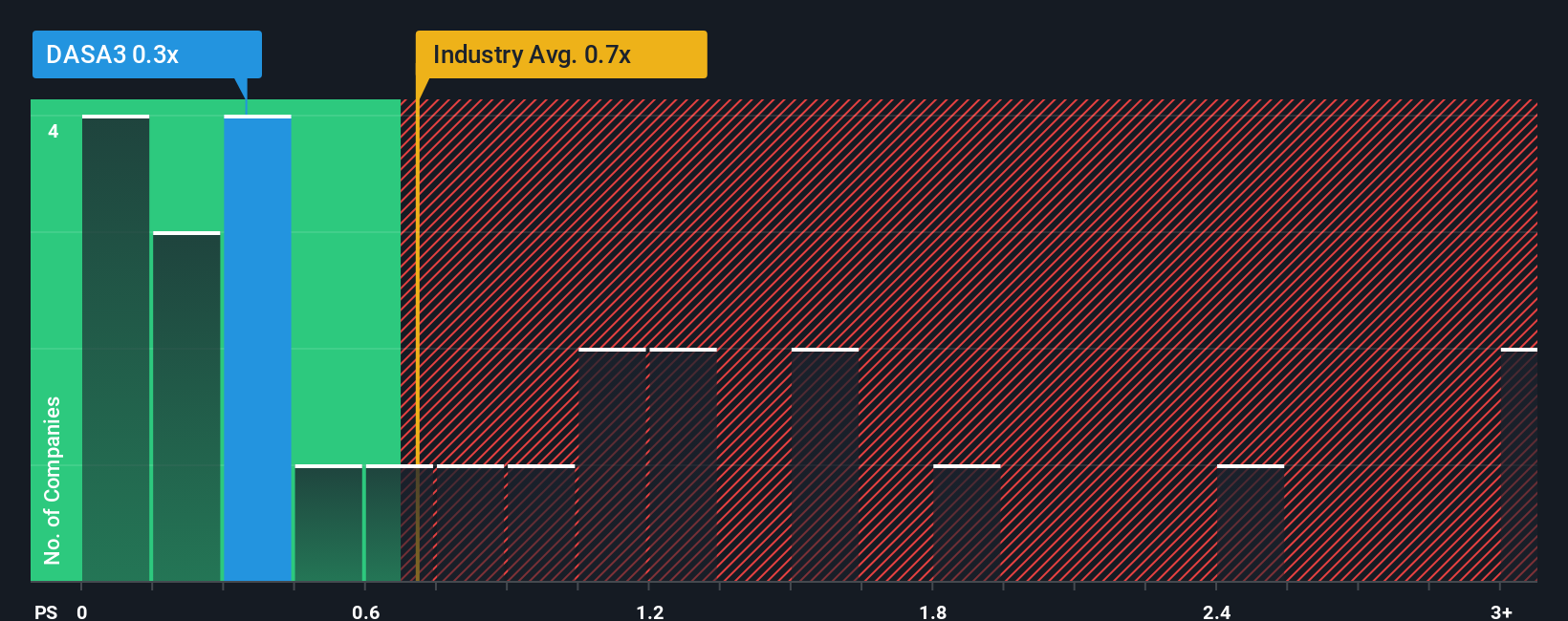

Even after such a large jump in price, it's still not a stretch to say that Diagnósticos da América's price-to-sales (or "P/S") ratio of 0.3x right now seems quite "middle-of-the-road" compared to the Healthcare industry in Brazil, where the median P/S ratio is around 0.4x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Diagnósticos da América

What Does Diagnósticos da América's Recent Performance Look Like?

Diagnósticos da América could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Diagnósticos da América will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Diagnósticos da América?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Diagnósticos da América's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 16%. Unfortunately, that's brought it right back to where it started three years ago with revenue growth being virtually non-existent overall during that time. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Looking ahead now, revenue is anticipated to slump, contracting by 17% during the coming year according to the lone analyst following the company. Meanwhile, the broader industry is forecast to expand by 10%, which paints a poor picture.

In light of this, it's somewhat alarming that Diagnósticos da América's P/S sits in line with the majority of other companies. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

What We Can Learn From Diagnósticos da América's P/S?

Diagnósticos da América appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

While Diagnósticos da América's P/S isn't anything out of the ordinary for companies in the industry, we didn't expect it given forecasts of revenue decline. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If we consider the revenue outlook, the P/S seems to indicate that potential investors may be paying a premium for the stock.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Diagnósticos da América (at least 2 which are a bit unpleasant), and understanding these should be part of your investment process.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.